How to Spot Forex Scams and Unregulated Brokers (Safety Checklist)

Forex scams cost traders money fast. The damage often starts with one click, one deposit, and one fake promise. This guide shows you how to spot forex scams and avoid unregulated brokers before you fund an account.

You will learn the most common scam patterns, the red flags on broker websites and apps, and the exact checks that confirm a broker holds a real license. You will also learn how scammers use bonuses, “account managers,” copy trading, and withdrawal blocks to trap your funds.

Use the checklist to verify regulation, confirm the legal entity behind a brand, review fees and leverage terms, test withdrawals, and document everything. If you also trade from the US, read our guide on Is Forex Trading Legal in the US before you open an account.

Key Takeaways

- In het kort: Treat every broker as untrusted until you verify its license in the regulator’s own register.

- Match the broker name, legal entity, and address to the regulator record. Do not rely on logos, badges, or “regulated” claims.

- Check who holds your money. Avoid offshore entities, unclear ownership, and “global brands” with no single accountable company.

- Read the fee and leverage terms before you deposit. Watch for wide spreads, hidden commissions, inactivity fees, and extreme leverage.

- Ignore bonuses and pressure. “Limited time” offers, account managers, and upsell calls signal high risk.

- Do not trust copy trading or managed accounts from strangers. If you cannot verify licensing and track record, you take the full risk.

- Test the system early. Make a small deposit, place a simple trade, then request a withdrawal. Track how long it takes and what documents they demand.

- Watch for withdrawal blocks. Extra “verification,” sudden fees, forced trading volume, or account freezes often precede a loss.

- Document everything. Save emails, chats, receipts, platform logs, and wallet or bank references. You need proof for disputes and reports.

- If you trade from the US, confirm the broker’s US status before you fund an account. Use our guide on whether forex trading is legal in the United States.

Forex scams vs. unregulated brokers: what they are and why it matters

How legitimate brokers operate

A real broker follows rules that limit how they can handle your money and your trades. Regulation does not remove risk, but it raises the cost of abuse.

- Licensing: The broker holds a current license from a recognized regulator. The license covers the exact legal entity that takes your deposits.

- Segregation of client funds: Your money sits in separate accounts from the broker’s operating cash. This reduces the chance your deposit funds their expenses or losses.

- Minimum capital requirements: Regulators often require brokers to hold a capital buffer. Thinly capitalized firms fail faster and freeze withdrawals sooner.

- Audits and reporting: Regulated brokers file regular reports and face audits. This creates paper trails you can use in disputes.

- Conduct rules: Regulators limit misleading marketing, bonuses, and high pressure sales tactics, depending on the jurisdiction.

- Dispute resolution: You get a formal complaint path, deadlines, and a regulator that can sanction the firm. With scams, you get support tickets and silence.

Forex scams vs. unregulated brokers

A forex scam has one goal, take your deposit. An unregulated broker might execute trades, but you have no enforceable protections. Both can end with the same result, you cannot withdraw.

- Scam: The “platform” can be fake. Prices, balances, and profits can be invented. The business runs like a deposit funnel.

- Unregulated broker: The platform can be real, but the company answers to no serious authority. If they manipulate execution, change terms, or delay payouts, you have little leverage.

Key differences: unregulated, offshore regulated, regulated in your country

These labels sound similar. They are not.

| Label you see | What it usually means | What it means for your safety |

|---|---|---|

| Unregulated | No license, or a license claim with no verifiable record for the entity taking your funds. | Low accountability. Few enforceable rules on custody, reporting, complaints, or withdrawals. |

| Offshore regulated | Licensed in a small jurisdiction that markets itself to financial firms, often with lighter oversight. | Better than nothing, but weak enforcement is common. Cross-border complaints move slowly and cost more. |

| Regulated in your country | Licensed where you live, with local conduct rules and local enforcement tools. | Higher chance of recovery options, faster complaint handling, clearer legal jurisdiction. |

Focus on the legal entity name, license number, and regulator register entry. A brand name on a website proves nothing.

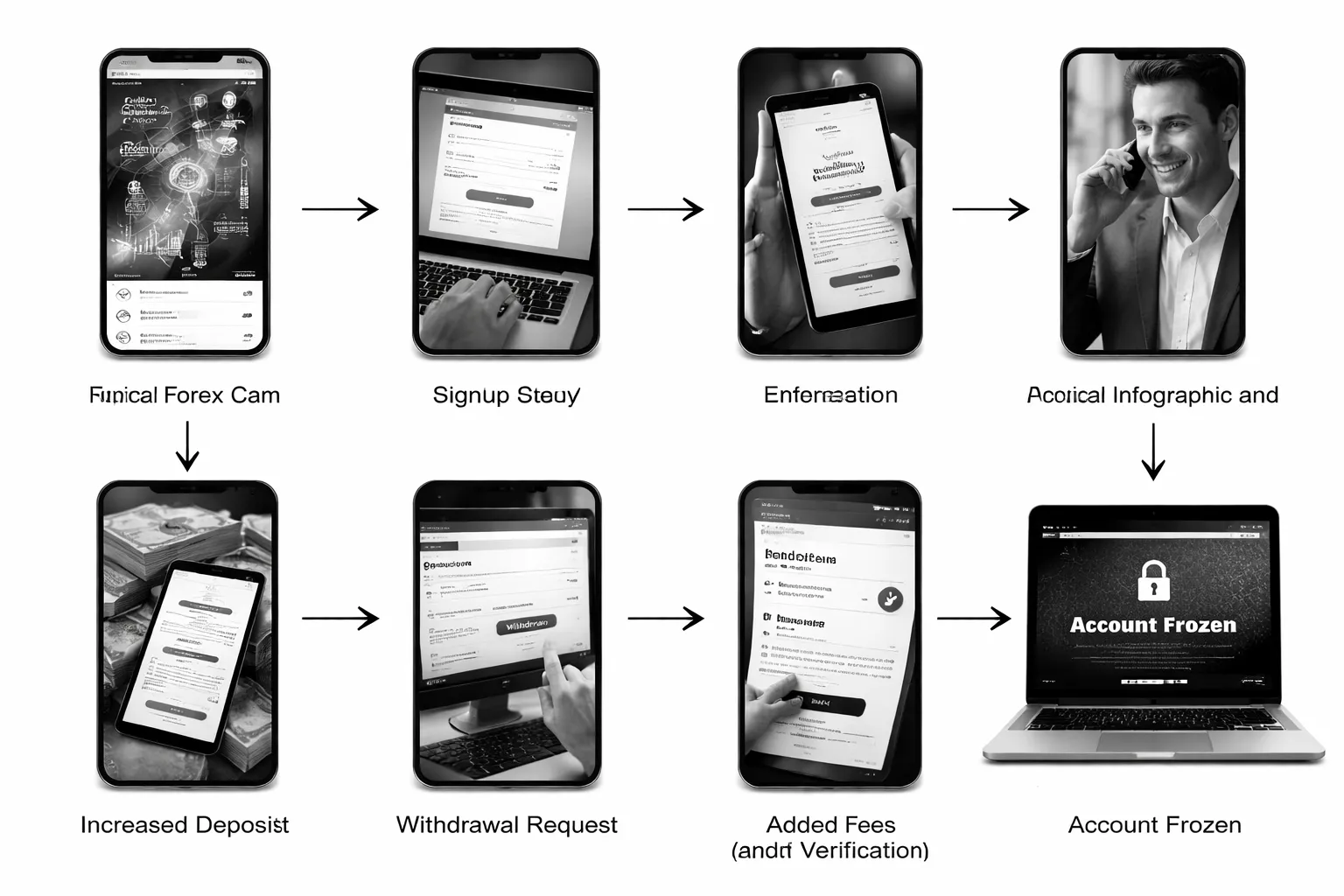

Typical victim journey: ad click to “account manager” to withdrawal blockage

Many losses follow the same path. You can spot it early if you know the steps.

- Step 1, the hook: You see an ad on social media, messaging apps, or search. It promises fast returns, “AI trading,” or guaranteed signals.

- Step 2, fast onboarding: They push you to deposit small amounts first. They make it feel easy and urgent.

- Step 3, the closer: An “account manager” calls you. They steer you to larger deposits, remote access apps, or crypto payments.

- Step 4, manufactured success: Your account shows quick profits. They use this to push bigger funding and higher leverage.

- Step 5, the withdrawal trap: When you request a payout, they add conditions. Identity “rechecks,” tax or fee demands, bonus clauses, minimum trading volume, or sudden margin issues.

- Step 6, the lock: They delay, then freeze the account, then stop responding. Sometimes they offer “recovery” if you pay again.

If you trade from the US, confirm the broker’s US status before you send money. Use our guide on forex trading rules in the United States.

Why forex attracts fraud

- High leverage: Large position sizes magnify gains and losses. Scammers use this to sell big outcomes and justify sudden blowups.

- Complex pricing and execution: Spreads, slippage, margin calls, and swaps confuse new traders. Fraudsters hide behind jargon when withdrawals fail.

- Cross-border payments: Crypto, wire transfers, and payment processors make chargebacks harder. Jurisdiction fights slow everything down.

- Always-on marketing: Social platforms let fake firms target by interest, income, and location. They can vanish and relaunch under a new name fast.

The safety checklist: how to spot forex scams and unregulated brokers fast

Regulation verification steps, use official registers only

- Start with the regulator name, then find the register. Do not trust a badge image, a PDF, or a “regulated” claim on the broker site.

- FCA (UK). Search the Financial Services Register. Match the firm name, FRN, status, and “permissions.” Check if it says “EEA authorised” or “appointed representative,” these are common abuse points.

- NFA and CFTC (US). Use NFA BASIC. Confirm the firm is an FCM or RFED for retail forex. Many scams show a random NFA ID that belongs to someone else.

- ASIC (Australia). Check ASIC Professional Registers for the AFS license. Verify the licensee name and “authorised representatives.”

- CySEC (Cyprus, EU). Use CySEC’s CIF register. Confirm the CIF number and domain details listed by the regulator, if available.

- Also check major local regulators. IIROC or CIRO (Canada), MAS (Singapore), DFSA (DIFC), FSCA (South Africa), SFC (Hong Kong), FSA (Japan). If the broker takes your country as a client, it must show a valid legal basis.

- Confirm the status. Look for “Authorised,” “Current,” or “Active.” Avoid “No longer authorised,” “Suspended,” “Under investigation,” or “Unregistered.”

License clone detection, match the real entity to the brand you use

- Match the legal entity name. The register lists a company name, not a brand name. If the website only shows the brand, push for the full legal entity.

- Match the domain. Clone scams copy a real license number but operate on a different domain. Treat domain mismatch as a stop sign.

- Match the address and phone. Compare the register data to the broker’s footer, legal page, and emails. Scammers often use a real address with a different suite number.

- Match reference numbers. FCA FRN, CySEC CIF number, NFA ID. Confirm the number belongs to the exact entity you deal with.

- Check for regulator warnings. Many regulators publish “clone firm” alerts. Search the regulator site plus the broker name and domain.

Company due diligence, verify the business behind the site

- Pull the corporate registry record. UK Companies House, Cyprus Registrar, ASIC company search, state registries in the US. Confirm incorporation date and active status.

- Check directors and owners. Look for recent director churn, nominee patterns, or missing beneficial ownership where disclosure is standard.

- Measure operating history. Compare “years in business” claims against incorporation date and domain age.

- Map brand and entity structure. Many scams hide behind a marketing brand while the contract sits with an offshore entity. Your money follows the contract, not the brand.

- Confirm the client entity for your country. Legit groups often run multiple regulated entities. Scams route you to an unregulated subsidiary at signup.

Platform and trade execution checks, look for patterns that cost you money

- Track spreads at liquid times. Compare EUR/USD and major pairs during London and New York overlap to reputable brokers. Persistent wide spreads signal dealing desk abuse or fake pricing.

- Log slippage. Record each market order: requested price, filled price, time, and volatility conditions. One way slippage that only hurts you is a red flag.

- Watch for repeated requotes and rejections. Frequent “off quotes,” “trade context busy,” or rejected stops in normal markets suggests platform manipulation.

- Test execution with small size. Place the same type of order at similar times across days. Scams show inconsistent fills and unexplained spikes.

- Verify the platform build and server. For MT4 or MT5, confirm the broker server name matches the legal entity and domain. Fake servers exist.

Deposit and withdrawal red flags, follow the money path

- Crypto only funding. Crypto removes chargebacks and speeds disappearances. Treat it as high risk, especially for first deposit.

- Third party payments. If they ask you to pay a different company or a person, stop. Regulated brokers do not need this.

- “Processing fees” to unlock withdrawals. Scammers demand extra deposits to release funds, clear “tax,” or “verify” a wallet. Legit brokers deduct fees from balance, they do not demand new money.

- Withdrawal friction. Delays, shifting requirements, or “compliance review” that never ends signals a payout block.

- Account manager pressure. If someone pushes bigger deposits right before you request a withdrawal, treat it as a trap.

Terms and conditions traps, read what blocks your exit

- Bonus wagering rules. If a bonus forces huge volume before withdrawal, your cash can get locked with the bonus. Avoid deposit bonuses.

- Forced minimum volume. Some terms tie withdrawals to a trading target, even without a bonus. That is a control lever.

- Inactivity and admin fees. High monthly “dormant” fees drain accounts and create pressure to trade.

- Unilateral changes. Terms that let them change spreads, leverage, margin rules, or withdrawal policies without notice increase abuse risk.

- Dispute venue clauses. Offshore arbitration, unclear governing law, or “sole discretion” language makes recovery harder.

KYC and AML misuse patterns, spot the endless loop

- Endless verification. They accept deposits fast, then demand new documents at withdrawal. Each round adds delay.

- Selective enforcement. They ignore KYC until you win or request a payout, then block you for minor issues.

- Document overreach. Requests for unnecessary data, full card photos, or remote device access signal risk. Real KYC asks for standard ID and proof of address.

- Changing requirements. If the checklist keeps expanding, you face a stalling tactic, not compliance.

Communication warning signs, demand traceable commitments

- WhatsApp or Telegram only. Real brokers provide ticket systems, email, and phone tied to the legal entity.

- Scripted replies. If every issue gets a copy paste answer, expect no resolution.

- Avoidance of written commitments. If they refuse to confirm fees, timelines, or policies by email, assume the opposite will happen.

- Pressure tactics. Time limited “upgrade,” “VIP,” or “recovery” offers aim to rush you past checks. See the full safety flow in our forex scam safety checklist.

Marketing credibility audit, verify claims outside their ecosystem

- Fake testimonials. Look for repeated phrasing, stock photos, and profiles with no history.

- Paid review farms. Sudden waves of 5 star reviews, similar wording, and new accounts signal manipulation.

- Manipulated review pages. Some sites copy “Trustpilot style” layouts with no real platform backing. Click through to the actual review domain.

- Unverifiable performance claims. Guaranteed returns, fixed daily profit, or “risk free” language marks a fraud pitch.

- Affiliate heavy funnels. If search results show mostly coupon codes, referral pages, and promo articles, the brand may run on incentives, not service.

Cybersecurity basics, check the surface area before you sign in

- Domain age. Check WHOIS or a domain history tool. A “10 year broker” on a 3 month old domain is a mismatch.

- HTTPS is not enough. HTTPS only encrypts traffic. It does not prove regulation or honesty.

- App authenticity. Install only from official app stores or verified links. Check the publisher name and reviews for consistency.

- Remote access tool requests. Any request to install AnyDesk, TeamViewer, or similar tools is a major red flag. Scammers use it to move funds and capture logins.

- Email hygiene. Watch for free email domains, lookalike spellings, and mismatched sender domains in support emails.

| Fast check | What to confirm | If it fails |

|---|---|---|

| Regulator register | Entity name, status, permissions, reference number | Assume unregulated, do not deposit |

| Clone screening | Domain, address, phone match the register | Assume license cloning |

| Payments | Same entity receives funds, normal methods, clear fees | Expect withdrawal friction |

| Execution | Normal spreads, balanced slippage, low rejections | Expect price manipulation |

| Terms | No bonus lock, clear withdrawal rules, stable policies | Expect trapped funds |

| Support | Tickets, email trail, specific written answers | Expect stalling and denial |

Common forex scam types you’ll see (with examples of the telltale signs)

Signal seller and “VIP group” scams

You pay for trade alerts, a chat room, or a “mentor.” The real product is your subscription and your referral sign up.

- Performance screenshots. They post cropped wins, no timestamps, no account ID, no broker name, no history tab.

- Referral funnel. You must open an account through their link, use their “partner broker,” or deposit a minimum to “unlock” signals.

- Paywalled losses. Free channel shows wins, VIP channel holds the losing trades, stop outs, and “recovery” martingale ladders.

- No third party verification. They refuse Myfxbook, FX Blue, or a read only investor link. They claim it “reveals the strategy.”

- Pressure to act fast. “Last spots,” “price doubles tonight,” “only serious traders.”

Account manager and boiler room scams

They pitch “managed forex” or “we trade for you.” Then they push bigger deposits and block withdrawals.

- High pressure calls. They call often. They rush you. They dismiss written questions.

- Emotional manipulation. They tie your deposit to urgency, pride, or fear. “You are close,” “don’t quit now,” “you will regret it.”

- Upsell ladder. Small deposit first, then “upgrade to VIP,” then “add margin,” then “top up to avoid liquidation.”

- Scripted authority. They claim ex bank roles, “institutional desk,” or inside access. No verifiable credentials.

- Withdrawal hostage tactics. They demand extra deposits for “tax,” “insurance,” “verification,” or “anti money laundering release.”

Copy trading and PAMM/MAM fraud

You copy a trader or join a managed allocation pool. You never get clean, auditable proof of trading.

- Opaque track record. They show a single equity curve image, no trade list, no account history, no broker statement you can verify.

- Short, cherry picked history. They highlight 1 to 3 good months. They hide prior blow ups and account resets.

- Unrealistic stability. Smooth daily gains with no drawdowns. Real trading shows drawdown and variance.

- Control of your funds. They ask for login, remote access, or to “add you to MAM” without clear legal docs.

- Fees that punish exits. High performance fees, lockups, and “notice periods,” then delays when you request withdrawal.

Fake trading platforms and app clones

You trade on a web platform or app that looks like MT4 or MT5. The numbers are not real.

- Simulated profits. Your account grows fast. Withdrawals fail, or they “review” forever.

- Rigged charts. Spreads widen at random, spikes hit only your stop, fills ignore your limit price.

- Missing market details. No instrument specs, no swap rates, no execution policy, no server time, no audit trail.

- App store lookalikes. Similar name and logo to a known broker. Different publisher, website, or support email.

- Deposit routing tricks. They accept crypto to personal wallets, or card payments to unrelated merchants.

Bonus and recovery scams

Bonuses trap your funds. Recovery scams hit after you lose money. Both aim to extract more deposits.

- Bonus lock clauses. They require huge “volume” before you can withdraw. They cancel withdrawals due to “bonus abuse.”

- Terms that change. They update policies after you deposit, then apply new rules to old funds.

- Recovery scam pitch. A “chargeback expert” or “fund retriever” contacts you, often from social media or messaging apps.

- Double dipping. They ask for upfront fees, then “tax” or “court” costs, then more money to “release” your refund.

- Fake authority. They use regulator logos, case numbers, and legal threats. They refuse verifiable office details.

Pig butchering variants in forex

They build a relationship first. Then they guide you into a “private” forex platform and push large deposits.

- Relationship grooming. Daily chats, fast trust, then talk shifts to trading results and “helping you.”

- Guided deposits. They teach you how to buy crypto and send it to the “broker,” often to a new address each time.

- Controlled withdrawal bait. They allow one small withdrawal to build confidence, then block larger ones.

- Escalation plan. They push bigger sizes, leverage, and urgent “events.” Your deposits rise fast.

- Isolation tactics. They tell you not to talk to friends or banks. They claim “banks don’t understand crypto trading.”

For deeper checks on fake track records and verified results, use our guide to reading Myfxbook results.

Red flags by category: behaviors, numbers, and policies that don’t add up

Promises that violate market reality

If the pitch sounds like a savings account, treat it as a threat.

- Guaranteed returns. Markets do not allow guaranteed profit. Anyone who promises certainty controls the story, not the risk.

- No risk or “protected” trading. Losses can happen on any leveraged product. “Risk-free” usually means you carry the risk and they control access.

- Fixed daily profits. A fixed daily percentage has a math problem. Compounding turns small daily promises into impossible annual results.

- Zero drawdown claims. Real trading has losing streaks. Zero drawdown usually means fake reporting, selective history, or backfilled results.

Unrealistic trading conditions

Scam brokers sell conditions that look perfect on paper and break in live markets.

- Extreme leverage pushed as “standard.” High leverage increases the chance of fast wipeouts. It also lets the broker profit from rapid churn and margin calls.

- Too-good spreads with no tradeoffs. Tight spreads should come with clear commissions, realistic slippage, and normal execution rules. If the broker cannot explain the cost model, assume hidden markups.

- “No slippage” or “instant fills” on news. News spikes create gaps and slippage. A promise of perfect fills signals price control, not market access.

- Claims of constant high win rates. A very high win rate often comes from martingale sizing or holding losses until they blow up. Ask for full history and maximum drawdown, not just wins.

Pressure tactics

Legit brokers let you choose your pace. Scammers force urgency.

- Limited-time bonuses tied to deposits. Bonuses often come with withdrawal locks and volume requirements. The “gift” becomes a cage.

- Threats to close positions unless you deposit more. Margin calls follow rules, not negotiations. If they demand a top-up by wire or crypto to “save” trades, you are in a trap.

- Escalation scripts. They push bigger lots, higher leverage, and “once-a-year” events. They punish hesitation with fear, then reward deposits with praise.

- Refusal to put terms in writing. If support will not email the exact policy, they want deniability.

Conflicts of interest

You need to know who wins when you lose.

- Dealing-desk opacity. If they cannot explain order routing and execution, assume they can trade against you.

- Undisclosed markups. Watch for “raw spreads” paired with vague fees, or fixed spreads that widen at key times without notice.

- Incentive-based “advice.” If the same person who sells you deposits also gives trade signals, the incentive points one way.

- Account manager control. If they ask for remote access, platform login, or “trade on your behalf” without a regulated mandate, stop.

Withdrawal friction signals

Most forex scams break at the withdrawal step. Track every new rule.

- Upfront taxes, insurance, or “clearance” fees. Real taxes do not require you to pay a broker before you withdraw your own funds. A demand for prepayment is a common extraction tactic.

- New verification fees after you request a payout. KYC checks happen at onboarding, not after you ask for money back. Sudden “verification invoices” signal stalling.

- Withdrawal minimums that keep rising. They move the goalposts so you keep depositing to qualify.

- Only crypto or wire for “faster release.” They steer you to irreversible rails, then blame “processing” when you complain.

- Silence, then a new “case handler.” They rotate contacts to reset the story and extend delays.

- Promises: guaranteed profit, fixed daily returns, no risk.

- Numbers: zero drawdown, perfect fills, spreads that sound free.

- Policies: vague fees, changing terms, bonus withdrawal locks.

- Behavior: urgency, threats, isolation, refusal to confirm in writing.

- Withdrawals: upfront “tax” bills, surprise verification charges, pressure to pay by crypto.

For deeper checks on performance claims, use our guide to reading Myfxbook results.

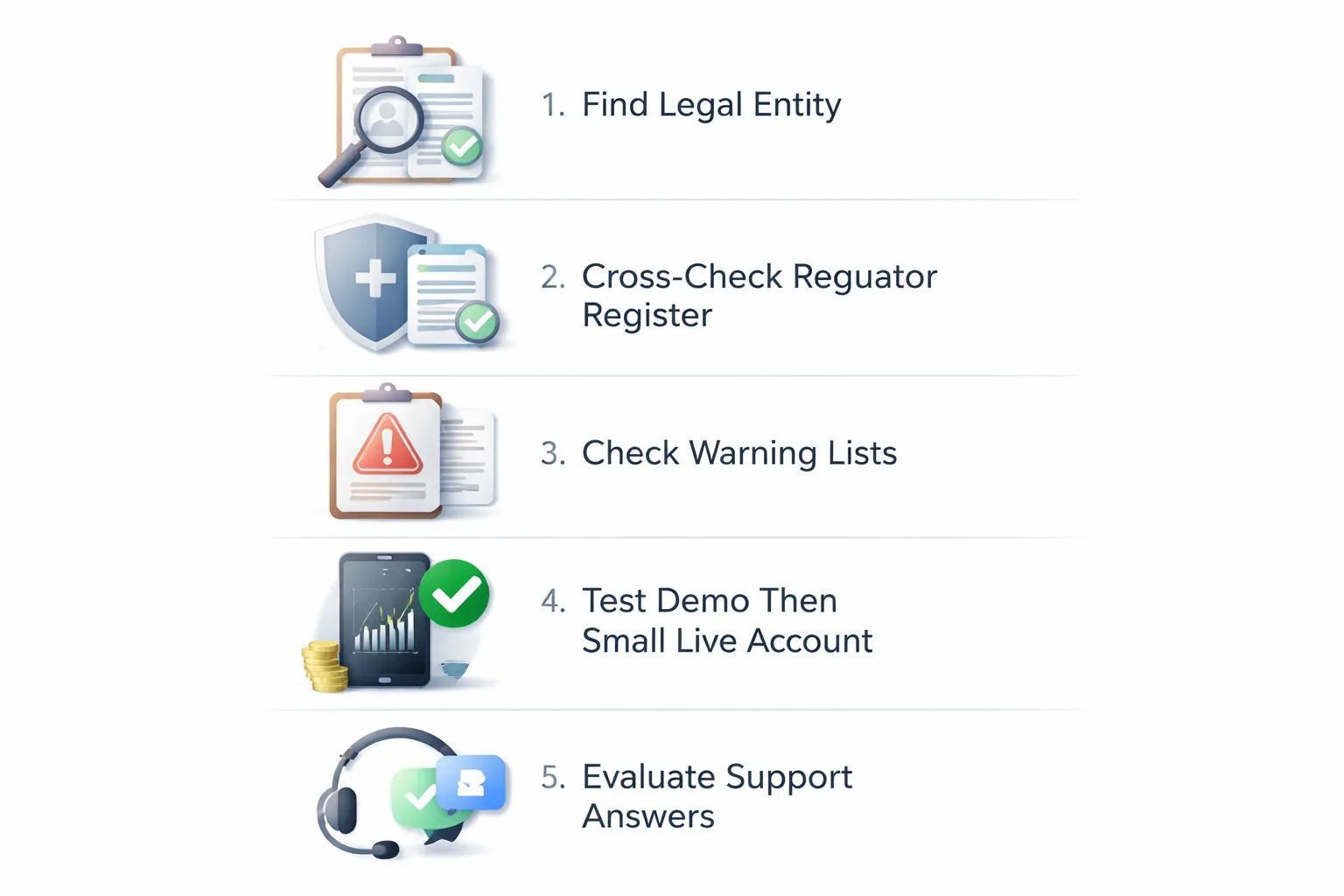

How to verify a broker step-by-step (practical walk-through)

1) Find the legal entity behind the brand

Start with the broker’s own legal disclosures. Do not trust the homepage claims.

- Footer and risk disclosure: scroll to the bottom. Copy the company name, registration number, and the regulator name, if listed.

- Client agreement and product disclosure: open the PDF terms. Find the section that says who you contract with. Save the exact legal entity name and jurisdiction.

- Company address: record the full address, not just a city.

- Group structure: note if the brand lists multiple entities. You must know which one holds your account.

If the documents use a different company name than the website, treat it as a high risk signal.

2) Cross-check domains and contact details against regulator records

Next, confirm that the regulator record matches what the broker shows on its site.

- Use the regulator register: search by legal entity name and license number. Avoid “license lookup” links provided by the broker.

- Match the trading name: the register should list the brand name or “trading as” name.

- Match the website domain: the register often lists approved domains. Your broker’s domain must match exactly. Watch for extra words, hyphens, or different endings.

- Match email and phone: compare support contacts to the register and official company listing.

- Match the address: check the street address, not just the country.

If the regulator record does not list the domain, ask support to confirm in writing which regulated entity owns that domain and holds client accounts. Keep the reply.

3) Check warning lists and investor alerts

Now search for public warnings. Do this even if the broker claims regulation.

- Regulator warning lists: check the regulator in the broker’s claimed country, then check major regulators in your region.

- Consumer agencies: search your country’s financial consumer protection site for alerts.

- Watchdog databases: search by brand name, legal entity name, domain, and phone number.

- Domain history: look for recent domain registration, frequent rebrands, or multiple similar domains.

One warning can be enough to walk away. Multiple warnings mean you stop.

4) Test execution and pricing using a demo, then a small live account

Claims about spreads and fills mean nothing until you test them yourself.

- Demo test: check platform stability, order types, and whether prices match a second data source.

- Live micro test: fund the minimum you can afford to lose. Use bank card or bank transfer, not crypto.

- Measure spreads: record spreads during liquid hours and during news. Compare to what the broker advertises.

- Check slippage and re-quotes: place small market orders and stop orders. Log fill price, requested price, and time.

- Test withdrawal early: withdraw part of your deposit within the first week. Track how long it takes and what documents they demand.

| Test | What to record | Red flag |

|---|---|---|

| Spread check | Spread at fixed times, normal and volatile periods | Spreads far wider than advertised, no explanation |

| Order execution | Requested price, fill price, execution time | Frequent re-quotes, abnormal slippage on small orders |

| Swap and fees | Overnight swap, commissions, inactivity fees | Charges not shown in the fee schedule |

| Withdrawal test | Time to process, extra demands, fees | Upfront “tax” or “verification” fees, delays without dates |

5) Assess support quality with specific pre-sales questions

Support behavior tells you how problems will go later. Ask short, direct questions. Demand written answers.

- All fees: “List every fee that can apply to my account, including inactivity, deposit, withdrawal, conversion, and platform fees.”

- Where funds sit: “Which entity holds client money, and what segregation rules apply?”

- Negative balance protection: “Do you guarantee negative balance protection for my entity and my country?”

- Execution model: “Are you market maker or agency, and where is this stated in the client agreement?”

- Complaints process: “Give the complaints email, postal address, and timeline. Name the external dispute body, if any.”

If they dodge, rush you, refuse to answer in writing, or push crypto funding, you stop. If you trade from the US, also review US forex trading rules and regulators before you open any account.

Safe trading practices that reduce your risk (even with legitimate brokers)

Start small, then prove you can withdraw

Use a minimum viable deposit. Fund the smallest amount that lets you test the platform, spreads, and withdrawals.

- Deposit small: Treat the first deposit as a verification fee, not trading capital.

- Trade light: Place a few small trades to generate normal account activity.

- Withdraw early: Request a partial withdrawal within the first week, then repeat.

- Track timing: Note request time, approval time, and when funds hit your bank or card.

- Watch for friction: Extra “verification,” surprise fees, bonus lockups, and pressure to cancel the withdrawal are hard signals.

A legitimate broker can still be slow. A broker that blocks withdrawals or keeps inventing new steps is a risk you can control by staying small.

Use safer funding methods and avoid irreversible transfers

Pick funding rails that give you records and dispute options. Avoid payment methods that remove your leverage.

- Card deposits: Useful for small tests. You often get better consumer protection than wires.

- Bank transfer to a regulated entity: Use your own named bank account. Match the broker’s legal entity name to the beneficiary.

- Avoid crypto funding: Crypto transfers are hard to reverse. Scammers prefer them for a reason.

- Do not send money to a personal account: No staff member, “account manager,” or “liquidity provider” should receive your funds.

- Do not use remote access tools: If they ask for AnyDesk or TeamViewer to “help fund,” stop.

Account hygiene that blocks takeovers

Most trading losses feel like market risk. Account takeovers look the same until you check your logs. Lock down access.

- Turn on 2FA: Use an authenticator app where possible. Avoid SMS if the broker offers app based 2FA.

- Use unique passwords: One password per broker and per email account. Use a password manager.

- Secure your email: Your email controls password resets. Add 2FA and recovery codes.

- Protect your devices: Update your OS and browser. Use a screen lock. Do not install unknown plugins.

- Avoid public Wi Fi: Do not trade or withdraw on hotel, cafe, or airport networks.

- Check login history: Review IP, device, and session lists if your broker provides them.

Keep a paper trail you can act on

If a dispute happens, you win with documentation. Start collecting it on day one.

- Save the client agreement: Download the full terms, execution policy, and fee schedule.

- Screenshot key pages: Deposit page, withdrawal rules, bonus terms, and any promises made in writing.

- Export chat logs: Download emails and live chat transcripts. Save WhatsApp and Telegram messages as files.

- Keep confirmations: Save deposit receipts, withdrawal requests, and ticket numbers.

- Download statements: Pull monthly statements and full trade history in CSV and PDF.

Store copies outside the broker portal. Use cloud storage plus a local backup.

Risk management that scammers exploit when you ignore it

Scammers push you toward oversized trades, fast deposits, and emotional decisions. Basic risk controls remove their leverage.

- Cap risk per trade: Keep it small and fixed. Many retail traders use 0.5 to 2 percent per trade as a ceiling.

- Limit leverage: High leverage turns normal volatility into margin calls. Use the lowest leverage that fits your strategy.

- Use hard stops: Place a stop loss at entry. Do not widen it to avoid taking a loss.

- Set a daily loss limit: Stop trading after a defined drawdown. No revenge trades.

- Do not average down on margin: Adding to losers can wipe an account fast, especially in news spikes.

- Ignore pressure: “VIP tiers,” deposit deadlines, and recovery promises are sales tactics, not risk controls.

If you want more red flags around coaching, signal sellers, and performance claims, read our forex scams and fake gurus checklist.

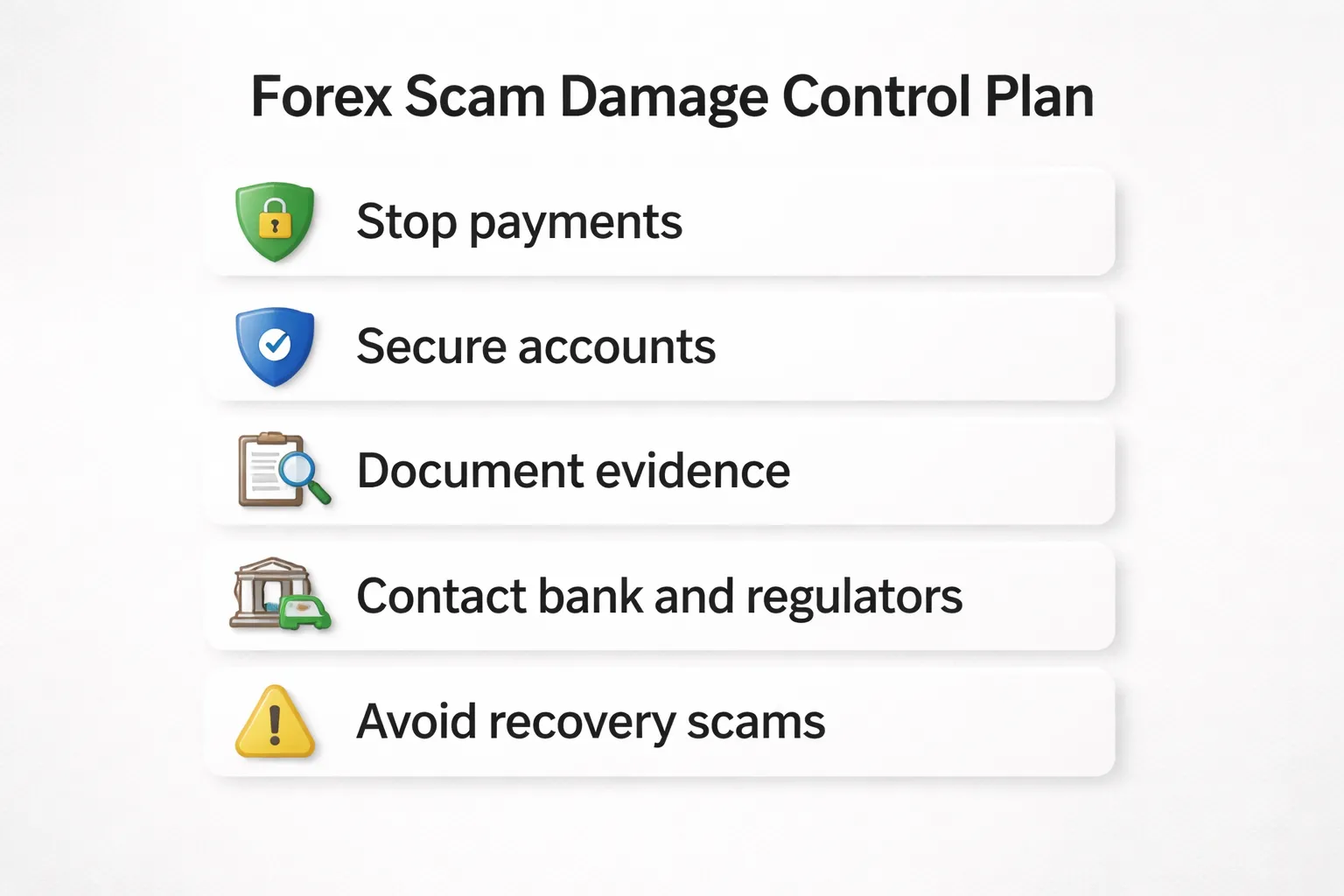

What to do if you suspect a forex scam (damage control plan)

Immediate steps: stop the bleeding

- Stop sending money. Do not “verify” accounts with another deposit. Do not pay “tax,” “insurance,” or “unlock” fees.

- Freeze all access. Change your broker password, email password, and banking app password. Use long, unique passwords.

- Turn on 2FA. Secure your email first. Most account takeovers start there.

- Revoke platform permissions. Remove any API keys. Disable third party apps. Disconnect MetaTrader from unknown servers.

- Remove remote access tools. Uninstall AnyDesk, TeamViewer, and similar apps if the “broker” asked you to install them.

- Lock your cards and accounts. Ask your bank to block future merchant charges and transfers tied to the scam.

- Stop all contact. Block numbers, WhatsApp, Telegram, and email domains. Do not argue. Do not negotiate.

How to document evidence properly

- Build a timeline. Date and time of first contact, deposits, “profits,” withdrawal attempts, and every refusal or new fee demand.

- Save payment proof. Card receipts, bank transfer confirmations, wire MT103 (if available), ACH references, and screenshots of payee details.

- Capture crypto trails. Wallet addresses, transaction IDs (hashes), network used, exchange used, and timestamps. Export CSV if your exchange allows it.

- Export platform records. Account statements, order history, trade IDs, logs, and chat transcripts. Download them, do not rely on web access.

- Record communications. Emails, DMs, call logs, voicemail, and any “terms” they sent you. Screenshot names, handles, and profile links.

- Archive the website. Take full-page screenshots of the homepage, deposit page, withdrawal page, and “regulation” claims. Save the URL and domain.

Who to contact, in order

- Your bank or card issuer. Report fraud. Ask for chargeback options, transfer recall options, and blocks on future payments.

- The relevant regulator. File a complaint where you live and where the broker claims to operate. Use the regulator’s official complaint form.

- Local cybercrime or financial crime unit. Submit a report with your timeline and payment references. Get a case number.

- Hosting and domain abuse contacts. Report the scam domain and web host. Ask them to preserve logs and suspend the site.

- Your crypto exchange. If you sent crypto from an exchange, open a fraud ticket. Ask if they can flag the destination address and share law enforcement guidance.

Do not skip steps because you feel embarrassed. Banks and investigators see this every day. Speed matters.

Chargebacks, recalls, and dispute options

- Card deposits. Ask for a chargeback for “services not provided” or “fraud.” Submit evidence of withdrawal refusal and fee demands. Many issuers impose strict windows, often measured in weeks, not months.

- Bank wire. Ask for a wire recall immediately. Success drops fast once funds hit the recipient bank and move again. Provide the beneficiary name, account details, date, amount, and reference.

- ACH and bank transfer. Ask about dispute procedures for unauthorized or misrepresented transactions. Provide the exact merchant name and transaction IDs.

- Crypto. Treat recovery as low probability unless funds remain on a regulated exchange that can freeze them under a valid request. Still report and document. Address clustering and exchange tags can help investigators later.

Get everything in writing from your bank. Keep ticket numbers, dates, and the name of the agent.

Avoiding recovery-room scams

- Expect a second wave. Scammers sell victim lists. “Recovery agents” then contact you with a promise to get your funds back.

- Watch the playbook. They claim they traced your funds, they show fake case files, they name-drop regulators, they pressure you to act fast.

- They charge upfront. “Legal fees,” “blockchain tracing fees,” “tax clearance,” and “account reactivation” are the same scam in a new wrapper.

- They ask for more access. ID scans, bank logins, remote access tools, or a “test” transaction.

- Your rule. Pay nothing upfront. Verify licensing directly with a regulator. Use a lawyer you find yourself, not one they refer.

If you want to check which regulators apply in your country, use our guide on whether forex trading is legal in the United States and the agencies that oversee it.

Regulation and legal protections explained (without the jargon)

Client money protections (what you get, what you do not)

Regulation matters because it changes where your money sits and what happens if the broker fails.

- Segregated accounts. A regulated broker usually must keep client funds separate from its own operating money. This lowers the risk that your deposit pays the broker’s bills. It does not guarantee you get all your money back.

- Compensation schemes. Some countries run investor compensation funds that can pay you up to a limit if a regulated firm collapses. Coverage, limits, and eligibility vary by country and by entity. Many places offer no payout for forex and CFDs.

- Audit and capital rules. Top tier regulators require minimum capital, reporting, and independent audits. This reduces the odds of a weak broker running on fumes.

What to check before you deposit.

- Which legal entity holds your account, and which regulator licenses that exact entity.

- Where your client money is held, and whether the broker says it uses segregated accounts.

- Whether your country offers a compensation scheme for your product type, and the payout cap.

Negative balance protection and margin closeout rules

These rules control how bad a loss can get when markets move fast.

- Negative balance protection. If your account goes below zero, the broker must bring it back to zero. Without it, you can owe the broker money after a gap or spike.

- Margin closeout rules. Some regulators force brokers to close positions when your margin level drops to a set threshold. This limits runaway losses and reduces the chance you end up in debt.

- Why it matters for retail traders. Retail accounts use leverage. Leverage plus sudden moves can wipe out your balance in seconds. These protections set hard limits on damage.

What to verify.

- Does negative balance protection apply to all clients, or only some regions.

- The broker’s closeout level, and whether it matches local regulatory rules.

- Whether the broker can change leverage or margin requirements during volatility.

Complaints and dispute resolution with regulated brokers

Regulation gives you a process. It does not guarantee you win.

- Step 1, complain to the broker in writing. You submit dates, order IDs, platform logs, and screenshots. You ask for a written final response.

- Step 2, escalate to an external body. Many jurisdictions offer a financial ombudsman, mediation service, or regulator-run complaint channel. They review evidence and timelines. Some can order compensation, others can only recommend outcomes.

- Step 3, enforcement and records. Regulators can fine, restrict, or revoke licenses. They also keep public registers and warning lists. This helps you spot repeat offenders.

How to protect your complaint.

- Save chat logs, emails, call recordings if legal in your area, and full account statements.

- Document every deposit, withdrawal request, and refusal reason.

- Stop sending more money while a dispute runs.

Offshore jurisdictions (what you may lose, how to judge the trade off)

Many scams hide behind offshore registration. Some real brokers also use offshore entities. Your protections often drop either way.

- Weaker client money rules. Segregation may not exist, or enforcement may stay light.

- No compensation scheme. If the broker fails, you may have no backstop.

- Limited dispute options. You may need to sue in a foreign court under foreign law. This costs time and money.

- Looser marketing rules. High leverage, bonuses, and aggressive sales tactics show up more often where rules stay thin.

How to evaluate the trade off.

- Pick the strongest regulated entity the broker offers you, not the one with the highest leverage.

- Confirm the license on the regulator’s register, then match the company name, license number, and website domain.

- Read the legal docs for governing law, dispute venue, and who holds client money.

- Assume offshore means harder withdrawals, harder disputes, and fewer recoveries. Size your deposit for that reality.

If you want a broader red flag list beyond licensing, read our guide on how to spot forex scams and fake gurus.

Quick decision framework: proceed, pause, or walk away

A scoring checklist you can apply in 10 minutes

Score each item. Add points. Use the total to decide.

| Signal | Low risk (0) | Medium risk (+1) | High risk (+2) |

|---|---|---|---|

| Regulator match | License found, name, number, and domain match | License exists, but brand, domain, or entity details look off | No license, “registered” only, or license cannot be verified |

| Client money custody | Segregated client funds, top tier bank named | Segregation claimed, bank not named | No segregation language, or broker “holds” funds in-house |

| Withdrawals | Clear timelines, same-method refund policy, no extra conditions | Vague timelines, manual review language | Bonus turnover blocks, “account must be verified after deposit,” or fees that scale with balance |

| Pricing and costs | Transparent spreads, swaps, commissions, and inactivity fees | Some fees missing, swaps unclear | Hidden fees, no swap table, “zero spread” marketing with no commission detail |

| Leverage and bonuses | Reasonable leverage, no deposit bonus pressure | High leverage offered, bonus available but optional | Extreme leverage, aggressive bonus pushes, “insured profit” claims |

| Sales behavior | No pressure, email support works, written answers | Frequent calls, pushes urgency, avoids specifics | Threats, guilt, “last chance,” asks you to install remote access software |

| Payment methods | Card and bank transfer to the licensed entity | Third party processors, unclear beneficiary | Crypto only, personal accounts, “company wallet,” or changing payee names |

| Performance claims | No guarantees, risk disclosures present | Selective screenshots, vague “proven system” claims | Guaranteed returns, fixed daily profit, or “risk-free” language |

| Online footprint | Long operating history, consistent domains, real staff | Mixed reviews, recent rebrand, unclear ownership | Fresh domain, cloned site reports, many identical complaints about withdrawals |

| Legal docs | Clear governing law, dispute venue, entity name consistent | Docs exist, but conflict with website claims | No legal docs, or docs point to a different company than the one taking deposits |

- 0 to 5 points: Proceed. Use normal risk controls.

- 6 to 12 points: Pause. Do not scale deposits. Run a controlled test.

- 13 to 20 points: Walk away. The downside outweighs any upside.

Deal-breakers that should end the conversation immediately

- No verifiable license for the exact entity and domain taking your deposit.

- They ask for crypto deposits, gift cards, or transfers to a personal name.

- They push remote access tools such as AnyDesk or TeamViewer.

- They guarantee returns or promise fixed daily, weekly, or monthly profit.

- Withdrawals require extra deposits, “tax prepayment,” or “unlock fees.”

- Bonus terms block withdrawals unless you hit high volume targets.

- They refuse written answers and keep everything on calls or chat.

- Entity details change across the footer, terms, invoices, and payment instructions.

- They claim regulation “in process” or show a certificate that does not appear on the regulator register.

One deal-breaker means walk away. Do not negotiate. Do not “try a small amount”.

When uncertainty remains: how to run a controlled test safely

- Use a small test deposit you can lose. Treat it as a fee to verify operations.

- Use a reversible payment method. Prefer card or bank transfer to the licensed entity. Avoid crypto.

- Verify identity before you deposit. If KYC fails later, withdrawals stall.

- Trade small and simple. Open and close a few low-risk positions. Avoid bonuses and promotions.

- Request a partial withdrawal within 24 to 72 hours. Do not wait until you build a larger balance.

- Test support quality. Ask for the exact withdrawal timeline, fees, and the beneficiary name that will appear on the transfer.

- Document everything. Save receipts, chats, emails, and bank references. Screenshot the account page and terms shown to you.

- Scale only after repeat withdrawals. Aim for two successful withdrawals on different days before increasing size.

If they delay, invent new requirements, or change instructions during the test, stop. Withdraw what you can and move on. For a broader pattern checklist, use our forex scam and fake guru safety checklist.

Frequently Asked Questions

What is the biggest red flag for a forex scam?

They block or delay withdrawals. They add surprise fees, KYC demands, or trading volume rules after you request a payout. Stop sending money. Save all chats, emails, and account screenshots.

How do I check if a forex broker is regulated?

Find the broker’s legal entity name and license number. Verify it on the regulator’s official register. Match the website domain and contact details to the register entry. If the license belongs to a different company, treat it as unregulated.

What is a clone broker?

A clone broker copies a real firm’s name or license details to look regulated. The domain, email, or payment details will not match the real firm. Verify the exact URL and entity on the regulator site before you deposit.

Are offshore regulated brokers safe?

Often no. Many offshore licenses offer weak oversight and limited dispute options. You may have no compensation scheme and no enforceable protections. If you use one, keep deposits small and test withdrawals early.

Can a scam broker let you withdraw at first?

Yes. Some pay small withdrawals to build trust. They push you to scale fast, then freeze the account during a larger withdrawal. Follow a strict withdrawal test before you increase size.

What documents should a legit broker provide?

You should see clear terms, fee schedules, risk disclosures, and a client agreement tied to a regulated entity. You should also see segregated funds language and a complaint process. If they refuse written terms, walk away.

What payment methods are highest risk?

Crypto, wire to personal accounts, and third party payment processors carry high risk. You lose chargeback options and clear dispute paths. Prefer card payments or bank transfer to a regulated entity with matching name and address.

What should I do if I already sent money?

Stop deposits. Request withdrawal in writing. Collect proof, receipts, wallet addresses, bank details, and chats. Contact your bank or card issuer fast and ask about chargeback or recall. Report the broker to the regulator and local cybercrime unit.

How can I verify a trader’s track record?

Demand third party verified results with full history. Check deposit and withdrawal activity, leverage, and max drawdown. Avoid screenshots. Use our guide to reading Myfxbook results to spot data tricks.

Why do scammers push “account managers” and WhatsApp groups?

They control the narrative and isolate you from neutral advice. They use urgency, bonuses, and fake social proof to keep you depositing. Legit brokers do not need aggressive chat pressure to keep clients funded.

What is the safest way to test a broker?

Deposit the minimum. Place a few small trades. Withdraw twice on different days. Document every step. If they change rules mid process or delay without clear reasons, stop trading and withdraw what you can.

Conclusion

Conclusion

Most forex scams follow the same pattern. They promise fast returns, push you to deposit more, then block or delay withdrawals.

Use one rule for every broker. Verify regulation first, then test money flow. If you cannot confirm the license on the regulator site, walk away.

- Check the license. Match the broker name, legal entity, domain, and address on the regulator register.

- Control your risk. Start with the minimum deposit. Use a separate email and a new card or bank account if possible.

- Test withdrawals early. Withdraw twice on different days. Keep screenshots, emails, and chat logs.

- Ignore pressure. Do not accept bonuses, VIP tiers, or time limited offers tied to lockups.

- Stop at the first rule change. If fees appear, terms shift, or KYC expands after you request a withdrawal, exit.

Final tip. Treat every deposit like a compliance test. If the broker fails once, do not negotiate. Withdraw what you can, report it to your regulator, and switch to a properly regulated firm.

-

-

- Regulation verification steps, use official registers only

- License clone detection, match the real entity to the brand you use

- Company due diligence, verify the business behind the site

- Platform and trade execution checks, look for patterns that cost you money

- Deposit and withdrawal red flags, follow the money path

- Terms and conditions traps, read what blocks your exit

- KYC and AML misuse patterns, spot the endless loop

- Communication warning signs, demand traceable commitments

- Marketing credibility audit, verify claims outside their ecosystem

- Cybersecurity basics, check the surface area before you sign in

-

- What is the biggest red flag for a forex scam?

- How do I check if a forex broker is regulated?

- What is a clone broker?

- Are offshore regulated brokers safe?

- Can a scam broker let you withdraw at first?

- What documents should a legit broker provide?

- What payment methods are highest risk?

- What should I do if I already sent money?

- How can I verify a trader’s track record?

- Why do scammers push “account managers” and WhatsApp groups?

- What is the safest way to test a broker?

-

-

- Regulation verification steps, use official registers only

- License clone detection, match the real entity to the brand you use

- Company due diligence, verify the business behind the site

- Platform and trade execution checks, look for patterns that cost you money

- Deposit and withdrawal red flags, follow the money path

- Terms and conditions traps, read what blocks your exit

- KYC and AML misuse patterns, spot the endless loop

- Communication warning signs, demand traceable commitments

- Marketing credibility audit, verify claims outside their ecosystem

- Cybersecurity basics, check the surface area before you sign in

-

- What is the biggest red flag for a forex scam?

- How do I check if a forex broker is regulated?

- What is a clone broker?

- Are offshore regulated brokers safe?

- Can a scam broker let you withdraw at first?

- What documents should a legit broker provide?

- What payment methods are highest risk?

- What should I do if I already sent money?

- How can I verify a trader’s track record?

- Why do scammers push “account managers” and WhatsApp groups?

- What is the safest way to test a broker?

-

How to Place a Forex Trade Step by Step (Your First Trade Explained)

2 months ago -

Forex Trading vs Crypto Trading: Which Market Is Better for Beginners?

2 months ago -

Forex Lot Size Calculator: How to Use It to Size Trades Correctly

4 months ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

4 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

4 months ago

-

Is Forex Trading Legal in the United States? Rules, Regulators & What to Know

4 months ago -

Forex Market Hours & Trading Sessions Explained (Best Times to Trade)

4 months ago -

Forex Trading Platforms Comparison: MetaTrader vs cTrader vs TradingView

4 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

4 months ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

4 months ago