What Is Slippage in Forex? Causes, Examples & How to Reduce It

Slippage hits when your forex order fills at a different price than you expected. It can cost you pips, or add pips to your result. You see it most in fast markets, low liquidity, and around news. It also shows up with stop losses, market orders, and large position sizes.

This guide explains what slippage is in forex, how it works, and how brokers execute orders when prices move. You will learn the main causes, clear examples with pip impact, and the difference between positive and negative slippage. You will also get practical ways to reduce it, including order type choices, timing rules, pair selection, and broker settings. If you need a refresher on pip math, see what pips are in forex.

Key Takeaways

In het kort:

- Slippage is the gap between your expected price and your fill price. It shows up in pips.

- You can get positive slippage or negative slippage. Both come from fast price changes between click and execution.

- Slippage rises in high volatility, low liquidity, and around news. It also rises during session opens, closes, and rollovers.

- Market orders fill fast but accept slippage. Limit orders control price but may not fill.

- Wider spreads and thin order books increase pip impact. Exotic pairs and off hours tend to slip more.

- You can reduce slippage with tighter timing, more liquid pairs, and the right order type. You can also use broker tools like max deviation, fill policy, or guaranteed stops if available.

- Track your fills. Log expected price, executed price, spread, and time, then adjust your rules.

Slippage is an execution cost. Treat it like spread and commissions. Add it to your real risk and your real expectancy.

Use market orders when you need a fill more than a price. Use limit orders when price matters more than speed.

If you trade leveraged products, small pip gaps can hit your P and L fast. Review your position sizing and risk rules in our forex leverage guide.

What Is Slippage in Forex (Definition and Why It Happens)

Expected Price vs Executed Price

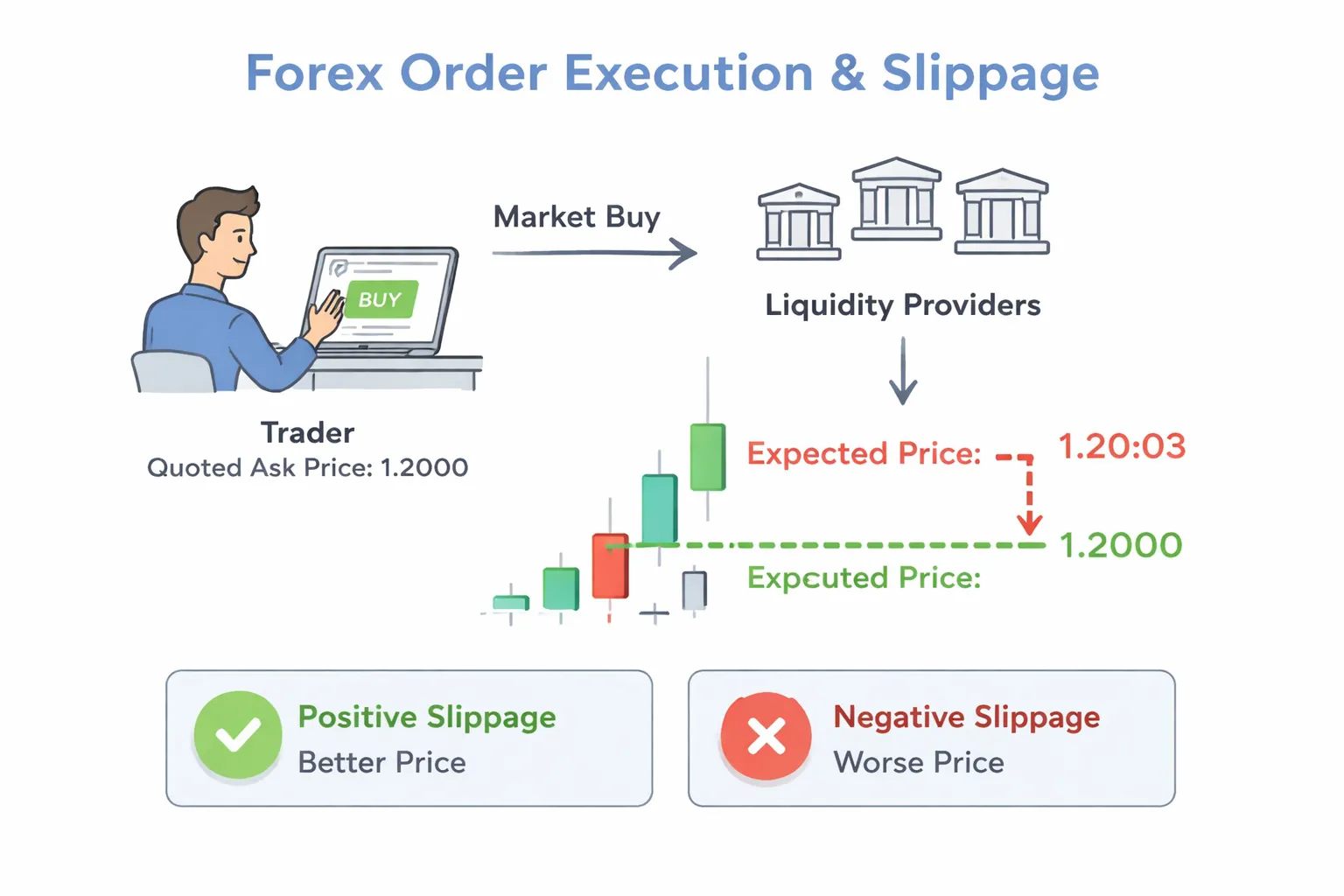

Slippage happens when your order fills at a different price than you expected.

Your expected price usually comes from the quote you see on the platform.

Your executed price is the price your broker can actually trade at when your order hits the market.

The difference between those two prices is slippage. It shows up in pips and in your P and L.

How Order Execution Works

Forex quotes move fast. You see a bid and an ask. Those prices come from liquidity providers and other market participants.

When you place a market order, you ask for the best available price right now. Your broker routes the order to liquidity.

If there is enough liquidity at your requested size, you fill near the quote you saw.

If liquidity thins out or price moves while the order routes, you fill at the next available price level.

This effect gets stronger when you trade larger size, trade during news, or trade less liquid pairs.

Positive vs Negative Slippage

Slippage can help you or hurt you.

- Positive slippage: you buy lower than expected or sell higher than expected.

- Negative slippage: you buy higher than expected or sell lower than expected.

Example. You hit buy at 1.20500 with a market order. You fill at 1.20512. You took 1.2 pips of negative slippage.

Example. You hit sell at 1.20500. You fill at 1.20506. You got 0.6 pips of positive slippage.

Slippage vs Spread vs Requotes

Traders mix these up. They are different costs and behaviors.

| Term | What it is | What you see | When it happens most |

|---|---|---|---|

| Spread | Bid and ask gap | You buy at ask and sell at bid | Always, wider in low liquidity |

| Slippage | Fill price differs from expected price | Execution price prints away from the quote | Fast markets, thin liquidity, large orders |

| Requote | Broker rejects your price and offers a new one | Order does not fill, you must accept a new price | Older dealing desk models, volatile bursts |

Spread is visible before you trade. Slippage is visible after you trade. Requotes block your trade until you accept a new price.

If you want to separate spread from execution quality, learn the basics of how spread works in forex.

Is Slippage “Bad”?

Small slippage is normal. It comes from price movement and limited liquidity at a given level.

Slippage becomes a red flag when it shows a pattern.

- You get mostly negative slippage and rarely positive slippage.

- Slippage spikes on calm sessions on major pairs.

- Fills look worse than the visible market across many trades.

- Stops fill far beyond normal volatility for the same time and pair.

Track it. Log expected price, executed price, order type, time, pair, and size. After 50 to 100 trades, you will see if slippage is random or systematic.

Real-World Slippage Examples (Buy, Sell, Stops, and Gaps)

Market Buy Example, Fast Move During a Data Release

You place a market buy on EUR/USD at 1.10000 right as a CPI number hits. Quotes jump and liquidity pulls. Your broker fills you at the next available price.

| Item | Value |

|---|---|

| Order | Market buy EUR/USD |

| Price you clicked | 1.10000 |

| Executed price | 1.10028 |

| Slippage (pips) | +2.8 pips against you |

This is classic negative slippage. You compete with other orders at the same time. The best ask disappears before your order reaches the market.

Market Sell Example, Thin Liquidity and Wider Price Steps

You place a market sell on GBP/JPY during a thin session. The book shows fewer levels. Prices move in larger steps.

| Item | Value |

|---|---|

| Order | Market sell GBP/JPY |

| Price you clicked | 187.250 |

| Executed price | 187.210 |

| Slippage (pips) | 4.0 pips against you |

On many platforms, GBP/JPY uses 0.01 as one pip. A 0.040 move equals 4.0 pips. Thin liquidity makes this common even without news.

Stop-Loss Example, Stops Turn Into Market Orders at the Trigger

You set a stop-loss to exit a long. Price trades down to your stop. At that moment, your stop triggers and sends a market sell. You do not control the fill price.

| Item | Value |

|---|---|

| Position | Long EUR/USD |

| Stop level | 1.09950 |

| Trigger occurs | Bid touches 1.09950 |

| Executed price | 1.09930 |

| Slippage (pips) | 2.0 pips against you |

You planned your risk at the stop price. Your actual risk uses the fill price. During spikes, the gap between trigger and fill can exceed the candle range you saw when you placed the trade.

Take-Profit and Limit Orders, How Limits Avoid Worse Prices

Limits give you price control. They can still slip, but slippage works in your favor or you get no fill.

- Buy limit: you set the highest price you accept. If the market trades above it, you do not get filled.

- Sell limit: you set the lowest price you accept. If the market trades below it, you do not get filled.

| Order | Limit price | Possible fill | Result |

|---|---|---|---|

| Buy limit EUR/USD | 1.10000 | 1.09995 | Filled, 0.5 pips better |

| Buy limit EUR/USD | 1.10000 | 1.10005 | No fill |

| Sell limit EUR/USD | 1.10500 | 1.10510 | Filled, 1.0 pip better |

| Sell limit EUR/USD | 1.10500 | 1.10490 | No fill |

Take-profit orders often use limit logic. You may miss an exit in a fast reversal. You avoid getting a worse price than you planned.

Weekend and Overnight Gap Example, Price Jumps Over Your Level

Gaps create the worst slippage because there is no trading at your price. Your stop triggers at the first available price after the gap.

| Item | Value |

|---|---|

| Position | Long EUR/USD into weekend |

| Friday close | 1.10020 |

| Stop level | 1.09970 |

| Sunday open | 1.09890 |

| Executed price | 1.09890 |

| Slippage (pips) | 8.0 pips against you |

The market never traded at 1.09970 after the reopen. Your stop could not fill there. Your real exit becomes the first tradable bid.

How to Calculate Slippage in Pips and in Account Currency

Log two prices, expected price and executed price. Use the order direction to label it as better or worse.

- For a buy: slippage (pips) = (executed price minus expected price) divided by pip size.

- For a sell: slippage (pips) = (expected price minus executed price) divided by pip size.

Pip size is usually 0.0001 for most pairs and 0.01 for JPY pairs. If your broker shows fractional pips, adjust for the extra digit. See what pips are in forex if you need a quick refresher.

| Example | Expected | Executed | Pip size | Slippage |

|---|---|---|---|---|

| EUR/USD buy | 1.10000 | 1.10028 | 0.0001 | 2.8 pips worse |

| GBP/JPY sell | 187.250 | 187.210 | 0.01 | 4.0 pips worse |

To convert slippage into account currency, multiply slippage in pips by your position’s pip value.

- Slippage cost = slippage (pips) x pip value (per pip) x number of lots.

| Inputs | Value |

|---|---|

| Slippage | 2.8 pips |

| Pip value | $10 per pip per 1.0 standard lot (example) |

| Size | 0.50 lots |

| Estimated slippage cost | 2.8 x $10 x 0.50 = $14 |

Your pip value changes with pair, account currency, and position size. Use your platform’s pip value readout or trade calculator, then apply the same formula across your log.

Common Causes of Slippage in Forex Markets

Slippage happens when the price you see is not the price you get. That usually comes from fast price moves, thin liquidity, or slow order routing. These are the most common causes in forex.

Macroeconomic news and event risk

High impact releases can move price several pips in milliseconds. Liquidity pulls, spreads widen, and your market order fills at the next available price.

- Non-Farm Payrolls (NFP), unemployment rate, wage growth.

- CPI, core inflation, PPI, inflation surprises.

- Rate decisions, statement changes, press conferences, dot plots.

- Unexpected headlines, central bank comments, geopolitical shocks.

Event risk hits hardest when you trade right at release time or place tight stop orders near price. A 1 to 3 pip “normal” fill can become 10 to 50 pips during peak volatility.

Liquidity conditions: major vs minor vs exotic pairs

More liquidity usually means less slippage. Less liquidity means fewer quotes and bigger jumps between price levels.

- Major pairs like EUR/USD and USD/JPY often slip less in normal conditions.

- Minors can slip more, especially outside their home session.

- Exotics can slip a lot due to wider spreads and thinner order books.

Liquidity also changes by time of day and by broker. You should track slippage by pair, then size your risk with realistic assumptions.

Trading session effects: London and New York overlap vs Asian session

Session timing changes both liquidity and volatility. That changes slippage risk.

- London and New York overlap often brings the deepest liquidity, but also fast moves around US data.

- Asian session often has thinner liquidity for many pairs, which can increase slippage on stops and market entries.

- Session opens can bring quick repricing as liquidity resets.

If you trade outside peak liquidity for your pair, expect worse fills. This matters most for stop-loss orders and breakout entries.

Volatility spikes and quote updates: latency vs price speed

Slippage increases when price moves faster than your order can reach the market.

- Latency adds delay from your platform, internet, VPS, broker servers, and liquidity venues.

- Quote speed changes during volatility. Quotes update faster, but they also change before your order arrives.

- Platform load can slow execution during major events.

Even with low latency, you cannot “beat” a sudden spike. You can only reduce delay and avoid trading when price jumps between levels.

Market gaps and rollovers: end-of-day, weekend, and holiday effects

A gap creates instant slippage because your stop triggers at the first tradable price, not your stop level.

- Weekend gaps often appear after major political or economic news.

- Holiday liquidity drops, so price can jump on small order flow.

- Rollover can bring brief liquidity holes and wider spreads around broker reset time.

Gaps hit stop-loss orders the hardest. You can manage this by reducing exposure into weekends and thin holiday periods.

Order size and partial fills

Bigger orders can move through multiple price levels. That creates average fills worse than the first quote.

- Large tickets may fill in parts across several liquidity providers.

- Thin markets increase the chance of partial fills and wider slippage.

- Stops on big size can slip more during fast drops because the book thins as others exit.

If you scale size up, monitor slippage per lot. Keep a separate log for fills above your typical ticket size.

Execution model factors: dealing desk, STP, ECN, and internalization

Your broker’s execution setup shapes how your order gets filled. It also shapes how often you see requotes, partial fills, or larger slippage.

- Dealing desk brokers can choose to fill internally. They may requote more in fast markets. Slippage can still occur when they cannot hold the quote.

- STP routes orders to external liquidity. Fills depend on available depth and routing quality.

- ECN matches in a pooled market. You can see more variable spreads and more partial fills, especially on size.

- Internalization means the broker fills some flow inside its system. That can improve fills at times, but it depends on their risk and inventory.

Spreads and slippage work together. If spreads widen, slippage risk often rises too. Keep them separate in your tracking. Learn the difference in our spread explanation.

Order Types and Their Slippage Risk (What to Use When)

Market Orders, Highest Fill Chance, Highest Price Risk

A market order prioritizes execution. You ask for a fill now. You accept whatever price the market offers when your order hits the book.

- Slippage risk: High during fast moves, low liquidity, and around session opens and closes.

- Best use: When you must get in or out, like an emergency exit, a hedge, or a hard risk cut.

- Worst use: Thin markets, news spikes, and pairs with wide, unstable spreads.

Limit Orders, Price Control, Fill Uncertainty

A limit order prioritizes price. You set the worst price you will accept. If the market cannot meet it, you do not get filled.

- Slippage risk: Low. The platform should not fill you worse than your limit price.

- Main trade-off: You can miss the trade or get a partial fill, especially on size.

- Best use: Entries at planned levels, mean reversion setups, and markets with normal depth.

- Watch for: Price can touch your level on the chart but still not fill, spreads and last traded price differ.

Stop Orders, Trigger First, Price Second

A stop order turns into a market order after price hits your stop level. That trigger mechanic makes slippage common. When stops fire, many traders hit the market at the same time.

- Slippage risk: High. The stop level triggers the order, it does not guarantee the fill price.

- Best use: Breakout entries and basic stop-loss exits when speed matters more than precision.

- Worst use: High impact news, low liquidity periods, and instruments that gap.

Stop-Limit Orders, Control Your Worst Price

A stop-limit order triggers at the stop price, then places a limit order. You cap your worst fill price. You also accept a higher chance of no fill.

- Slippage risk: Low on price, high on execution risk.

- Main trade-off: Your stop-loss can fail to execute if price jumps past your limit. That can increase losses.

- Best use: Entries where you can tolerate missing the trade.

- Use caution for stop-loss: Only if you can handle the risk of staying in the position during a fast move.

Guaranteed Stop-Loss Orders (GSLOs), Pay for Certainty

A GSLO guarantees your exit price. The broker takes the gap risk. You pay for that insurance.

- Slippage risk: None on the guaranteed level, if the broker honors the guarantee terms.

- Cost: You usually pay a premium, wider spread, added fee, or both. Some brokers refund the premium if it never triggers.

- Availability: Not offered by all brokers. Often limited to certain instruments and account types.

- Limitations: Minimum stop distance, max position size, and restrictions during extreme volatility.

Pending Orders Around News, Triggers Can Behave Differently

News can change how pending orders execute. Spreads can widen, quotes can update in jumps, and the best price can disappear between ticks.

- Stops: Trigger fast and fill worse than expected, because they become market orders into a surge.

- Limits: Can get skipped if price jumps over your level. You may see no fill, or only a partial fill.

- Stop-limits: Often trigger, then fail to fill. That can leave you exposed during the most volatile seconds.

- Practical rule: If you trade news, plan for worse fills. If you cannot tolerate slippage, avoid marketable orders during the release.

| Order type | What you control | Slippage risk | Primary risk | Best for |

|---|---|---|---|---|

| Market | Execution speed | High | Worse price | Fast exits, urgent entries |

| Limit | Price | Low | No fill, partial fill | Planned entries, take profit |

| Stop | Trigger level | High | Worse fill after trigger | Breakouts, basic stop-loss |

| Stop-limit | Trigger and worst price | Low on price | No exit in fast moves | Precise entries, controlled fills |

| GSLO | Exit price | None at guarantee level | Extra cost, broker limits | Gap protection, strict risk caps |

Why Slippage Matters for Traders (Impact on Performance and Risk)

Expected Value and Strategy Edge

Slippage changes your real entry and exit prices. That changes your expected value.

If your strategy targets small gains, a small average slip can wipe out your edge.

| Metric | Without slippage | With 0.2 pip slippage per side |

|---|---|---|

| Average win | 5.0 pips | 4.6 pips |

| Average loss | -5.0 pips | -5.4 pips |

| Win rate | 50% | 50% |

| Expected value per trade | 0.0 pips | -0.4 pips |

That is the core problem. Slippage hits winners and losers, but it hits your net result every time.

Risk Management Distortion

Slippage changes your real stop distance. Your platform stop may say 20 pips. Your fill may turn it into 25 pips.

This matters most when price moves fast. Your stop triggers, then liquidity sits lower. You exit worse than planned.

- Your risk per trade increases. A 20 pip stop with 5 pips slippage becomes 25 pips of price risk.

- Your position size becomes wrong. You sized for the planned stop, not the filled stop. Read position sizing if you want the math.

- Your R multiple shifts. Your 1R loss becomes 1.25R. Your stats look fine on paper, then drift live.

Slippage can also distort take-profit fills. You may miss a limit fill by a fraction of a pip in fast reversals, then watch price run away.

Scalping and High-Frequency Sensitivity

Short timeframes feel slippage the most. Your targets are small. Your trade count is high.

- Small targets. If you aim for 3 to 8 pips, 0.3 to 1.0 pip of slippage is a large percentage of the move.

- More executions. More trades means more times you pay the slippage cost.

- News spikes. Scalpers often trade around volatility. That is where slippage clusters.

For scalping, average slippage matters. Worst-case slippage matters more. One bad fill can erase many small wins.

Position Trading Perspective

Slippage matters less when your targets and stops are wide.

- Lower percentage impact. A 1 pip slip on a 200 pip move barely changes the outcome.

- Fewer entries and exits. You execute less often, so you face slippage less often.

- Higher exposure to gaps. Weekend gaps and major event gaps can still create large slippage on stops.

If you hold through major releases, your main risk is the rare large slip, not the small average slip.

Backtesting vs Live Trading

Backtests often assume perfect fills. Live trading never gives you that.

- Add a slippage model. Apply a fixed cost per side, then stress test with higher values during news.

- Use asymmetric assumptions. Model more negative slippage than positive. Your broker may pass price improvement, but you should not rely on it.

- Model stop slippage separately. Stops slip more than limits in fast markets. Use a larger assumption for stop orders.

- Check sensitivity. Re-run results with 0.1, 0.3, 0.5, and 1.0 pip per side to see where your edge breaks.

If your strategy fails with small execution costs, it has no buffer. You will feel that fast in real money trading.

How to Reduce Slippage in Forex (Practical Checklist)

Slippage never disappears. You control how often it hits, and how hard.

Trade the most liquid pairs and times

- Stick to majors. EURUSD, USDJPY, GBPUSD, USDCHF, USDCAD, AUDUSD, NZDUSD. They usually show tighter spreads and deeper liquidity.

- Trade session overlap. London, and London to New York overlap. You often get more volume and cleaner fills.

- Avoid thin hours. Late New York, early Asia, and holidays. Liquidity drops, spreads widen, and slippage rises.

- Know pair behavior. Crosses and exotics can gap and spike more, even on normal headlines.

Avoid high-impact news windows, or size down and widen parameters

- Do not trade into red-flag events. CPI, NFP, FOMC, rate decisions, central bank speeches. Most retail fills get worse in the first seconds.

- Use a time buffer. Many traders avoid 5 to 15 minutes before and after the release. If you must trade, test your own buffer by pair and broker.

- Cut size first. If you trade anyway, reduce position size. Thin books cannot absorb normal size without price movement.

- Widen stops and targets. Tight levels trigger more orders and more slip in spikes. Wider parameters reduce churn.

Prefer limit orders for entries when price precision matters

- Use limits to cap entry price. A buy limit will not fill above your price, a sell limit will not fill below your price.

- Accept missed trades. Limits protect price but increase non-fills in fast moves.

- Use limits for mean reversion entries. If your edge depends on exact entry, market orders can erase it.

- Watch for partial fills. Limits can fill in pieces. Track your average fill price, not the first fill.

Use stop-limit or GSLOs when controlling worst-case loss is critical

- Know what a stop does. A stop triggers a market order. In a spike, it can fill far away.

- Use stop-limit to cap slippage. You set a stop price and a worst fill price. Risk: you may not exit.

- Use GSLO where offered. A guaranteed stop locks the maximum loss. You pay for that protection, often via a wider spread or an explicit premium.

- Match tool to the risk. If a gap would break your account, pay for the guarantee or cut exposure.

Adjust position sizing to market depth

- Reduce size in thin liquidity. Smaller size usually means less market impact and fewer bad fills.

- Scale size by spread and volatility. When spreads widen or ATR rises, cut your lot size.

- Know your units. Use consistent sizing rules tied to your lot size, your stop distance, and current market conditions.

Set realistic stop-loss placement

- Avoid obvious levels in volatile periods. Round numbers, session highs and lows, and prior day extremes attract stop runs.

- Give the trade room that matches volatility. If your stop sits inside normal noise, you will trigger often, and you will pay slippage on exits.

- Separate strategy stop from disaster stop. Some traders use a wider hard stop for tail events, and a tighter exit rule for normal conditions. Test both costs.

Monitor spreads and depth-of-market (DOM) where available

- Track live spread. If spread expands beyond your tested range, skip the trade. Your expected slippage usually rises too.

- Watch liquidity cues. On platforms that show DOM or liquidity bands, avoid entries when the book looks thin near your price.

- Log execution stats. Save fill price, requested price, time, pair, and spread. Review by session and event type.

Use VPS and low-latency setup for time-sensitive strategies

- Use a VPS near your broker server. It reduces network delay and dropped connections.

- Keep your platform stable. Avoid heavy indicators, unstable plugins, and Wi-Fi. Execution issues often look like slippage.

- Be realistic. Latency helps most for scalping and fast breakout systems. It will not fix trading through news spikes.

Split orders and scale in and out to reduce single-fill risk

- Break large orders into smaller clips. One big market order can sweep the book. Several smaller orders often average better.

- Scale into entries. You reduce the chance that one bad fill ruins the trade.

- Scale out exits. You lower dependence on one fill during fast reversals.

- Measure the trade-off. More tickets can raise commissions. Compare average fill improvement versus added costs.

| Goal | Best tool | Main trade-off |

|---|---|---|

| Control entry price | Limit order | Missed or partial fills |

| Exit fast in a crash | Stop market | Higher slippage risk |

| Cap worst fill on exit | Stop-limit | No fill in a gap |

| Hard cap worst-case loss | GSLO | Extra cost, limited availability |

| Lower fill risk in thin markets | Smaller size, split orders | More complexity, possible higher fees |

Choosing a Broker to Minimize Slippage (Execution Quality and Transparency)

Key execution metrics to look for

Spreads matter. Execution quality matters more when price moves fast. Ask for numbers. Compare brokers on the same account type and instrument.

- Fill speed, measured in milliseconds. You want consistent execution, not rare “best case” claims.

- Price improvement rate. A broker should sometimes fill you better than requested, not just worse.

- Rejection rate. High rejection rates often show weak liquidity access or aggressive risk controls.

- Requote frequency, if the broker uses instant execution. Requotes often rise in news and gaps.

- Market impact by size. Test small, then larger lots. Slippage often scales with order size in thin conditions.

Slippage policy and reporting

Reputable brokers explain how they handle slippage and show it in trade reports. You need proof, not marketing lines.

- Clear order handling rules. Market orders can slip both ways. Stop orders trigger, then fill at the best available price.

- Symmetric slippage. The broker should pass positive and negative slippage, based on market conditions.

- Execution method disclosure. Look for details on market execution, liquidity sources, and how orders route.

- Post trade reporting. You should see requested price, executed price, time stamp, and any partial fills.

- Complaints and dispute process. The policy should state how you can challenge abnormal fills.

Regulation and trust signals

Execution integrity depends on oversight. Regulation does not remove slippage. It reduces the chance of abusive handling.

- Top tier licensing. Verify the license number on the regulator site, not just on the broker footer.

- Best execution standards. Some regulators require brokers to take reasonable steps to get good outcomes.

- Segregated client funds. It does not fix fills. It lowers the risk of broker failure.

- Audited reporting and governance. Stronger controls reduce hidden dealing practices.

Demo vs live differences

Demo results often look clean. Live trading includes real liquidity, real queue priority, and real risk checks.

- Demo fills can be idealized. Many demos fill at the quoted price with low latency.

- Live accounts face liquidity limits. During news, quotes change before your order reaches the market.

- Risk controls can slow fills. Some brokers add checks that only apply to live accounts.

- Test with small size. Track slippage over at least 50 to 100 trades, across calm and volatile sessions.

Red flags to avoid

- Frequent requotes during normal market conditions.

- Asymmetric slippage, you get negative slippage often, you rarely see price improvement.

- Vague execution claims with no metrics, no reports, and no audit trail.

- Abnormal fill patterns around stops, repeated stop fills far outside typical spread moves without matching market evidence.

- Pressure to trade during major news while disclaiming responsibility for execution quality.

Questions to ask broker support

- What is your median and 90th percentile execution time for this account type, on major pairs?

- Do you pass positive slippage on market and stop orders? Can you show a report sample?

- What is your order rejection rate in volatile periods?

- Do you use last look with liquidity providers? If yes, how often do orders get rejected due to last look?

- How do you handle partial fills on larger orders?

- Where are your trading servers located, and do you support VPS or FIX API for lower latency?

- Can you provide execution quality statistics by instrument and time of day?

- What triggers a trade review, and how do you investigate disputed fills?

| What to check | What you want to see | Why it matters |

|---|---|---|

| Execution time | Stable median, transparent percentiles | Reduces slippage from fast quote changes |

| Price improvement | Documented positive and negative outcomes | Signals fair routing and handling |

| Rejections and requotes | Low rates, explained causes | Shows liquidity quality and fewer forced retries |

| Reporting detail | Time stamps, requested vs executed price | Lets you audit slippage yourself |

| Regulation | Verifiable license and best execution framework | Reduces execution abuse risk |

If slippage pushes you closer to forced liquidation, read our guide on margin call vs stop out and set risk limits that account for worse fills.

Slippage vs Other Trading Costs (Putting It in Context)

Spread, Commission, and Swap vs Slippage

Some costs show up before you click buy or sell. Slippage shows up after.

- Spread: The bid ask gap. You see it up front. It changes with volatility and liquidity, but you can estimate it before entry.

- Commission: A fixed fee per lot or per side on many accounts. You can calculate it exactly if you know your trade size. Use your lot size to convert it into money cost.

- Swap: Overnight financing. It depends on the pair, your direction, and broker rates. You can check the swap table before you hold a position past rollover.

- Slippage: The gap between the price you request and the price you get. You only know it after execution. It spikes during news, session opens, thin liquidity, and fast moves.

Why Low Spreads Do Not Guarantee Low Slippage

Spreads and slippage come from different problems.

- Spread is a quote. It reflects current pricing at the top of book.

- Slippage is a fill. It reflects what liquidity actually existed when your order hit the market.

- Low spread can vanish fast. A tight quote can widen or disappear in milliseconds during a spike.

- Market orders pay the real-time market. If price jumps, you get the next available price, not the last visible quote.

- Stops can slip even on tight spreads. A stop becomes a market order once triggered. It can fill far from the trigger if price gaps or sweeps liquidity.

Judge execution with fill data, not a marketing screenshot of minimum spreads.

Total Cost Framework: Estimating All-In Execution Cost Per Trade

Track your cost in pips and in money. Use the same framework for every trade.

- Spread cost (pips): average spread at entry time.

- Commission cost (pips): round-turn commission converted to pips for your trade size.

- Slippage (pips): executed price minus requested price. Track it separately for entry and exit.

- Swap (pips): only if you hold through rollover.

All-in cost (pips) per round trip: spread + commission + entry slippage + exit slippage + swap.

| Cost component | When you know it | How predictable it is |

|---|---|---|

| Spread | Before entry | Medium, varies by time and volatility |

| Commission | Before entry | High, fixed schedule |

| Swap | Before holding overnight | Medium, can change with broker rates |

| Slippage | After execution | Low, depends on market conditions and order type |

When Better Fills Happen: Price Improvement

Slippage can work in your favor. Brokers may call it price improvement.

- It happens when price moves toward you between order submission and execution.

- It shows up more in limit orders that rest and get filled at your price or better.

- It shows up less in stops and market orders during fast moves, because they must fill immediately.

- It is not guaranteed. Some brokers pass improvements through. Some internalize flow. Some apply asymmetric execution rules.

Log requested vs executed price for every trade. Calculate average slippage by pair, session, and order type. Then decide where your setup actually works.

Frequently Asked Questions

What is slippage in forex?

Slippage is the gap between your requested price and your executed price. It can be positive or negative. It happens when the best available price changes before your order fills, usually during fast moves or thin liquidity.

Is slippage the same as spread?

No. Spread is the bid ask gap you see before you trade. Slippage is a change between the price you requested and the price you got. You can pay spread with zero slippage, or get slippage even on tight spreads.

Do limit orders get slippage?

Proper limit orders should not fill worse than your limit. If price moves away, you get no fill. You can still see positive slippage if the broker improves your fill. Watch for partial fills during low liquidity.

Do stop losses always get slippage?

No. Stops become market orders when triggered. In fast markets, the next available price can be far from your stop level. You see it most during news spikes, weekend gaps, and session opens.

Is slippage always bad?

No. You can get price improvement. Many traders never measure it, so they miss the real cost. Track requested vs executed price, then compute average slippage by pair, session, and order type.

What causes slippage in forex?

Low liquidity, rapid price changes, and order size versus available depth. News releases, rollovers, and session transitions amplify it. Broker execution rules matter, including whether they pass through positive slippage or skew outcomes.

Which pairs and times have the least slippage?

Major pairs during the London and New York overlap tend to slip less. Exotic pairs and off hours slip more. Use your own trade log. Compare slippage by trading session and avoid thin windows.

How can you reduce slippage?

Trade liquid pairs, cut size, and avoid major news minutes. Use limit entries when you can. Place stops at levels that account for volatility. Choose brokers with transparent execution stats. Time your trades around known session changes.

What is a requote, and how is it different?

A requote is a broker rejecting your requested price and offering a new one, common on instant execution models. Slippage is a fill at a different price without asking again. Market execution tends to slip, not requote.

How do you measure slippage in pips?

Slippage in pips equals executed price minus requested price, converted to pips. Keep the sign. Negative means worse fill. Positive means improvement. Export trade data, then average by symbol, time of day, and order type.

Can slippage cause stop hunting?

Slippage does not prove stop hunting. It often comes from liquidity gaps and fast price moves. If you see one sided slippage across many trades, test another broker and compare execution reports and fill distributions.

Does slippage matter more for scalping?

Yes. Small targets make slippage a larger share of expected profit. If your average slippage plus spread approaches your average win, your edge disappears. Use tight execution filters and track results by timeframe.

Where can you learn the basics before worrying about slippage?

Start with order types, spreads, and execution basics. Read what is forex trading, then return to slippage with a trade log and real fill data.

Conclusion

Conclusion

Slippage is the gap between your expected price and your fill. You cannot remove it. You can measure it and control its impact.

- Track it. Log expected price, fill price, spread, pair, session, and news context. Review slippage in pips and in dollars per trade.

- Trade liquid markets. Focus on major pairs and active sessions. Avoid thin hours and obvious liquidity gaps.

- Control risk. Cut position size when volatility rises. Keep stops realistic for the current ATR. Tight stops in fast markets invite bad fills.

- Use execution rules. Prefer limit orders for entries when you can. Use market orders only when you accept uncertain fills. Add a max slippage setting if your platform supports it.

- Filter events. Skip or reduce exposure around high impact releases. Spreads widen and fills degrade.

Final tip. Treat slippage like a trading cost. If your average slippage plus spread starts to approach your average win, change one variable fast, pair, time, order type, or size, then re-test with new fill data.

High leverage makes slippage hurt more because it magnifies small execution errors into large P and L swings. Read how forex leverage works and set size limits that still hold up when fills get worse.

-

Forex Market Hours & Trading Sessions Explained (Best Times to Trade)

4 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

4 months ago -

What Is a Lot Size in Forex? Lot Types + Quick Examples

4 months ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

4 months ago -

What Are Pips in Forex? Definition, Examples & Why They Matter

4 months ago

-

-

- Market Buy Example, Fast Move During a Data Release

- Market Sell Example, Thin Liquidity and Wider Price Steps

- Stop-Loss Example, Stops Turn Into Market Orders at the Trigger

- Take-Profit and Limit Orders, How Limits Avoid Worse Prices

- Weekend and Overnight Gap Example, Price Jumps Over Your Level

- How to Calculate Slippage in Pips and in Account Currency

-

- Macroeconomic news and event risk

- Liquidity conditions: major vs minor vs exotic pairs

- Trading session effects: London and New York overlap vs Asian session

- Volatility spikes and quote updates: latency vs price speed

- Market gaps and rollovers: end-of-day, weekend, and holiday effects

- Order size and partial fills

- Execution model factors: dealing desk, STP, ECN, and internalization

-

- Trade the most liquid pairs and times

- Avoid high-impact news windows, or size down and widen parameters

- Prefer limit orders for entries when price precision matters

- Use stop-limit or GSLOs when controlling worst-case loss is critical

- Adjust position sizing to market depth

- Set realistic stop-loss placement

- Monitor spreads and depth-of-market (DOM) where available

- Use VPS and low-latency setup for time-sensitive strategies

- Split orders and scale in and out to reduce single-fill risk

-

- What is slippage in forex?

- Is slippage the same as spread?

- Do limit orders get slippage?

- Do stop losses always get slippage?

- Is slippage always bad?

- What causes slippage in forex?

- Which pairs and times have the least slippage?

- How can you reduce slippage?

- What is a requote, and how is it different?

- How do you measure slippage in pips?

- Can slippage cause stop hunting?

- Does slippage matter more for scalping?

- Where can you learn the basics before worrying about slippage?

-

-

- Market Buy Example, Fast Move During a Data Release

- Market Sell Example, Thin Liquidity and Wider Price Steps

- Stop-Loss Example, Stops Turn Into Market Orders at the Trigger

- Take-Profit and Limit Orders, How Limits Avoid Worse Prices

- Weekend and Overnight Gap Example, Price Jumps Over Your Level

- How to Calculate Slippage in Pips and in Account Currency

-

- Macroeconomic news and event risk

- Liquidity conditions: major vs minor vs exotic pairs

- Trading session effects: London and New York overlap vs Asian session

- Volatility spikes and quote updates: latency vs price speed

- Market gaps and rollovers: end-of-day, weekend, and holiday effects

- Order size and partial fills

- Execution model factors: dealing desk, STP, ECN, and internalization

-

- Trade the most liquid pairs and times

- Avoid high-impact news windows, or size down and widen parameters

- Prefer limit orders for entries when price precision matters

- Use stop-limit or GSLOs when controlling worst-case loss is critical

- Adjust position sizing to market depth

- Set realistic stop-loss placement

- Monitor spreads and depth-of-market (DOM) where available

- Use VPS and low-latency setup for time-sensitive strategies

- Split orders and scale in and out to reduce single-fill risk

-

- What is slippage in forex?

- Is slippage the same as spread?

- Do limit orders get slippage?

- Do stop losses always get slippage?

- Is slippage always bad?

- What causes slippage in forex?

- Which pairs and times have the least slippage?

- How can you reduce slippage?

- What is a requote, and how is it different?

- How do you measure slippage in pips?

- Can slippage cause stop hunting?

- Does slippage matter more for scalping?

- Where can you learn the basics before worrying about slippage?

-

How to Place a Forex Trade Step by Step (Your First Trade Explained)

2 months ago -

Forex Trading vs Crypto Trading: Which Market Is Better for Beginners?

2 months ago -

Forex Lot Size Calculator: How to Use It to Size Trades Correctly

4 months ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

4 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

4 months ago

-

Is Forex Trading Legal in the United States? Rules, Regulators & What to Know

4 months ago -

Forex Market Hours & Trading Sessions Explained (Best Times to Trade)

4 months ago -

Forex Trading Platforms Comparison: MetaTrader vs cTrader vs TradingView

4 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

4 months ago -

What Is a Lot Size in Forex? Lot Types + Quick Examples

4 months ago