Forex Taxes in the US: Section 988 vs 1256 (Complete Guide)

Forex profits in the US do not all face the same tax treatment. Two IRS rules drive most outcomes, Section 988 and Section 1256. The difference can change your tax rate, your ability to deduct losses, and how you report trades.

This guide breaks down how each section works for spot forex, forex options, and currency futures. You will learn when gains count as ordinary income versus capital gains, how losses get limited or fully deductible, and which traders can use the 60/40 split under Section 1256. You will also learn how the Section 988 election works, when you must file it, and what records you need to support it.

If you need a rules primer before taxes, read Is Forex Trading Legal in the United States?.

Key Takeaways

- In het kort:

- Most spot forex gains and losses fall under Section 988, you report them as ordinary income or loss.

- Ordinary loss under Section 988 can offset wages, interest, and other income, it does not face the capital loss cap.

- Section 1256 applies to certain regulated futures and some FX contracts, it uses the 60/40 split, 60 percent long term and 40 percent short term, no matter how long you held the position.

- Section 1256 also uses mark to market at year end, you recognize open P and L each tax year.

- Your best tax outcome depends on your profile, high income years can favor the 60/40 treatment, drawdown years often favor ordinary loss.

- If you want capital gain treatment for eligible FX trades, you may need a Section 988 election, timing matters, you must make it on time and keep proof.

- Keep clean records, trade confirmations, broker statements, year end positions, and a method for translating amounts into USD.

- If a broker offer or “tax free” pitch feels off, use this forex scam safety checklist before you fund an account.

Forex taxes in the US: what traders are actually taxed on

How the IRS defines “foreign currency transactions” in plain English

The IRS taxes you on gains and losses that come from changes in exchange rates, when the underlying amount is in a currency that is not your “functional currency.” For most US traders, your functional currency is USD.

A “Section 988 transaction” is a transaction where you pay, receive, or measure an amount in a non-USD currency. In retail FX, that often means your profit or loss depends on a currency pair moving, even if you never take delivery of currency.

Two practical points matter.

- If your broker account is in USD, you still have foreign currency exposure. The tax result follows the instrument and how it references currency, not the account label.

- The IRS cares about realized results. Open trade swings can change your equity, but they usually do not change your taxes until you close or otherwise realize the position.

Common retail products and why the tax rules differ

Retail traders use several products that look similar on a platform. The tax code does not treat them the same.

- Spot FX (including retail “rolling spot”). Often treated under Section 988 by default, with ordinary gain or loss, unless you make a valid election out where allowed.

- Forwards and swaps. These can fall under Section 988, but the details depend on the contract terms, how it settles, and whether it qualifies for different treatment.

- Options on currency. Many currency options fall under Section 988. Some exchange-traded currency options can fall under Section 1256.

- Currency futures. Regulated futures contracts typically fall under Section 1256. That brings the 60/40 split and mark-to-market rules.

Why the split matters. Section 988 generally creates ordinary income or loss. Section 1256 generally creates a blend of long-term and short-term capital treatment, and it marks positions to market at year-end. That difference changes rates, loss limits, and how cleanly results flow onto a return.

Taxable events you need to track

You do not get taxed on every tick. You get taxed on specific events.

- Closing a trade. You realize gain or loss when you close all or part of a position.

- Expiration, assignment, exercise. Options create realized events when they expire, get exercised, or get assigned.

- Year-end mark-to-market for Section 1256. If your product qualifies for 1256, you treat open positions as sold at fair market value on the last trading day of the year, then you start the next year with a new basis.

- Rollover and swap. “Rollover” in retail FX usually shows up as swap or financing. You must treat it as part of your taxable results. Depending on how your broker reports it, it may appear as interest, as a fee, or folded into trade P&L.

- Interest and financing charges. These can include margin interest, borrow fees, or platform financing. You need to categorize them correctly because the label on a statement does not control the tax treatment.

Track realized versus unrealized clearly.

- Realized P&L comes from closed trades and realized option events. This usually drives what you report.

- Unrealized P&L sits on open positions. You generally do not report it unless mark-to-market rules apply to your product.

Why broker statements often do not match tax reporting needs

Broker statements help you manage an account. They often fail as tax workpapers.

- They mix categories. Many statements net trading P&L, commissions, and swap into one number. Your tax return may need them separated.

- They use broker labels, not tax labels. A broker may call something “swap,” “rollover,” “interest,” or “fee.” You still must map it to the right tax category.

- They do not handle Section 988 versus 1256 correctly. A platform can show all FX products in one ledger even though some contracts may qualify for 1256 and others do not.

- They do not give clean USD translation. The IRS expects US taxpayers to report in USD. If parts of the ledger post in a non-USD currency, you need a consistent conversion method and supporting rates.

- They do not show election timing. Your statement will not prove you made a valid Section 988 election out, or when you made it. You must keep that proof yourself.

If you want to sanity-check performance stats against what you can actually substantiate from statements and fills, use this guide to how to read Myfxbook results.

Section 988 explained (ordinary income/loss treatment)

What counts as a Section 988 transaction

Section 988 covers many gains and losses that come from amounts set, paid, or received in a nonfunctional currency. For most U.S. retail traders, that means forex gains and losses that settle in a currency other than the U.S. dollar.

- Spot forex trades. Most retail spot FX trading falls here by default.

- Forex forwards and rolling spot contracts. If your broker structure functions like a forward or rolling settlement, Section 988 often applies.

- Non-equity options on foreign currency. Many FX options can fall under Section 988 unless another rule overrides, or you make a valid election where allowed.

- Foreign-currency denominated items. Certain FX gains and losses tied to receivables, payables, or cash accounts can qualify when you translate into your functional currency.

What usually does not fall under Section 988 are instruments that already have their own tax regime. Regulated futures contracts and many exchange-traded options often land under Section 1256 instead. Broker statements alone may not clearly label this. You need to know what you traded.

Ordinary character, what it means for your tax bill

Section 988 gains and losses are ordinary by default. That means your net profit generally taxes at your ordinary income rates, not long-term capital gains rates.

- Short holding periods do not matter. You do not get long-term capital gains rates under default 988 treatment.

- Ordinary gains add to your taxable income like wages, interest, or business income.

- Ordinary losses reduce ordinary income, subject to general limits and your facts, such as trader vs investor status and other activity rules.

Loss treatment, the main practical advantage

The big draw of Section 988 is how it treats losses. Ordinary losses can offset ordinary income without the strict capital loss limits that apply to capital assets.

- Capital loss limitation. Capital losses generally face an annual limit against ordinary income, with the rest carried forward.

- Section 988 ordinary loss. It can offset ordinary income more directly, which matters if you have salary, business income, or interest income.

This is why many active spot FX traders prefer default Section 988 treatment when they expect volatility or drawdowns.

Sourcing rules, U.S. source vs foreign source

Section 988 also has sourcing rules. Source matters because it can affect foreign tax credits, how you report cross-border activity, and how certain U.S. tax rules apply when you trade through foreign brokers or have foreign ties.

- U.S. source. Income treated as U.S. source generally sits fully inside the U.S. tax net.

- Foreign source. Foreign source income may interact with foreign tax credits and other international reporting and limitation rules.

For many U.S. retail traders trading from the U.S., sourcing may not change the final number on your return, but it can change how you support it and how it nets against other items. Keep clean records of where you reside, where you trade, and which entity holds the account.

Interest, carry, swaps, and financing components

Retail forex results often include financing. Your broker may label it swap, rollover, or interest. Do not treat it as the same thing as trade P and L without checking how your statement reports it.

- Carry and swap credits or debits usually track the interest rate differential and the broker financing charge.

- Cash interest on account balances can show up separately from trading gains and losses.

- Fees such as commissions and platform charges generally reduce your trading profit, but your reporting method must match your records.

You need to map each line item to its tax character. If your broker bundles swap into the trade result, you still need a consistent approach. If you use an Islamic or swap-free account, the broker may replace swap with another charge. That can change how your costs show up on statements. See Islamic accounts and swap-free trading explained.

Section 1256 explained (60/40 blended capital gains treatment)

Section 1256 explained (60/40 blended capital gains treatment)

Section 1256 is a special tax rule for certain exchange-traded derivatives. It can apply to some FX-related products, but it usually does not apply to spot forex trades you place with a retail FX broker.

Which contracts typically qualify

- Regulated futures contracts, including many currency futures traded on U.S. exchanges.

- Nonequity options on broad-based indexes and other qualifying underlying assets, including some currency-related options when traded on a qualified exchange.

- Exchange-traded FX products, like certain FX futures and listed options tied to currencies.

Most OTC retail forex, including typical spot and rolling spot positions, falls under Section 988 by default. Section 1256 treatment usually shows up when you trade FX through listed, cleared products.

The 60/40 rule (blended capital gains treatment)

Section 1256 uses a fixed split for gains and losses, no matter how long you held the position.

- 60% of net Section 1256 gain or loss counts as long-term capital gain or loss.

- 40% counts as short-term capital gain or loss.

This matters because long-term capital gains rates can be lower than ordinary income rates. The split applies even if you opened and closed the position in the same day.

Mark-to-market at year-end (timing changes)

Section 1256 contracts are marked to market at year-end. You treat open positions as if you sold them at fair market value on the last business day of the tax year.

- You recognize gains and losses for the year even if you did not close the trade.

- Your next tax year starts with a new “tax basis” equal to that year-end value.

- Your broker statements for futures often support this, but you still need your own records to match totals and dates.

Mark-to-market changes tax timing. It can pull taxes forward in a winning year, or pull losses forward in a losing year.

Netting rules and how 1256 losses interact with other capital gains and losses

You net your Section 1256 contracts together for the year, then apply the 60/40 split to the net result. That net capital gain or loss then flows into your broader capital gain and loss calculation.

- Section 1256 results can offset other capital gains.

- If you end up with a net capital loss, you face the normal capital loss limits and carryforward rules.

- You track Section 1256 separately from ordinary income items because the character differs.

What “regulated” and “exchange-traded” mean for retail traders

In practice, “regulated” and “exchange-traded” means the contract trades on a recognized exchange and clears through a regulated clearinghouse. You get standardized contract terms, public pricing, and formal end-of-year tax reporting that fits Section 1256 workflows.

- Currency futures on a major exchange often qualify.

- Retail spot forex with a dealer typically does not qualify.

- Some brokers offer both products, you need to know which account and which instrument you used.

If you trade FX products on a U.S. exchange, confirm the contract type in your platform and in your broker’s tax documents. If you trade OTC spot, you should assume Section 988 unless you have clear support for a different treatment. If you are unsure which market you are trading in, start with Is Forex Trading Legal in the US? Rules, Regulators and What Traders Must Know.

Section 988 vs 1256: side-by-side comparison for real-world scenarios

Rate impact: when ordinary treatment can cost more (and when it won’t)

Section 988 taxes your net FX gain as ordinary income. That means your gain stacks on top of your other income and faces your marginal bracket.

Section 1256 uses a fixed split. 60 percent gets long-term capital rates, 40 percent gets short-term rates. It does not matter how long you held the position.

In plain terms, Section 1256 often lowers the federal rate on profitable years, especially if you sit in higher brackets. Section 988 can be close to the same cost if your marginal bracket is low and your gains are small.

Loss impact: when ordinary losses are more valuable than capital losses

Section 988 losses are ordinary. You can generally use them without the capital loss limits that apply to most investor capital losses.

Section 1256 losses are capital losses, reported as 60/40. You can use them against capital gains. If you have more losses than gains, your annual deduction against ordinary income is limited, with the rest carried forward.

If you expect a losing year or you want maximum flexibility to offset wages and business income, Section 988 can matter more than rate savings.

Timing impact: realized P&L vs year-end mark-to-market outcomes

Section 988 for spot FX usually follows realized P&L. Your taxable gain or loss triggers when you close the trade, plus any recognized items your broker reports.

Section 1256 has mark-to-market. You treat open positions as if you sold them at fair market value on December 31. You pay tax on paper gains and you deduct paper losses, then you reset your cost basis for the next year.

- If you carry large open winners into year-end, Section 1256 can accelerate tax.

- If you carry large open losers into year-end, Section 1256 can accelerate deductions.

- If you close most trades before year-end, timing differences shrink.

Audit and documentation risk: what the IRS expects to see

Your biggest risk comes from mixing rules across products or switching treatment without support.

- Product proof. Keep broker statements that show the instrument type. Examples include regulated futures contracts, listed options, or OTC spot.

- Year-end support. Save 1099s, year-end statements, and your trade logs. Your totals must tie out.

- Consistency. Apply the same treatment to the same product type each year unless a valid change occurs.

- Elections. If you elect out of Section 988 for eligible contracts, keep a dated record of the election and apply it consistently.

If you cannot clearly show that your trades qualify for Section 1256, treat them as Section 988 until you can. If you are still unsure what market you trade in, use this guide to US forex trading rules and regulators to confirm where your product sits.

Section 988 vs 1256: side-by-side for real-world scenarios

| Scenario | Section 988 outcome | Section 1256 outcome | What this means for you |

|---|---|---|---|

| High-income year, net profitable, frequent trading | Gains taxed at your marginal ordinary rate | 60% long-term, 40% short-term blend | Section 1256 often lowers the effective federal rate on gains |

| Losing year, you want the loss to offset wages or business income | Ordinary loss treatment tends to be more usable | Capital loss treatment, may face annual limits if you lack capital gains | Section 988 can deliver faster tax value from losses |

| You hold large positions open into December | Tax depends mostly on what you closed | Open positions get marked to market at year-end | Section 1256 can create tax on unrealized gains, or deductions on unrealized losses |

| You close most trades quickly and end the year mostly flat | Tax tracks realized closes | Mark-to-market has little effect if few positions remain open | Focus shifts to rate and loss rules, not timing |

| You trade OTC spot through a retail broker | Default treatment in most cases | Usually not available | Assume Section 988 unless you have clear documentation for different treatment |

| You trade currency futures on a US exchange | Usually not the default for these contracts | Common treatment for regulated futures contracts | Expect 1256 reporting and mark-to-market, confirm on your tax forms |

Quick decision framework based on product type, holding period, and consistency

- Start with product type. OTC spot FX usually points to Section 988. Exchange-traded currency futures usually point to Section 1256.

- Then check your profit and loss profile. If you expect a strong net gain and you qualify for 1256, the 60/40 blend can help. If you expect large losses, 988 ordinary losses can help more.

- Then check your year-end exposure. If you hold big open positions into December, 1256 timing can move tax into the current year.

- Stay consistent. Use the same treatment for the same contract type. Save statements, trade logs, and any election records.

How to elect out of Section 988 (and when you should not)

Who can elect out of Section 988, and which instruments usually qualify

You can only elect out for certain “Section 988 transactions” that also qualify for capital treatment. Most retail spot forex does not fit well here because it is not a regulated futures contract and it often does not meet the “forward contract” or “nonequity option” buckets in the way the tax rules expect.

The election most commonly shows up in these areas:

- Foreign currency options that are capital assets in your hands, often exchange traded options.

- Foreign currency forwards used for trading or hedging, when structured as contracts that can qualify for capital gain or loss.

- Nonfunctional currency positions held as a capital asset, in limited cases where your facts support capital treatment.

If you trade exchange traded currency futures that fall under Section 1256, you usually do not need a Section 988 election to get 1256 treatment. The contract type drives the result.

Deadlines and mechanics, what to do before trading starts

You must make the election on a timely basis. In practice, that means you document the election before you enter the trade that you want treated as capital gain or loss instead of ordinary income or loss under Section 988.

Use a written, signed election statement. Keep it with your records. Do not wait until you prepare your return.

- Do it before the first trade in the account or strategy you want covered.

- Be specific about the instrument type, the account, and the effective date.

- Apply it consistently to the covered class of transactions for the period you specify.

Many traders create the election as a dated PDF, sign it, and store it with year files. Some attach a copy to the return as a belt and suspenders step, but your strongest position is having it dated and executed before trading.

What records you should keep

You need records that prove timing, scope, and results.

- Election statement, signed and dated, with the account number and instrument type covered.

- Trade logs showing ticket time, product, size, and price. Export them from your broker and keep the raw file.

- Monthly and annual account statements that tie trades to P and L and show open positions at year end.

- Support for classification, contract specs for the product, exchange listing details for options, and any broker product description.

If you ever face an IRS exam, you win on paper. You need a clean timeline that shows you elected before you traded.

Consistency rules, how to avoid cherry-picking

You cannot pick ordinary treatment for losses and capital treatment for gains after the year ends. That is the fastest way to invite a reclassification.

Set a rule and follow it.

- Same product, same treatment across the year, unless the rules force a different result.

- Same account process, one election file, one log method, one reporting approach.

- No retroactive elections based on how the year turned out.

If you want flexibility, separate strategies by account and document the purpose of each account. Keep the reporting consistent within each.

Common election mistakes that break your position, and safer alternatives

- Making the election after trading starts. Safer alternative, stop trading, document the election, then begin new covered trades going forward.

- Using vague language. Safer alternative, list the exact product type, account, and start date, and keep contract specs.

- Assuming spot forex automatically qualifies. Safer alternative, treat retail spot as Section 988 unless you have a clear fact pattern that supports a qualifying contract type.

- Mixing 988 and 1256 on the same contracts. Safer alternative, classify by instrument first, then apply the correct section consistently.

- Relying on broker tax documents alone. Safer alternative, maintain your own trade exports and reconcile them to statements.

If you trade products on US regulated venues, confirm the instrument status first. Start with the regulatory setup and product type, then align your tax treatment. See US forex trading rules and regulators for the product and venue basics.

Trader vs investor: why your “tax status” changes the outcome

Investor vs trader tax treatment in practice

Your trading activity can fall into two buckets. Investor activity or a trading business. The label changes which deductions you can take, how you report expenses, and how losses hit your return.

- Investor: You report gains and losses on Schedule D and Form 8949 when they are capital. You face capital loss limits, $3,000 per year against ordinary income, then carryforward. Many investment expenses that used to help investors became limited after the Tax Cuts and Jobs Act.

- Trader (business): You run trading like a business. You may deduct ordinary and necessary business expenses tied to trading activity. You still report gains and losses under the correct code section, often Section 988 for spot forex and many OTC forex contracts, and Section 1256 for certain regulated futures and options.

This matters because two traders can place similar trades and end up with different after tax results. The difference often comes from expense treatment and, for some products, elections like Section 475.

Trader Tax Status (TTS), core tests you must meet

The IRS does not grant TTS with a single form. You earn it by how you trade. Courts look at facts and circumstances. Focus on three themes.

- Frequency: You place trades often. Think many trades across many weeks and months. A few bursts of activity do not help.

- Regularity: You trade consistently during the year. Long gaps reduce your case.

- Intent: You seek to profit from short term market moves, not long term appreciation or dividends. Short holding periods support this.

Document your pattern. Keep calendars, trade logs, and broker exports. If your activity looks like investing, the IRS will treat you like an investor.

Section 475 mark-to-market vs Section 1256 mark-to-market

These rules sound similar. They work differently.

- Section 1256 mark-to-market: It applies by default to Section 1256 contracts. You mark positions to market at year end. You get the 60 percent long term and 40 percent short term capital split, regardless of holding period.

- Section 475 mark-to-market: It is an election for qualifying traders with TTS. You treat positions as sold at fair market value at year end, and you generally get ordinary treatment on the resulting gain or loss. Ordinary losses avoid the $3,000 capital loss cap, but you give up capital gain treatment on those positions.

Do not confuse them. Section 1256 is instrument based. Section 475 is status and election based. If you trade forex products across venues, confirm the instrument and venue first. See US forex trading rules and regulators for the framework.

Business expense categories for active traders and what the IRS expects

If you qualify as a trader, you still need clean substantiation. Treat your records like you expect an audit.

- Home office: A dedicated space used regularly and exclusively for trading. Keep square footage math, photos, and utility records.

- Market data and tools: Data feeds, charting platforms, news services, backtesting tools, journaling software, and VPS costs.

- Education: Training that maintains or improves your trading skills. Keep invoices, course outlines, and proof of payment. Avoid claiming costs that look like a new career start.

- Professional fees: Tax prep, CPA, enrolled agent, legal help for elections, and entity setup if relevant.

- Office and technology: Computer equipment, monitors, peripherals, internet, phone, and office supplies. Track business use percentage for mixed use items.

- Travel and meals: Only when primarily business related. Keep receipts and a written business purpose.

Keep receipts, invoices, and payment proof. Keep a written note for the business purpose when it is not obvious. Reconcile expense totals to bank and card statements.

When a tax professional is essential, and what to ask

Get professional help when you plan to claim TTS, make a Section 475 election, trade multiple forex product types, or run high volume. Small mistakes can create large amendments and penalties.

- Ask how they evaluate TTS: What trade frequency and holding period patterns do they look for, and what documents do they want from you.

- Ask about Section 988 vs 1256 mapping: How they classify your exact instruments by venue and contract type, and how they handle mixed products in one account.

- Ask about Section 475 timing and mechanics: Election deadlines, required statements, how they handle the first year adjustment, and what positions they include or exclude.

- Ask about expense positions: Which categories they will support, what substantiation they require, and how they treat home office and mixed use tech.

- Ask about audit readiness: What records they want you to keep, and how long they want them retained.

Pick someone who works with active traders. You need clear positions, not vague comfort.

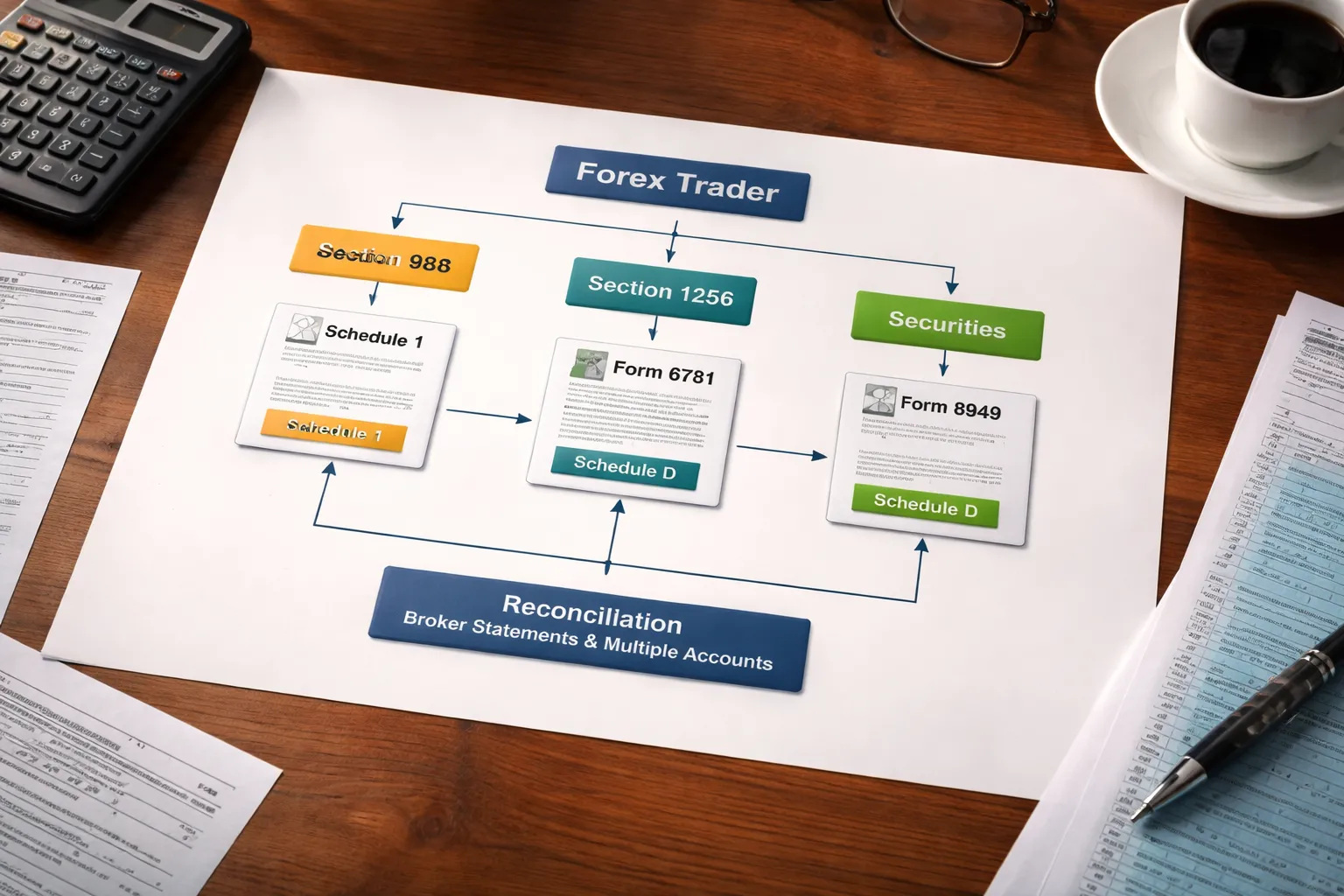

Reporting forex on U.S. tax forms (practical filing map)

Typical forms by treatment

Your filing path depends on what you traded and which tax treatment applies.

- Section 988, spot forex and many retail FX contracts, you usually report as ordinary income or loss. Many filers place the net result on Form 1040, Schedule 1, as “Other income” or “Other loss,” with a statement attached that shows your calculation and identifies it as Section 988 forex.

- Section 1256 contracts, you report on Form 6781. This covers regulated futures contracts and certain exchange traded currency contracts. The Form 6781 total flows to Schedule D.

- Form 8949 and Schedule D, you use these for capital assets. Many traders use them for stocks and options. Some forex positions can land here only if they qualify and you made a valid election out of Section 988 where allowed, and you treat them as capital.

Practical map. If your broker issues a consolidated 1099 that includes 1256 totals, start with Form 6781. If you traded retail spot FX with no 1099 and no 1256 box, expect a self-prepared Section 988 statement and a Schedule 1 style entry.

Where Section 988 items can land

- Ordinary P and L, common for retail spot forex. Many taxpayers report a single net number for the year and attach a statement with support.

- Interest and carry, your broker may label it as swap, rollover, financing, or interest. If you net it into trade P and L in your books, stay consistent and document the method. If you break it out, map it to interest income or expense based on how the broker reports it.

- Fees and commissions, treat them consistently. Many traders include them in trade level P and L. Some deduct them as expenses if they qualify as trading business expenses, which often depends on your facts and whether you file as a trader in securities or as a business entity.

How to reconcile broker 1099s, or the lack of them, with your books

Retail forex often comes with no 1099. That does not reduce your reporting duty. You need a clean tie-out from broker statements to your tax numbers.

- Start with broker yearly summary, if available. Pull realized P and L, financing, commissions, and any adjustments.

- Build your own annual P and L, from daily statements or trade confirmations. Use the same time zone and cutoff the broker uses for statement days.

- Reconcile line by line. Differences usually come from deposits and withdrawals treated as activity, currency translation, open positions carried into year end, and financing booked on a different day than you expect.

- Document your methodology. Note whether you use trade date or settlement conventions, and how you treat partial closes and rollovers.

If you do receive a consolidated 1099, do not assume it covers everything. Many forex products sit outside typical 1099 reporting. Your books still drive the final answer.

Handling multiple accounts, brokers, and product types in one year

Do not mix unlike buckets.

- Separate by tax regime. Keep Section 1256 on its own track for Form 6781. Keep Section 988 spot FX on its own track for ordinary reporting. Keep stocks and equity options on their own track for 8949 and Schedule D.

- Aggregate within each bucket. Combine all Section 1256 accounts into one Form 6781 presentation. Combine all Section 988 spot FX accounts into one annual net result, with a supporting statement that shows each account subtotal.

- Keep product labels consistent. Many brokers call products “forex” even when the tax form category differs. Identify each instrument type using contract specs, venue, and broker disclosures, not marketing names.

- Track transfers between brokers. Transfers can break cost basis trails and create phantom gains if you import history incorrectly. Keep deposit and withdrawal logs for each account.

Wash sales, why they usually apply to securities, and where traders still get tripped up

Wash sale rules generally target securities, like stocks and many equity options. Spot forex and many Section 988 currency contracts typically do not fit the standard “stock or securities” pattern. Traders still get burned in a few ways.

- Mixing stocks with FX. You can have wash sales in your stock and ETF trading even if your forex trading does not trigger them. Keep separate reports and do not let a platform net everything together.

- Trading currency ETFs or FX related securities. If you trade securities that track currencies, wash sale rules can apply like any other security.

- Relying on broker wash sale numbers. Brokers compute wash sales per account. They often do not net across brokers. You must reconcile if you trade the same security in multiple places.

Recordkeeping checklist

You need records that let you rebuild your tax numbers from raw broker data.

- Trade confirmations, fills, size, price, timestamps, and instrument identifiers.

- Daily statements, realized and unrealized P and L, financing, commissions, and balance changes.

- Year end statements, open positions at year end, and any broker adjustments.

- Deposit and withdrawal ledger, dates, amounts, and accounts. Keep bank or wallet records that match.

- P and L methodology memo, how you calculate gains and losses, how you treat financing, how you handle partial closes, and how you translate any non USD figures to USD.

- Product classification list, which instruments you treat as Section 988, which you treat as Section 1256, and which you treat as securities for 8949 and wash sales.

- Tax folder for elections and statements, any Section 988 related elections or disclosure statements you attach, plus copies of what you filed.

Keep your tax treatment consistent with your broker data and your own books. If you change methods midstream, write down why and show the bridge from old to new.

Edge cases and overlooked issues competitors often miss

Spot FX with a U.S. broker vs offshore broker, what changes and what does not

Your broker’s location does not change the Internal Revenue Code. Your product does.

- What does not change: Spot forex gains and losses generally fall under Section 988 as ordinary income or loss. Your default treatment does not flip just because the broker sits offshore.

- What changes: Your reporting workload can change. Offshore brokers often give you weak U.S. tax reporting. You may need to rebuild trade history, P and L, and year-end balances from raw statements.

- What changes: You may trigger foreign account reporting. A foreign broker account can create FBAR and FATCA filings even if your trading tax treatment stays the same.

- What changes: With some offshore brokers you may trade CFDs or other instruments that do not map cleanly to U.S. forms. Do not assume “forex” on the platform equals “forex” for U.S. tax.

Match your tax position to the contract type shown on statements, confirmations, and the broker’s product disclosure. Save those documents in your tax folder.

Crypto-FX pairs and synthetic USD exposure, where taxpayers misclassify transactions

Traders misclassify these trades because the ticker looks like a currency pair. The IRS often sees crypto as property, not currency.

- Crypto pairs: BTC/USD and ETH/USD usually mean you bought or sold crypto property. That points to capital gain or loss, not Section 988.

- Stablecoins: USDT and USDC still count as crypto in most tax workflows. Each swap can create a taxable disposal even if you think you stayed “in dollars.”

- Synthetic forex: Some platforms offer “forex” exposure through crypto collateral, perpetuals, or tokenized products. Your tax result depends on the actual instrument. You may have capital treatment, ordinary treatment, or a mix.

- Common error: Netting everything into one “forex P and L” bucket. That can understate taxable events for crypto disposals and overstate ordinary losses.

Fix this by separating trades into buckets by instrument. Spot FX. Section 1256 contracts. Crypto spot. Crypto derivatives. Reconcile each bucket to statements and wallets.

Hedging and business-related FX, how tax treatment can change for bona fide hedges

Hedging can override your usual trader logic. The IRS cares about why you entered the trade and what it hedged.

- Bona fide hedge: You hedge a real business exposure, like receivables, payables, inventory purchases, or a foreign currency debt.

- Documentation drives treatment: You need contemporaneous records that identify the hedged item and the hedge, plus how you measure effectiveness.

- Timing can change: Hedge accounting can change when you recognize gains and losses. It may also change the character to better match the underlying business item.

- Trader hedge is different: A “hedge” between two speculative positions usually does not qualify as a tax hedge. Do not label trades as hedges unless you can support the business purpose and identification rules.

If you run a business with real foreign currency exposure, treat hedging as its own lane. Keep a hedge memo, invoices, contracts, and a clear link from exposure to trade.

Foreign accounts and informational reporting (FBAR, FATCA/Form 8938) basics

These filings sit next to your tax return. They can apply even when you owe no tax.

- FBAR (FinCEN 114): File if your foreign financial accounts exceed $10,000 in aggregate at any point during the year. This includes many offshore broker accounts.

- Form 8938 (FATCA): Separate filing with your tax return if you exceed thresholds based on filing status and residency. It can apply even when FBAR does not, and vice versa.

- Key number: Use maximum values, not year-end values. Save screenshots or statements that support the highest balance.

- Do not guess: If you used an offshore broker, review whether the account qualifies as foreign and whether it is reportable. Keep account opening docs and monthly statements.

If you need a quick refresher on the regulatory side of where you can trade and with whom, read Is forex trading legal in the United States.

State tax considerations, why your state may not mirror federal benefits

Federal rules set the baseline. States can ignore parts of it.

- No Section 1256 rate benefit in some states: The 60/40 split helps on federal tax. Many states tax all income at the same rate, so your state bill may not drop.

- State conformity changes over time: Some states decouple from federal provisions or lag federal updates. Your result can change by year.

- Net operating loss limits: Ordinary losses under Section 988 can help federally, but your state may cap or modify NOL usage.

- Local taxes: City and local rules can stack on top. Do not plan your strategy using federal rates alone.

Run a federal and state side-by-side projection before you rely on Section 1256 benefits or large ordinary losses. Keep the projection in your tax folder with your election records.

Worked examples: calculating taxes under 988 vs 1256

Example A: profitable year, ordinary income vs 60/40 treatment

Assumptions

- You trade full time. You qualify for trader tax status.

- You have no other income or deductions in this example.

- Your federal ordinary rate is 35%.

- Your federal long term capital gain rate is 15%.

- Your state taxes ordinary income at 6% and taxes capital gains at the same 6%.

- You realize $100,000 of net trading profit.

Section 988 (ordinary)

- Federal tax: $100,000 x 35% = $35,000.

- State tax: $100,000 x 6% = $6,000.

- Total tax: $41,000.

- Effective tax rate: 41.0%.

Section 1256 (60/40)

- 60% long term: $100,000 x 60% = $60,000.

- 40% short term: $100,000 x 40% = $40,000.

- Federal tax on long term portion: $60,000 x 15% = $9,000.

- Federal tax on short term portion: $40,000 x 35% = $14,000.

- Federal subtotal: $23,000.

- State tax: $100,000 x 6% = $6,000.

- Total tax: $29,000.

- Effective tax rate: 29.0%.

Takeaway

- On the same $100,000 profit, Section 1256 saves $12,000 in this setup.

- Your state can shrink the gap if it taxes capital gains at the same rate as ordinary income.

Example B: losing year, ordinary loss value vs capital loss limits

Assumptions

- Your other income is W-2 wages of $120,000.

- Your federal ordinary rate is 32%.

- Your state ordinary rate is 6%.

- You have a net trading loss of $50,000.

- Under the capital loss rules, you only use $3,000 against ordinary income this year. The rest carries forward.

Section 988 (ordinary loss)

- Loss offsets wages: $50,000 reduces taxable ordinary income.

- Federal tax reduction: $50,000 x 32% = $16,000.

- State tax reduction: $50,000 x 6% = $3,000.

- Total current year tax reduction: $19,000.

Section 1256 (capital loss in this simplified example)

- Current year offset against wages: $3,000.

- Federal tax reduction: $3,000 x 32% = $960.

- State tax reduction: $3,000 x 6% = $180.

- Total current year tax reduction: $1,140.

- Capital loss carryforward: $47,000.

Takeaway

- Ordinary loss treatment can matter more in a down year than 60/40 matters in an up year.

- If your state limits NOL usage or uses different carry rules, your real benefit can drop.

Example C: mixed products, spot trades plus 1256 contracts in the same tax year

Assumptions

- You trade spot forex with a net gain of $40,000 treated under Section 988.

- You trade regulated FX futures with a net gain of $60,000 treated under Section 1256.

- Your federal ordinary rate is 35%.

- Your federal long term capital gain rate is 15%.

- Your state rate is 6% on both.

Compute each bucket separately

| Bucket | Income | Federal tax | State tax | Total tax |

|---|---|---|---|---|

| 988 spot (ordinary) | $40,000 | $40,000 x 35% = $14,000 | $40,000 x 6% = $2,400 | $16,400 |

| 1256 futures (60/40) | $60,000 | (60% x $60,000 x 15%) + (40% x $60,000 x 35%) = $13,800 | $60,000 x 6% = $3,600 | $17,400 |

| Total | $100,000 | $27,800 | $6,000 | $33,800 |

Takeaway

- You can have ordinary and 60/40 gains in the same year. You report them in different places.

- Do not net your 988 and 1256 results as if they share the same tax character. The character drives the rate and the loss rules.

Example D: year-end open positions, how mark-to-market changes reported income

Assumptions

- You trade a Section 1256 contract.

- On December 31, you still hold one open contract.

- Your realized profit from closed contracts is $10,000.

- Your open contract shows an unrealized gain of $20,000 at year end.

- Your federal ordinary rate is 35% and your long term rate is 15%.

- Your state rate is 6%.

What happens under Section 1256

- You treat the open position as sold at fair market value on December 31.

- Your taxable gain for the year includes the unrealized $20,000.

- Total Section 1256 gain reported this year: $10,000 + $20,000 = $30,000.

Tax math under 60/40

- 60% long term: $30,000 x 60% = $18,000.

- 40% short term: $30,000 x 40% = $12,000.

- Federal tax: ($18,000 x 15%) + ($12,000 x 35%) = $6,900.

- State tax: $30,000 x 6% = $1,800.

- Total tax: $8,700.

Next year reset

- Your cost basis resets to the December 31 mark.

- If that open gain reverses in January, you report a loss next year.

- This timing can create a cash problem if you owe tax on year-end gains without closing the position.

Practical control

- Track open 1256 positions into December. Do not let the mark surprise you.

- Keep clean broker statements. If your broker looks questionable, review US forex rules and regulators before you fund more accounts.

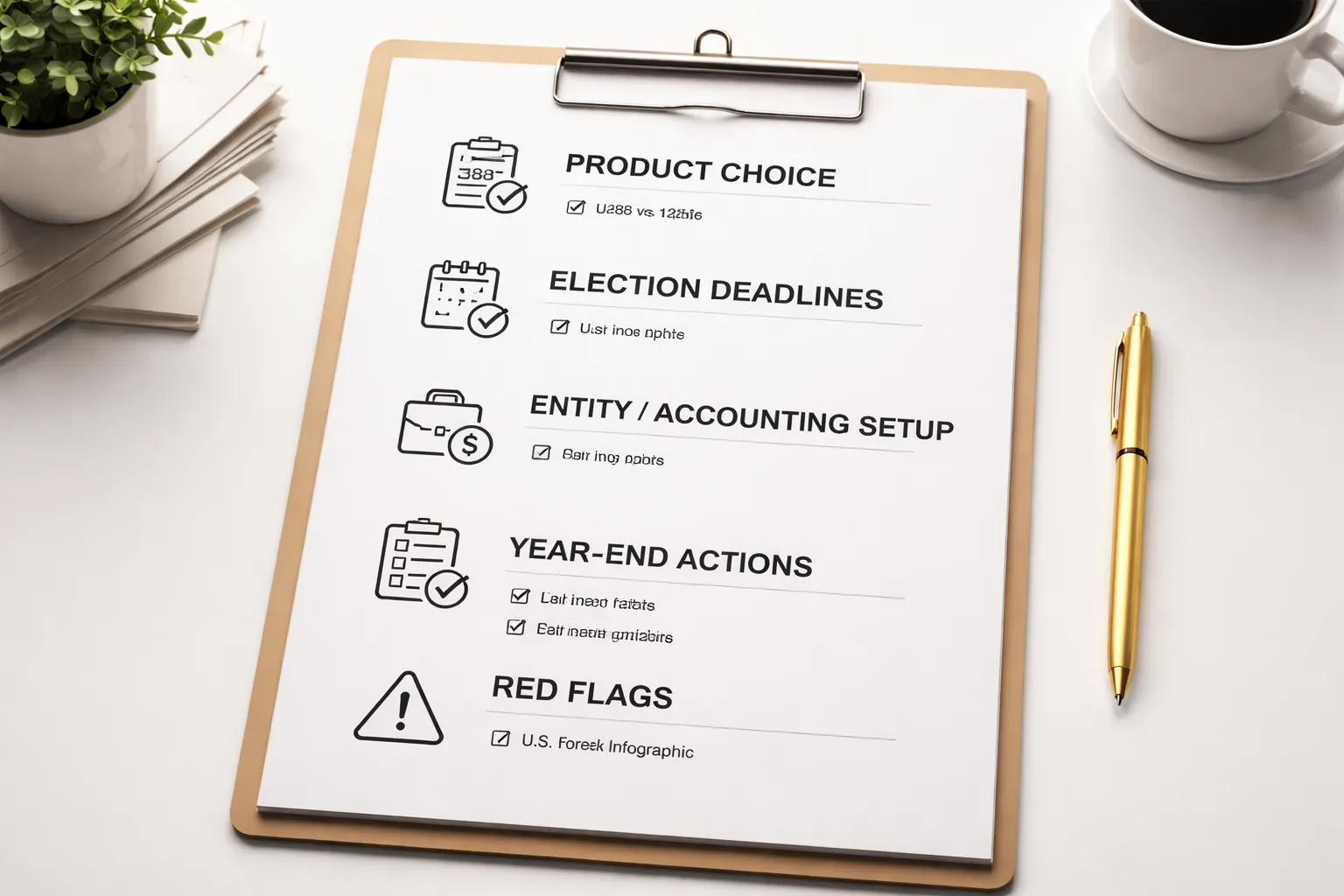

Tax planning checklist for forex traders (before year-end)

Choosing products intentionally

Your tax result starts with what you trade. Decide first, then place trades.

- Spot and most retail OTC forex. Defaults to Section 988. Gains and losses are ordinary.

- Exchange traded FX futures and many broad based currency futures options. Usually Section 1256. Gains and losses follow 60 percent long term, 40 percent short term, marked to market at year end.

- Currency ETFs and FX related stocks. Usually capital gain rules, not 988 or 1256.

- Do not mix assumptions. The same symbol can get different treatment based on where and how you trade it. Match each instrument to the tax character you want before you size up.

| Goal | What usually fits | What to watch |

|---|---|---|

| Prefer ordinary loss treatment to offset ordinary income | Section 988 spot style forex | Limited capital loss planning, no 60/40 blend |

| Prefer blended 60/40 capital treatment | Section 1256 FX futures | Year end mark to market, timing can create cash strain |

| Prefer pure capital gains framework | FX ETFs, stocks | Wash sale and basis tracking rules can apply |

Election readiness

Elections fail for one reason. You miss the deadline or you cannot prove you made it.

- Build a calendar. Put reminders for election deadlines, entity return due dates, and extension deadlines. Do this when you open the account, not in December.

- Keep an election packet. One folder per tax year. Include dated election statements, copies of filed returns, and proof of timely filing.

- Document trade classification. Keep a one page policy that states what you treat as 988 and what you treat as 1256, and why. Tie it to account types and instruments.

- Use a repeatable workflow. Monthly download of broker statements, monthly reconciliation, and a quarterly check that your records match your tax positions.

Entity and accounting considerations

An entity does not fix bad records. It can improve organization, but it adds rules.

- Individual. Simple filing. Fewer moving parts. You still need clean books and support for every number.

- Single member LLC. Often the same federal tax treatment as an individual, but better separation for banking and bookkeeping.

- S Corp election. Consider only when you have stable net income and a real reason to run payroll and corporate compliance. Do not use it as a default move.

- Pick an accounting method and stay consistent. Track proceeds, fees, and interest the same way all year. Do not change classifications in December.

- Lock down data sources. Use broker CSV exports, monthly statements, and a single journal for adjustments. Do not rely on screenshots.

Year-end actions

Year end planning is control. You reduce surprise marks, bad timing, and missing data.

- Run a tax P and L by product. Separate 988, 1256, and capital assets. Do not blend them.

- Harvest with purpose. If you need losses this year, close positions before year end. If you need to defer gains, do not realize them in December unless the trade plan supports it.

- Manage open 1256 positions. Estimate the mark to market impact in early December. Plan cash for the tax bill if the mark creates reportable gains.

- Confirm year-end reports. Check that your broker tax package matches your own records. Fix symbol mapping errors and contract multipliers before you file.

- Reconcile deposits and withdrawals. Match every transfer to a bank record. Clean this up before January statements arrive.

- Record expenses with proof. Keep invoices, subscription receipts, and a business purpose note. Do not wait until tax time.

- Validate performance analytics. If you use third party tracking, confirm it matches broker statements. Readouts can differ because of open trades and swap. Use how to read Myfxbook results to understand what the metrics do and do not show.

Red flags to avoid

- Inconsistent reporting across years. Switching between 988 and 1256 logic without documentation invites questions.

- Missing or late elections. If you cannot show timely filing, assume the election fails.

- Unsupported expense claims. No receipt, no clear business purpose, no deduction. Trading education and travel often get abused, treat them with caution.

- Broker statement gaps. Missing months, missing confirmations, or mismatched balances. Fix it now. Do not file with holes.

- Mixing personal and trading cash. Commingling breaks your audit trail and creates basis and expense problems.

- Ignoring regulator and product mismatch. If you trade offshore or through a questionable dealer, your data quality and compliance risk rise fast.

FAQ

Do I pay taxes on every forex trade, even if I do not withdraw?

Yes. You owe tax on realized gains and losses for the year, not on withdrawals. Closing a trade usually creates a taxable event. Open trades at year-end stay unrealized unless your broker applies mark-to-market rules to that product.

What is the default tax treatment for spot forex?

Most retail spot forex falls under Section 988. Gains and losses are ordinary. You report them on Form 1040, usually through Form 8949 and Schedule 1 or as instructed by your tax pro based on your activity and elections.

What is the default tax treatment for forex futures?

Exchange-traded currency futures are typically Section 1256 contracts. They get 60 percent long-term and 40 percent short-term capital treatment. They also get year-end mark-to-market. You usually report them on Form 6781.

Can I choose Section 1256 treatment for spot forex?

Usually no. Section 1256 applies to specific contract types, mainly regulated futures and certain options. Spot forex generally stays Section 988 unless you trade products that qualify as Section 1256 under the tax rules.

Can I elect out of Section 988 for forex options?

In some cases, yes. Certain nonequity options can qualify for an election out of Section 988 into capital treatment. You must make the election properly and on time. Get written confirmation of the election process from your tax advisor.

Which is better, Section 988 or Section 1256?

It depends on your results. Section 988 ordinary losses can offset ordinary income without the capital loss limits. Section 1256 can lower tax on gains via 60 40 rates. Your product type often decides the rule more than preference.

Do I need trader tax status to use Section 1256?

No. Section 1256 treatment depends on the contract, not trader tax status. Trader tax status affects business expense treatment and possible mark-to-market under Section 475 for securities, not whether a contract is a Section 1256 contract.

How do I handle losses under Section 988?

You treat them as ordinary losses. They can offset wages, interest, and other ordinary income, subject to general limits like at-risk and hobby loss rules. Keep clean trade logs and broker statements to support each realized loss.

How do I handle losses under Section 1256?

You treat them as capital losses with a blended 60 40 character. Net losses may qualify for a Section 1256 loss carryback using Form 1045 or amended returns, if you meet the rules. Document contract type and year-end mark-to-market.

What records do I need for a clean forex tax file?

Keep monthly statements, trade confirmations, year-end summaries, deposits and withdrawals, and your platform export. Match balances month to month. Save your 1099 if issued. Do not rely on screenshots. Store files in a single folder by tax year.

My broker did not send a 1099. Can I still file?

Yes. Many forex accounts do not issue a 1099. You still must report income. Use your statement summaries and raw trade exports to compute realized P and L. If you cannot reconcile totals, fix the data before you file.

Does trading offshore change my US tax rules?

No. US citizens and residents pay US tax on worldwide income. Offshore trading often creates weaker reporting and bigger audit risk. You may also trigger extra filings for foreign accounts. Review compliance and legality before you fund an offshore broker.

How do I reduce scam and compliance risk before tax season?

Vet your broker and dealer first. Confirm regulation, product type, and reporting quality. Avoid platforms that cannot produce complete statements and confirmations. Use this checklist to screen risks: Is forex trading legal in the United States?

Conclusion

Conclusion

Your forex tax result in the US depends on one choice, Section 988 or Section 1256. It controls the character of your gains and losses, the rate you pay, and how you can use losses.

- Section 988 fits most spot forex. It produces ordinary gains and losses. Ordinary losses can offset ordinary income. It can help when you have a net loss year.

- Section 1256 applies to regulated futures and certain options. It uses the 60/40 split and mark to market at year end. It can lower the effective rate in profitable years. Loss rules differ from ordinary treatment.

Do this before year end. Identify your product type for every account. Confirm whether it qualifies for 988 or 1256. Make any election on time. Save proof. Keep monthly statements, daily trade logs, confirmations, deposits, withdrawals, and year end reports.

Final tip. Reduce tax season risk by reducing broker risk. Trade only with platforms that give complete, consistent records and clear US compliance. Use this forex broker safety checklist before you fund an account.

-

-

- Section 1256 explained (60/40 blended capital gains treatment)

- Which contracts typically qualify

- The 60/40 rule (blended capital gains treatment)

- Mark-to-market at year-end (timing changes)

- Netting rules and how 1256 losses interact with other capital gains and losses

- What “regulated” and “exchange-traded” mean for retail traders

-

- Rate impact: when ordinary treatment can cost more (and when it won’t)

- Loss impact: when ordinary losses are more valuable than capital losses

- Timing impact: realized P&L vs year-end mark-to-market outcomes

- Audit and documentation risk: what the IRS expects to see

- Section 988 vs 1256: side-by-side for real-world scenarios

- Quick decision framework based on product type, holding period, and consistency

-

- Typical forms by treatment

- Where Section 988 items can land

- How to reconcile broker 1099s, or the lack of them, with your books

- Handling multiple accounts, brokers, and product types in one year

- Wash sales, why they usually apply to securities, and where traders still get tripped up

- Recordkeeping checklist

-

- Spot FX with a U.S. broker vs offshore broker, what changes and what does not

- Crypto-FX pairs and synthetic USD exposure, where taxpayers misclassify transactions

- Hedging and business-related FX, how tax treatment can change for bona fide hedges

- Foreign accounts and informational reporting (FBAR, FATCA/Form 8938) basics

- State tax considerations, why your state may not mirror federal benefits

-

- Do I pay taxes on every forex trade, even if I do not withdraw?

- What is the default tax treatment for spot forex?

- What is the default tax treatment for forex futures?

- Can I choose Section 1256 treatment for spot forex?

- Can I elect out of Section 988 for forex options?

- Which is better, Section 988 or Section 1256?

- Do I need trader tax status to use Section 1256?

- How do I handle losses under Section 988?

- How do I handle losses under Section 1256?

- What records do I need for a clean forex tax file?

- My broker did not send a 1099. Can I still file?

- Does trading offshore change my US tax rules?

- How do I reduce scam and compliance risk before tax season?

-

-

- Section 1256 explained (60/40 blended capital gains treatment)

- Which contracts typically qualify

- The 60/40 rule (blended capital gains treatment)

- Mark-to-market at year-end (timing changes)

- Netting rules and how 1256 losses interact with other capital gains and losses

- What “regulated” and “exchange-traded” mean for retail traders

-

- Rate impact: when ordinary treatment can cost more (and when it won’t)

- Loss impact: when ordinary losses are more valuable than capital losses

- Timing impact: realized P&L vs year-end mark-to-market outcomes

- Audit and documentation risk: what the IRS expects to see

- Section 988 vs 1256: side-by-side for real-world scenarios

- Quick decision framework based on product type, holding period, and consistency

-

- Typical forms by treatment

- Where Section 988 items can land

- How to reconcile broker 1099s, or the lack of them, with your books

- Handling multiple accounts, brokers, and product types in one year

- Wash sales, why they usually apply to securities, and where traders still get tripped up

- Recordkeeping checklist

-

- Spot FX with a U.S. broker vs offshore broker, what changes and what does not

- Crypto-FX pairs and synthetic USD exposure, where taxpayers misclassify transactions

- Hedging and business-related FX, how tax treatment can change for bona fide hedges

- Foreign accounts and informational reporting (FBAR, FATCA/Form 8938) basics

- State tax considerations, why your state may not mirror federal benefits

-

- Do I pay taxes on every forex trade, even if I do not withdraw?

- What is the default tax treatment for spot forex?

- What is the default tax treatment for forex futures?

- Can I choose Section 1256 treatment for spot forex?

- Can I elect out of Section 988 for forex options?

- Which is better, Section 988 or Section 1256?

- Do I need trader tax status to use Section 1256?

- How do I handle losses under Section 988?

- How do I handle losses under Section 1256?

- What records do I need for a clean forex tax file?

- My broker did not send a 1099. Can I still file?

- Does trading offshore change my US tax rules?

- How do I reduce scam and compliance risk before tax season?

-

How to Place a Forex Trade Step by Step (Your First Trade Explained)

2 months ago -

Forex Trading vs Crypto Trading: Which Market Is Better for Beginners?

2 months ago -

Forex Lot Size Calculator: How to Use It to Size Trades Correctly

4 months ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

4 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

4 months ago

-

Is Forex Trading Legal in the United States? Rules, Regulators & What to Know

4 months ago -

Forex Market Hours & Trading Sessions Explained (Best Times to Trade)

4 months ago -

Forex Trading Platforms Comparison: MetaTrader vs cTrader vs TradingView

4 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

4 months ago -

What Is a Lot Size in Forex? Lot Types + Quick Examples

4 months ago