Inflation and Exchange Rates Explained (Why Currencies Rise or Fall)

Inflation and exchange rates move together. When prices rise faster in one country than another, that currency often loses value. When markets expect higher interest rates to fight inflation, that currency can rise. Your job is to know which force dominates.

This guide explains the core links between inflation, interest rates, trade flows, and central bank credibility. You will learn how to read inflation data, spot when rate expectations matter more than the headline, and understand why two countries with similar inflation can still see different currency moves. You will also see the key drivers that hit major pairs first, like EUR/USD, GBP/USD, and USD/JPY.

Use this with your forex economic calendar so you track releases that move prices, not noise.

Key Takeaways

- In het kort: Inflation moves FX through expectations, not the headline.

- In het kort: The key variable is the inflation gap between two countries, not one country in isolation.

- In het kort: Currencies rise when your market prices higher relative rates, tighter policy, or less future easing.

- In het kort: Real yields matter, nominal yields alone can mislead when inflation shifts.

- In het kort: The first reaction often hits major pairs and rate differentials, then spreads to crosses.

- In het kort: Central bank reaction functions drive the move, the same CPI print can mean different policy paths.

- In het kort: Risk sentiment can override inflation for stretches, especially in USD and JPY pairs.

Key takeaways

- Track relative inflation. Build a simple spread, CPI (Country A) minus CPI (Country B). The spread drives rate expectations and FX.

- Separate headline from core. Headline often fades if energy or food drives the surprise. Core and services inflation tend to stick and matter more for policy.

- Watch the path, not one print. Markets price the next 3 to 6 meetings. A small CPI surprise can move FX if it shifts the expected rate path.

- Map CPI to the central bank. Ask one thing, does this print change the probability of hikes, cuts, or a hold. If it does, FX reacts.

- Use real yield logic. If yields rise but inflation expectations rise faster, real yields fall and the currency can weaken.

- Expect different outcomes with similar inflation. Growth, wages, fiscal stance, and credibility change how each central bank responds.

- Focus on what hits majors first. EUR/USD, GBP/USD, and USD/JPY usually react first because liquidity is highest and rate differentials price fast.

- Know the event stack. CPI, PCE, wage data, and central bank meetings often trade as one sequence. The first release sets the tone, later events confirm or reverse.

- Use your calendar with intent. Filter for market moving releases and compare actual vs consensus vs prior. Use a forex economic calendar step-by-step to track surprises and policy expectations.

Inflation and exchange rates: the core concepts (in plain English)

What an exchange rate really measures (price of money vs price of goods)

An exchange rate is a price. It is the price of one currency in another currency.

EUR/USD at 1.09 means 1 euro costs 1.09 US dollars. If it moves to 1.12, the euro got more expensive and the dollar got cheaper, in that pair.

FX prices money, not a shopping basket. A currency can rise in FX while your local prices still rise. These are different prices with different drivers.

Keep two lenses separate.

- Price of money: exchange rate, set by global trading, capital flows, and policy expectations.

- Price of goods: domestic price level, measured by CPI, PCE, producer prices, and wages.

Inflation is a loss of purchasing power, and FX markets care

Inflation means your currency buys fewer goods and services over time. That is purchasing power loss.

FX markets care because inflation changes what central banks do. It changes real returns. It changes where global money wants to sit.

- Higher inflation pushes markets to price tighter policy, higher yields, or both.

- If a central bank stays behind inflation, real yields fall. That can hurt the currency.

- If inflation falls fast, markets may price rate cuts. That can weaken the currency even if inflation looks “good” in headlines.

So you track inflation to track the policy path, not to guess the next grocery bill.

Nominal vs real exchange rates, and why the “real” story matters

The nominal exchange rate is the quoted FX rate you see on charts. EUR/USD, USD/JPY, and so on.

The real exchange rate adjusts that nominal rate for inflation differences between countries. It tells you who gained purchasing power after prices moved.

Use this rule.

- If your currency rises 5% but your inflation runs 5% above the other country, you did not gain real purchasing power.

- If your currency stays flat but your inflation runs lower, you gained in real terms.

FX can move on rates and risk fast. Real value shifts slower. Both matter, but they answer different questions.

| Concept | What it measures | What to watch |

|---|---|---|

| Nominal exchange rate | Currency price vs another currency | Spot rate, forward points, rate expectations |

| Real exchange rate | Nominal rate adjusted for inflation gaps | CPI or PCE differentials, tradables inflation, unit labor costs |

If you want the trading version of this, focus on relative inflation and relative policy, not inflation in one country in isolation. See fundamental analysis in forex for the full framework.

Inflation rate vs price level, and how base effects mislead

Inflation rate is the speed of price changes. Price level is the actual level of prices.

Year over year inflation can fall while prices keep rising. That confuses traders who read headlines too literally.

- If CPI rises from 100 to 110, prices went up 10%.

- If the next year CPI rises from 110 to 113, inflation is 2.7% year over year, but prices still went up.

Base effects drive this. The comparison point, last year’s number, changes the reported rate even if monthly price pressure stays firm or turns.

| Series | What it can hide | What traders check |

|---|---|---|

| YoY inflation | Base effects, old shocks dropping out | Next 1 to 3 prints, turning points |

| MoM inflation | Noise, seasonality | 3 to 6 month annualized trend |

| Core inflation | Still misses some supply shocks | Core services, shelter, wages |

When you read CPI, separate three things. The level, the rate, and the trend. Markets trade the trend because it changes the policy path.

The main mechanisms linking inflation to currency moves

Purchasing Power Parity (PPP), the long-run anchor

PPP links inflation to exchange rates through relative prices. If prices rise faster in your country than abroad, your currency should lose value over time. You need more of it to buy the same basket.

Core intuition: exchange rates adjust so similar goods cost the same across countries after conversion. High inflation makes your goods expensive. The currency must fall to restore price parity.

Simple PPP formula:

Expected FX change (home currency depreciation) ≈ inflation(home) minus inflation(foreign).

Example: your inflation runs 6% and a peer runs 2%. PPP implies about 4% depreciation over the period, all else equal.

What PPP gets right: it explains long horizons. Multi year currency trends often match inflation gaps, especially in high inflation countries.

Why PPP fails in the short run

- Services dominate CPI. Many services do not trade across borders, haircuts, rent, medical care. Their prices can diverge without forcing FX moves.

- Trade barriers and taxes. Tariffs, quotas, VAT, shipping, and compliance costs break the one price link.

- Sticky prices. Firms change prices slowly. FX can move in minutes. Goods prices adjust later.

- Different baskets. CPI weights differ. “Inflation” does not measure the same thing in every country.

- Terms of trade shocks. Energy and food swings can lift CPI while also boosting export revenue for commodity producers. The currency can rise even as inflation rises.

Interest-rate channel, inflation expectations move FX fast

FX trades the policy path. Inflation changes that path through expectations.

- Markets track inflation prints and revise the expected peak rate, the timing of cuts, and the risk of recession.

- If expected inflation rises and the central bank reacts with higher policy rates, short dated yields rise.

- Higher yields can reprice the currency upward, even if inflation is high.

- If inflation rises but the central bank looks behind the curve, real yields fall. The currency often weakens.

What to watch: breakeven inflation, real yields, OIS curves, and the 2 year rate differential versus peers. Those usually lead spot FX.

Use an economic calendar for forex to line up CPI releases with rate decisions and speeches. You trade the delta between the print and expectations.

Capital flows, yields attract money, until risk takes over

Higher yields pull in foreign capital. That demand can lift your currency.

- Carry flows: investors borrow in low yield currencies and buy high yield ones. This supports the high yielder while volatility stays low.

- Portfolio flows: pension funds and asset managers shift toward markets with higher expected real returns.

- Hedging costs: if FX hedging wipes out the yield pickup, flows slow. Covered yield matters, not just the headline rate.

When higher yields do not help:

- Inflation scares. If inflation looks unanchored, investors demand a risk premium and step back.

- Recession risk. Markets may price aggressive hikes now and deep cuts later. The currency can fade as growth breaks.

- Funding stress. In risk off periods, investors unwind carry and buy safe havens. High yield currencies can drop fast.

Trade competitiveness, inflation hits the current account over time

Inflation changes your relative prices. That shifts trade flows with a lag.

- If your costs rise faster than competitors, your exports lose share and imports look cheaper.

- The trade balance can deteriorate. That reduces structural demand for your currency.

- FX may need to weaken to restore competitiveness by lowering foreign currency prices of your exports.

What to track: unit labor costs, export prices, real effective exchange rate, and the current account. These link inflation to slower, trend driven FX moves.

When high inflation strengthens a currency (the counterintuitive cases)

Credible central bank tightening and the “higher-for-longer” FX effect

High inflation can lift your currency when markets expect your central bank to respond hard and stay restrictive.

FX trades the path of policy, not today’s CPI print. If investors price more hikes, fewer cuts, and a longer hold, your currency can rise even while inflation stays high.

- What you track: overnight index swaps (OIS) for the policy path, futures-implied terminal rate, and how far the market pushes the first expected cut.

- Watch the credibility signal: inflation expectations that stop rising even as headline inflation stays elevated.

- Watch the carry channel: widening short rate differentials versus peers, plus steeper cross currency basis demand for funding.

If your central bank surprises hawkish and the market believes it, foreign capital chases yield. That demand can dominate the inflation damage, at least for a while.

Real yields vs nominal yields: the difference that drives investors

Nominal yields can rise with inflation and still fail to support your currency. Investors care about returns after inflation.

Real yield equals nominal yield minus expected inflation. When real yields rise versus other countries, your currency often gains.

- What you track: 5Y and 10Y real yields, breakeven inflation, and the real yield spread versus key counterparts.

- Cleanest read: inflation-linked bonds and breakevens, plus survey measures of medium-term inflation expectations.

- Red flag: nominal yields up, breakevens up more. Real yields fall. Your currency can still weaken.

This is why two countries can print the same inflation rate and see opposite FX moves. The winner is the one with higher real yields and a credible path to lower future inflation.

Inflation caused by strong demand vs inflation caused by supply shocks

Inflation from strong demand can support your currency. Inflation from supply shocks usually does the opposite.

- Demand-driven inflation: strong growth, tight labor markets, rising wages, and firm consumption. Markets expect tighter policy and higher real yields. Your currency can strengthen.

- Supply-driven inflation: energy spikes, import price shocks, or supply disruptions. Growth slows while prices rise. Policy faces a tradeoff. Your currency often weakens.

Separate the two with data.

- What you track: core inflation versus headline, services inflation, wage growth, job openings, PMIs, and retail sales.

- Trade shock check: terms of trade, import price inflation, and energy share in CPI.

- Policy constraint check: recession risk pricing in rates markets and credit spreads.

Demand inflation tends to bring inflows. Supply shock inflation tends to bring outflows.

Safe-haven dynamics: why USD/JPY/CHF can move against textbook logic

In stress, FX can ignore inflation and follow safety and funding flows.

- USD: can rise during risk-off even if US inflation runs hot. Global investors buy Treasuries and hold dollars for liquidity.

- JPY: can strengthen in sharp risk-off moves because investors unwind carry trades and repatriate capital, even when Japan runs low yields.

- CHF: can strengthen on safe-haven demand and institutional inflows, even when inflation differentials point the other way.

Track risk first.

- What you track: VIX, equity drawdowns, credit spreads, and funding stress indicators.

- Positioning check: CFTC futures positioning and signs of crowded carry.

- Rates check: short rate differentials still matter, but risk can swamp them for weeks or months.

If you trade yen pairs, rate spreads and risk sentiment interact. Use this guide on what moves USD/JPY to map the drivers.

When inflation weakens a currency (the classic pattern)

Erosion of purchasing power and long-run depreciation pressure

Higher inflation cuts your currency’s real purchasing power. Over time, FX prices tend to reflect that gap.

Track the inflation differential. Watch CPI, core CPI, and trimmed mean measures versus major peers. A country running 3 to 6 points hotter than its trading partners usually faces steady depreciation pressure unless rates, growth, or capital inflows offset it.

Use real rates, not nominal rates. Calculate policy rate minus expected inflation. If your real rate stays negative while peers move positive, you often see outflows and a weaker currency.

- Data to watch: CPI and core CPI, breakevens, inflation swaps, real yield curves.

- FX tell: the currency struggles to rally on good news, then drops hard on bad prints.

Unanchored expectations, wage-price spirals and credibility loss

Inflation hurts FX most when expectations slip. The market stops trusting the central bank to cap prices.

Watch long-run inflation expectations. If 5y5y inflation swaps rise, or consumer expectations jump and stay high, the market starts pricing a weaker currency path. You also get higher risk premia in bonds, which pushes domestic funding costs up and scares off foreign buyers.

Wages matter. When wage growth runs above productivity and services inflation stays sticky, markets expect inflation to persist. If the central bank hesitates, credibility drops and FX sellers press harder.

- Data to watch: 5y and 5y5y inflation swaps, breakevens, wage growth, unit labor costs, services CPI.

- Policy tell: dovish guidance after hot inflation prints, or repeated “transitory” messaging while core stays high.

Fiscal dominance, high deficits, monetization fears, and FX selloffs

Big deficits can turn inflation into an FX problem fast. Markets focus on how the government funds itself.

If investors think the central bank must protect government financing, they price monetization risk. That shows up as a steeper curve, weaker demand at bond auctions, and rising inflation risk premia. FX often sells off in steps around auctions, budgets, and rating headlines.

Separate two cases. Tight fiscal plus credible tightening can stabilize FX even with high inflation. Loose fiscal plus hesitant policy usually breaks it.

- Data to watch: deficit to GDP, debt to GDP, auction bid to cover, term premium, CDS spreads, rating outlooks.

- Market tell: higher yields and weaker FX at the same time, especially after fiscal announcements.

Current account vulnerability, importing inflation via weaker FX

If your country runs a current account deficit, a weaker currency can feed inflation back into itself. Imports get more expensive. Energy, food, and intermediate goods hit fastest.

This matters more when invoicing sits in dollars and your economy depends on imported fuel. FX depreciation lifts local prices, inflation prints hot, and the central bank faces a bad choice between growth and inflation. If reserves look thin, markets test the currency harder.

- Data to watch: current account balance, trade balance, import share of CPI, FX reserves, external debt maturity profile.

- FX tell: large moves around oil, gas, and shipping shocks, plus widening cross currency basis and higher forward points.

Central banks, credibility, and why communication moves FX

Inflation targeting vs other regimes

Your central bank regime sets the rules FX traders use.

- Inflation targeting. The bank sets a clear inflation goal and moves rates to hit it. FX responds to expected real rates, policy credibility, and how fast inflation returns to target. When inflation runs hot and the bank hesitates, your currency usually weakens.

- Peg. The bank fixes the currency to another currency. Inflation can stay high if the peg forces the wrong interest rate for your economy. FX moves less day to day, then moves a lot when the peg breaks or gets reset. Reserves, capital controls, and external debt determine how long the peg holds.

- Managed float. The bank lets FX move but leans against extremes. You see fewer trends and more two way risk around intervention levels. Watch reserves, forward points, and onshore vs offshore pricing for stress.

- Dollarization. The country uses a foreign currency. You remove FX volatility but you lose monetary policy. Inflation then tracks fiscal policy, wage growth, and import prices. Competitiveness adjusts through jobs and growth, not the exchange rate.

Regime choice changes what matters most. In a peg, reserves and policy constraints dominate. In inflation targeting, the reaction function dominates.

Forward guidance and surprise risk

FX moves on gaps between what you expect and what the bank delivers. Markets price the whole path, not the next meeting.

- What gets priced. The expected policy rate path, the terminal rate, and how long rates stay restrictive. FX also prices balance sheet policy and liquidity tools when they affect funding conditions.

- Where to see expectations. OIS curves, interest rate futures, overnight funding rates, and implied terminal pricing. Add inflation swaps and breakevens to gauge real rate expectations.

- What drives the FX jump. A hike with a dovish statement can weaken the currency. A hold with a hawkish forecast can strengthen it. The statement, projections, and press conference often matter more than the rate line.

- How to measure surprise. Compare the decision to what futures implied the day before. Track the change in the front end of the curve and the 2 year yield. FX usually follows the short end when inflation risk dominates.

If you trade around events, you need the calendar, consensus, and positioning. Use your forex economic calendar to map the meetings, inflation prints, jobs data, and key speeches that shape expectations.

Policy reaction functions and what “data dependence” means for FX

Data dependence sounds vague, but you can model it. You look for which data the bank reacts to, and how quickly it reacts.

- Inflation focus. Some banks react to headline CPI. Others react to core CPI, trimmed mean, or services inflation. If the bank targets core but you trade headline, you misread policy risk.

- Labor market focus. Banks that prioritize jobs respond to wage growth, vacancies, and participation. Strong labor data can strengthen the currency if it raises the expected rate path.

- Growth and credit focus. When the bank worries about recession or financial stability, it may tolerate higher inflation. That usually lowers expected real rates and weakens FX.

- Transmission speed. Floating rate mortgage systems and high pass through economies feel hikes fast. Banks in these systems may stop earlier. That caps the currency unless inflation stays sticky.

Track a simple scorecard. Compare inflation trend, wage trend, and activity trend to the bank’s stated priorities. Then map that to the next three meetings, not just the next one.

| Central bank language | What it often signals | Typical FX impact | Data to watch |

|---|---|---|---|

| “We need more evidence” | Higher bar for cuts or hikes | Less volatility until key data hits | Core CPI trend, wages, inflation expectations |

| “Policy is restrictive” | Peak rate near, time at peak matters | Currency depends on how long rates stay high | Services inflation, unemployment rate, growth surprises |

| “We stand ready to act” | Greater sensitivity to downside or upside risks | Bigger moves on data prints | Financial conditions, credit spreads, FX volatility |

| “Temporary factors” | Bank may look through inflation | Lower expected real rates, weaker FX if inflation persists | Inflation diffusion, rents, wages, import prices |

Independence and political pressure as an exchange-rate variable

FX prices credibility. Credibility comes from independence, consistency, and a record of hitting targets.

- Fiscal dominance risk. When government borrowing rises and the central bank faces pressure to keep yields low, markets price higher future inflation. Your currency can weaken even before inflation prints.

- Leadership and mandate risk. Changes in the governor, public attacks on the bank, or mandate rewrites raise the risk premium in the currency. You often see it in weaker FX, higher bond term premium, and steeper inflation expectations.

- Intervention credibility. Verbal support without reserves or policy backing fails. Markets fade it. Coordinated intervention and tighter policy carry more weight.

- Capital controls and rules. Sudden controls can slow outflows, but they also raise long term risk and reduce foreign capital. That can weaken the currency once the immediate pressure eases.

Watch the hard signals. Primary balance trends, debt maturity, central bank financing of government, reserve coverage, and legal changes to the mandate. When those deteriorate, communication loses power and FX stops listening.

Inflation differentials: comparing countries is the real FX test

How to read CPI and PCE across two countries (apples-to-apples)

FX trades the gap, not the number.

Start with the same inflation concept on both sides. Use CPI versus CPI when you can. If you compare US PCE to another country’s CPI, you mix different baskets and methods.

- Match the frequency. Compare monthly to monthly, or year over year to year over year. Do not mix.

- Use seasonally adjusted series for month over month. Use non-seasonally adjusted for year over year if that is the local standard.

- Normalize the horizon. For FX, 3 month annualized and 6 month annualized often track turning points faster than year over year.

- Control for base effects. A falling year over year print can come from last year’s spike rolling off. Check the month over month path.

- Compare to what was priced. Markets move on surprise. Track consensus and the prior print, then map that to rate expectations.

- Focus on the differential. If Country A disinflates faster than Country B, all else equal the expected policy path diverges. FX reacts to that divergence.

If you trade data, tie each inflation release to the next central bank decision window. Use an economic calendar for Forex to line up CPI, wage data, and policy meetings.

Why core inflation can matter more than headline for FX

Headline inflation moves with energy and food. Core inflation captures persistence. Central banks react to persistence.

- Core drives the policy reaction function. Sticky services inflation usually matters more for the terminal rate and the hold period.

- Watch services ex housing or similar “supercore” cuts. They track labor costs and demand better than goods prices.

- Check trimmed mean and median inflation. These reduce one-off spikes and give you a cleaner trend signal.

- Map core to wages. If wage growth runs above productivity plus target inflation, core tends to stay firm.

When headline drops from oil but core stays hot, markets often fade the headline move. The currency follows rates, not relief at the pump.

Terms of trade and commodity inflation (oil, gas, metals, food)

Inflation does not hit every country the same way. The trade mix decides who imports inflation and who exports it.

- Commodity exporters can get a currency tailwind. Higher export prices lift income, fiscal receipts, and external balances.

- Commodity importers can face a double hit. Higher energy costs widen the trade deficit and raise CPI at the same time.

- Look at energy dependency. Gas-heavy economies react differently than oil-heavy ones. The pass-through to CPI also differs.

- Watch food weight in CPI. In many emerging markets, food has a large CPI share. Droughts and global grain prices can move inflation fast.

- Track the current account. A worsening current account alongside rising inflation is a bad mix for FX, especially if reserves fall.

For practical work, pair the inflation differential with trade data, import prices, and energy balance. That tells you if the inflation shock is demand-led, supply-led, or external.

Productivity and Balassa–Samuelson: structural drivers beyond CPI

Some currencies rise with higher inflation. Structural productivity can explain why.

- High productivity growth can mean higher real wages. That can lift prices in services without killing competitiveness in tradables.

- Balassa–Samuelson effect. Fast productivity gains in tradable sectors push wages up across the economy. Non-tradable prices rise, CPI rises, and the real exchange rate appreciates.

- Separate good inflation from bad inflation. Productivity-led price pressure often comes with stronger growth, stronger fiscal capacity, and better external accounts. Demand overheating or fiscal dominance usually does not.

- Use unit labor costs. If unit labor costs rise because productivity lags wages, competitiveness erodes. That tends to weaken the currency over time.

| Driver | What to check | FX implication |

|---|---|---|

| Inflation differential | 3m annualized CPI or core, surprise versus consensus | Moves rate path pricing, fast impact |

| Persistence | Core services, trimmed mean, wage growth | Shifts terminal rate and duration, medium impact |

| Terms of trade | Commodity exposure, current account, import prices | Reprices external balance risk, medium to slow impact |

| Productivity | Productivity growth, unit labor costs, investment | Explains long-run real appreciation or decay, slow impact |

Short-run vs long-run: why exchange rates can ignore inflation for months

Risk-on, risk-off, and global liquidity drive the short run

In the short run, FX trades like a risk asset. Inflation can print hot and the currency can still rise or fall for reasons that have nothing to do with consumer prices.

- Risk-on: money moves into higher yield and cyclical currencies. High beta FX can rally even if inflation runs above target.

- Risk-off: money moves into safe havens and funding currencies. Investors buy liquidity first. They worry about drawdowns, not CPI math.

- Global USD liquidity: when dollar funding tightens, USD often strengthens across the board. That can overpower local inflation differences for months.

- Real rates and policy expectations: the market prices the central bank reaction path. A “less hawkish than feared” shift can weaken a currency even with high inflation.

If you want a simple rule for the next few months, track global rates, volatility, and funding conditions before you track PPP models. See what actually moves prices for a broader driver map.

Positioning, momentum, and levels can beat fundamentals

FX moves on flows. Flows respond to positioning and risk limits faster than they respond to slow macro data.

- Positioning: crowded longs or shorts create one-way risk. A small surprise can force a large unwind.

- Momentum: trend systems, CTAs, and algo execution add demand in the direction of the move.

- Technical levels: stops cluster near prior highs, lows, and round numbers. Breaks trigger mechanical buying or selling.

- Hedging flow: exporters, importers, and asset managers rebalance on schedule. These flows can dominate daily and weekly price action.

This is why exchange rates can ignore inflation prints. The market can already hold the trade. The next move comes from who must exit.

Lag effects: inflation takes time to hit FX through wages and trade

Inflation affects currencies through competitiveness, profits, and the external balance. Those channels run slow.

- Prices adjust with contracts: many goods and services prices reset quarterly or annually. CPI can move before business pricing fully resets.

- Wages move slower: wage bargaining and hiring plans react with delays. Unit labor costs change over quarters, not days.

- Trade volumes react last: consumers and firms switch suppliers slowly. Shipping capacity, inventory cycles, and regulation add friction.

- Current account effects lag: higher import prices can worsen the trade balance at first, even before volumes adjust.

| Channel | What you can track | Typical timing |

|---|---|---|

| Inflation surprise | CPI, core, trimmed mean | Immediate |

| Policy reaction pricing | OIS, swaps, futures implied terminal rate | Days to weeks |

| Wage and cost pressure | Wage growth, unit labor costs, PMIs prices paid | Quarters |

| Competitiveness and trade | Export orders, trade balance, current account | Quarters to a year |

Regime shifts reset correlations

During shocks, the market changes the rulebook. Inflation stays on the screen, but it stops being the main driver.

- Crises: banking stress and liquidity events push investors into cash-like assets and safe havens.

- Wars and energy shocks: terms of trade dominates. Energy importers and exporters diverge even if inflation runs high everywhere.

- Policy pivots: a surprise pause, cut cycle, or emergency facility changes rate paths and risk premiums fast.

- Capital controls and intervention risk: governments can change flow dynamics overnight. That breaks clean inflation to FX relationships.

In these regimes, focus on the market’s constraint. Liquidity, collateral, and funding cost set the price. Inflation matters later, when the system stabilizes.

Real-world examples and mini case studies

A high-inflation emerging-market scenario: confidence, reserves, and depreciation

High inflation in an emerging market rarely stays a local story. It hits confidence first. Then it hits reserves. Then it hits the currency.

- Start point: inflation rises fast, wages lag, firms reprice inventory. People move savings into USD or EUR.

- Flow effect: importers buy more foreign currency to secure supply. Exporters delay converting receipts.

- Policy response: the central bank hikes. The government may cap prices or push cheap credit. Markets treat that as fiscal dominance.

- Reserve constraint: the central bank sells reserves to slow the fall. Spot FX stabilizes for weeks or months. The parallel rate keeps moving.

- End state: reserves thin out. The market prices a devaluation risk premium. USD funding cost rises. The currency drops in steps.

Practical check. Track FX reserves, the current account, and the gap between official and parallel rates if one exists. When reserves fall and the gap widens, depreciation risk rises even if policy rates jump.

An advanced-economy tightening cycle: inflation shock and currency repricing

In developed markets, the first driver is the expected rate path. Inflation matters because it changes that path.

- Shock: CPI prints above forecast for several months.

- Repricing: front-end yields rise. Rate differentials move in favor of the higher-yielding currency.

- Capital flows: global investors rebalance into the higher real and nominal carry, especially at the short end.

- FX result: the currency strengthens even before inflation falls, because markets trade the policy reaction.

Example pattern. In 2021 to 2022, the Fed shifted from “transitory” to aggressive hikes. The US dollar strengthened broadly as markets priced a faster and higher terminal rate. Inflation did not need to drop first. Rate expectations did the work.

Use this in your process. Watch the spread between 2-year yields, not just headline CPI. FX often follows the 2-year differential faster than it follows inflation itself.

For a driver framework on one major pair, see what moves EUR/USD.

Energy shock example: import dependence, inflation spike, and FX pressure

Energy shocks hit FX through the trade balance. Importers must buy more foreign currency for the same energy volume. That pushes the domestic currency down.

- Shock: oil or gas prices jump.

- Inflation link: fuel and electricity feed into transport, food, and manufacturing costs.

- Trade link: the import bill rises. The current account worsens.

- FX link: demand for USD rises because energy often settles in dollars. The local currency weakens.

- Policy dilemma: the central bank faces slower growth and higher inflation at once. It cannot fix the terms-of-trade shock with rates.

Mini case. In 2022, Europe faced a gas supply shock. Energy prices surged, inflation rose, and the region’s external balance deteriorated. The euro weakened as the market priced weaker growth and a worse trade position, even as inflation stayed high.

What to track. Net energy import dependence, the trade balance, and one-year inflation swaps. If inflation rises while the trade balance breaks down, FX pressure can persist.

What to learn from outliers (why “this time is different” sometimes is)

Sometimes inflation rises and the currency does not fall. Sometimes inflation falls and the currency still weakens. Outliers usually share one constraint that dominates.

- Credible inflation targeting: markets trust the central bank to cap medium-term inflation. Long-term inflation expectations stay anchored. FX reacts less to a single CPI shock.

- Risk regime: in risk-off moves, safe havens can rise even with worse inflation prints. Funding liquidity wins over macro logic.

- Terms of trade: commodity exporters can see currency strength even with high inflation if export prices surge and the current account improves.

- Financial repression: negative real rates with capital controls can hold the official FX rate stable for a while. The pressure shows up in reserves, forward points, and parallel markets.

- Positioning and valuation: if a currency starts cheap and investors hold short positions, a small policy shift can trigger a large rally.

Your takeaway. Treat inflation as one input. Then rank constraints in this order. Funding liquidity and policy credibility. External balance and reserves. Rate differentials and growth. The top constraint usually sets the FX trend.

How to analyze inflation and currency exchange rates explained (a practical checklist)

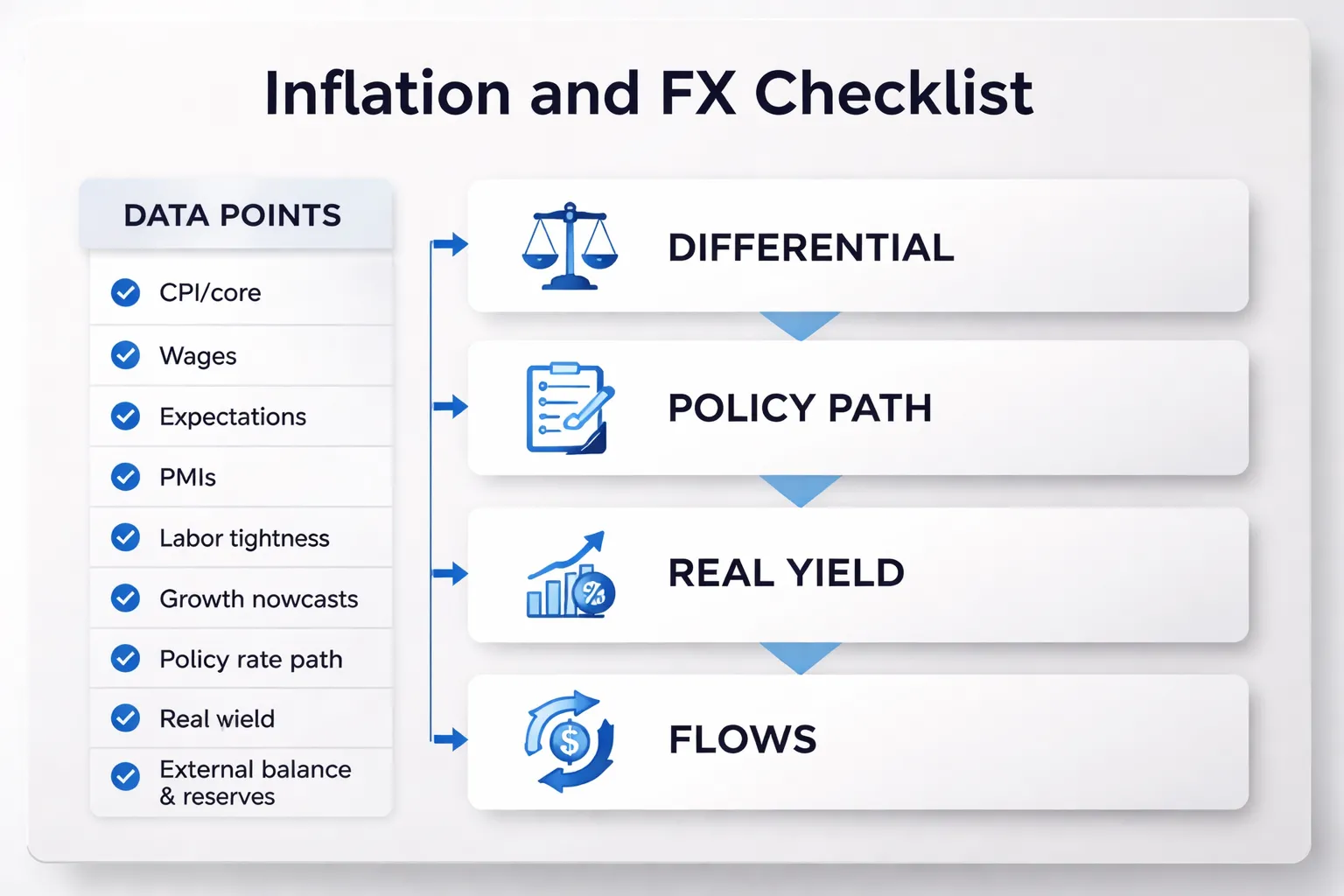

The 10 data points to track

- Headline CPI and core CPI. Track 1M annualized, 3M annualized, and YoY. Watch services ex housing if your country reports it.

- Wages. Use average hourly earnings, negotiated wages, or wage trackers. Compare wage growth to your inflation target plus productivity.

- Inflation expectations. Track 1Y and 5Y survey expectations. Add market based measures like breakevens if available.

- PMIs. Focus on prices paid, output prices, and new orders. Services PMI often leads sticky inflation.

- Labor market tightness. Unemployment rate, vacancies, quits, participation, and hours worked. Tight labor keeps services inflation high.

- Growth nowcasts. Monthly GDP proxies, industrial production, retail sales. Weak growth changes the policy path fast.

- Policy rate and forward guidance. Current rate, next meeting pricing, and the projected terminal rate. Track the reaction function.

- Real yield. Policy rate minus expected inflation. Use 1Y expected inflation or a clean proxy like 12M CPI forecast.

- External balance and funding. Current account, trade balance, terms of trade, and external debt maturity. Add FX reserves and import cover.

- Positioning and flows. CFTC where available, ETF and bond fund flows, and local bond auction demand. A crowded trade moves FX more than data.

A practical checklist, differential to flows

- 1) Start with the differential. Build the inflation gap and rate gap versus the anchor currency. For most pairs, use the US as the anchor.

- 2) Map the policy path. Write two paths, base case and stress case. Use meeting by meeting pricing and your own inflation view.

- 3) Convert to real yield. Compare real rate paths, not just nominal rates. A high nominal rate with high inflation often fails.

- 4) Check credibility. Compare inflation to target and test whether policy looks restrictive. Look for fiscal dominance signals, like rising deficits with no funding plan.

- 5) Check funding liquidity. Watch cross currency basis, swap spreads, and bank funding stress. In stress, the market buys funding currencies first.

- 6) Stress the external account. Ask if the country can fund its deficit without reserve loss. Track reserves, external rollover needs, and commodity import bills.

- 7) Translate into flows. Higher real yield plus stable funding pulls portfolio inflows. Weak credibility or reserves pushes outflows.

- 8) Add positioning. If investors already hold the trade, you need a bigger surprise. If positioning looks light, small surprises can trend.

- 9) Set the catalyst calendar. CPI, wages, PMI prices, central bank meetings, and major labor releases. For USD pairs, align this with what moves GBP/USD when the pound sits on US data and Fed pricing.

- 10) Define invalidation. Pick two numbers that kill your view. Example, core CPI prints below trend for three months, and terminal rate pricing drops 50 bps.

Red flags that inflation will likely weaken the currency

- Inflation rises while real rates fall. Markets see policy behind the curve.

- Core inflation accelerates in services. Central banks struggle to cool it without hurting growth.

- Wages re accelerate. You get persistence and higher inflation expectations.

- Inflation expectations unanchor. Survey and breakevens trend up together.

- FX reserves trend down. The central bank defends the currency, then runs out of room.

- Current account deteriorates. Especially when terms of trade turn against the country.

- Fiscal impulse rises into high inflation. Higher deficits force higher issuance and weaken policy credibility.

- Capital controls and parallel rates appear. The official rate stops reflecting reality, then gaps widen.

- Central bank signals a pivot too early. Cuts begin while inflation momentum still runs hot.

- Risk sentiment turns. High yielders with weak external balance sell off first.

Signals inflation may be peaking, and how FX often reacts first

- Disinflation shows in the short windows. 1M and 3M annualized core roll over before YoY looks clean.

- Goods prices break first. Freight rates fall, inventories rise, and input prices in PMIs drop.

- Wage growth cools. Hours worked fall, vacancy rates drop, and quits slow.

- Inflation expectations flatten. 1Y drops without a rise in 5Y. That signals less tail risk.

- Policy tone shifts from hike size to end game. The bank starts talking about “sufficiently restrictive” and data dependence.

- Real yields stop rising. The market prices fewer hikes even before the central bank confirms it.

- FX moves before the data looks pretty. If the market believes peak inflation is in, it front runs the turn in rate differentials. High yielders can top before CPI peaks, and low yielders can bottom before cuts start.

- Your action. When you see these signals, reduce conviction on “inflation up equals currency down.” Shift focus to the next driver, usually growth risk and the policy path.

Common myths and mistakes about inflation and FX

Myth: “Higher inflation always means a weaker currency”

Markets trade the policy reaction, not the inflation number in isolation.

- If inflation rises and the central bank hikes faster than peers, the currency can strengthen because yield support improves.

- If inflation rises and the central bank stays behind the curve, the currency can weaken because real yields fall and credibility slips.

- If inflation rises because of energy or taxes, growth can slow while prices stay high. That can hurt the currency even if headline CPI looks “strong.”

Your action. Map inflation to the expected rate path and the expected growth hit. Trade the gap versus other central banks.

Myth: “One CPI print determines the exchange rate”

FX prices the whole distribution of outcomes. One release rarely changes the trend by itself.

- Expectations matter more than the level. A “high” CPI can be bullish if the market feared worse.

- Composition matters. Core, services, and wage growth drive policy more than volatile items.

- Positioning matters. If traders already hold the same view, the currency can fall on “good” news because there is no new buyer.

Your action. Track consensus, whisper numbers, and market pricing before the release. Use an economic calendar to line up CPI with central bank meetings and key speeches.

Mistake: ignoring real rates and focusing only on headline inflation

Real yield drives capital flows. Headline CPI does not.

- Real rate equals nominal yield minus expected inflation. You care about the market’s inflation expectation, not last month’s CPI.

- Breakevens and swaps move FX. If inflation expectations rise faster than yields, real rates fall, and the currency often loses support.

- Rate differentials dominate. A country can have high inflation and a strong currency if its real rate stays high versus peers.

Your action. Watch 2-year yields, real yield proxies, and inflation expectations side by side. If real differentials move against your currency, reduce risk even if CPI trends your way.

Mistake: forgetting that FX is a relative price (two economies, two policies)

Every FX pair compares two stories at once.

- Inflation in Country A matters only versus Country B. A hot print helps A only if B looks cooler or less hawkish.

- Policy divergence sets the trend. The pair follows the expected path gap between two central banks, not one.

- Growth and risk can override inflation. When recession risk rises, funding flows can beat carry, even if inflation stays high.

Your action. Build a two-column checklist for each pair, inflation trend, growth momentum, and policy path for both sides. Trade the spread, not the headline.

FAQ

Does higher inflation always weaken a currency?

No. FX prices the reaction. If your central bank hikes faster than the other side, yield support can lift your currency. If inflation spikes and policy stays behind, real yields fall and your currency often drops.

What matters more, inflation or interest rates?

Rates, but in real terms. Track your policy path and your inflation path together. Real yield and expected rate differentials move capital. The spread between two central banks matters more than any single print.

What is the cleanest way to compare two currencies?

Build a two-column checklist. Track inflation trend, growth momentum, and policy path for both sides. Add real yields and next meeting pricing. You trade the gap, not your local headline.

How fast do exchange rates react to inflation data?

Usually within seconds, but the move depends on surprise versus expectations. Your risk regime can mute it. If markets focus on recession or stress, safe-haven and funding flows can dominate for weeks.

Why can a currency rise during high inflation?

Because your central bank stays credible. Markets expect tighter policy, slower demand, and better real returns later. If traders think inflation will fall and rates will stay high, your currency can rally.

What data should you watch each week?

- Inflation: CPI, core CPI, wages, inflation expectations.

- Growth: PMI, jobs, retail sales, GDP trackers.

- Policy: rate decisions, minutes, speeches, OIS pricing.

How do you use PPP without getting trapped?

Use PPP as a long-run anchor, not a timing tool. A currency can stay mispriced for years while carry and growth dominate. Pair PPP with real yield spreads and positioning before you size risk.

Why does growth sometimes beat inflation in FX?

Because capital chases safety and liquidity. When recession risk rises, traders cut risk and pay back funding trades. That can lift low-yield havens and punish high-yielders, even with worse inflation.

What is “policy divergence” in plain terms?

Two central banks move at different speeds. One hikes, the other pauses or cuts. The expected path gap drives the pair. You should track how the next 3 to 8 meetings reprice on both sides.

How do you apply this to GBP/USD?

Compare UK versus US inflation trend, growth momentum, and rate path. Watch real yield spreads and recession risk. Use key fundamentals and market drivers as your weekly checklist.

What is the fastest checklist you can run before a trade?

| Side A | Side B |

| Inflation: rising, flat, falling | Inflation: rising, flat, falling |

| Growth: accelerating, slowing | Growth: accelerating, slowing |

| Policy: hike, hold, cut path | Policy: hike, hold, cut path |

| Real yields: improving, worsening | Real yields: improving, worsening |

Conclusion

Inflation moves currencies through policy and real yields. Higher inflation does not help a currency by itself. What matters is the gap between inflation and rates, and how fast that gap changes.

Focus on the spread. Compare Side A vs Side B on three lines, inflation, growth, policy. Then confirm with one number, real yield direction.

- Currency strength setup: inflation cools or stays controlled, growth holds up, central bank stays tight, real yields improve.

- Currency weakness setup: inflation runs hot, growth fades, central bank turns dovish, real yields worsen.

Your final tip, trade the change, not the level. Track the next CPI print, the next central bank meeting, and the market priced path. If pricing and data diverge, you have an edge. If they match, size down or stand aside.

If you want a wider framework that fits this checklist into a full process, read fundamental analysis in forex explained.

-

How Interest Rates Affect Currency Pairs (With Real Examples)

5 months ago -

Fundamental Analysis in Forex Explained (What Actually Moves Prices)

5 months ago -

What Moves EUR/USD? The Biggest Drivers You Should Watch

5 months ago -

Economic Calendar for Forex: How to Use It (Step-by-Step)

5 months ago -

How to Trade Forex News (NFP, CPI, FOMC) Without Getting Wrecked

5 months ago

-

-

- A high-inflation emerging-market scenario: confidence, reserves, and depreciation

- An advanced-economy tightening cycle: inflation shock and currency repricing

- Energy shock example: import dependence, inflation spike, and FX pressure

- What to learn from outliers (why “this time is different” sometimes is)

-

- Does higher inflation always weaken a currency?

- What matters more, inflation or interest rates?

- What is the cleanest way to compare two currencies?

- How fast do exchange rates react to inflation data?

- Why can a currency rise during high inflation?

- What data should you watch each week?

- How do you use PPP without getting trapped?

- Why does growth sometimes beat inflation in FX?

- What is “policy divergence” in plain terms?

- How do you apply this to GBP/USD?

- What is the fastest checklist you can run before a trade?

-

-

-

- A high-inflation emerging-market scenario: confidence, reserves, and depreciation

- An advanced-economy tightening cycle: inflation shock and currency repricing

- Energy shock example: import dependence, inflation spike, and FX pressure

- What to learn from outliers (why “this time is different” sometimes is)

-

- Does higher inflation always weaken a currency?

- What matters more, inflation or interest rates?

- What is the cleanest way to compare two currencies?

- How fast do exchange rates react to inflation data?

- Why can a currency rise during high inflation?

- What data should you watch each week?

- How do you use PPP without getting trapped?

- Why does growth sometimes beat inflation in FX?

- What is “policy divergence” in plain terms?

- How do you apply this to GBP/USD?

- What is the fastest checklist you can run before a trade?

-

-

How to Place a Forex Trade Step by Step (Your First Trade Explained)

3 months ago -

Forex Trading vs Crypto Trading: Which Market Is Better for Beginners?

3 months ago -

Forex Lot Size Calculator: How to Use It to Size Trades Correctly

5 months ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

5 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

5 months ago

-

Forex Trading Platforms Comparison: MetaTrader vs cTrader vs TradingView

5 months ago -

Is Forex Trading Legal in the United States? Rules, Regulators & What to Know

5 months ago -

Stop Loss vs Take Profit: Differences, Examples & Best Practices

5 months ago -

Forex Market Hours & Trading Sessions Explained (Best Times to Trade)

5 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

5 months ago