Forex Swap Fees (Rollover) Explained: What You Pay and Why

Swap fees, also called rollover, hit your account when you hold a forex position past the daily cutoff time. You either pay or earn interest based on the rate difference between the two currencies, plus your broker’s markup. These charges can turn a “small” overnight hold into a steady cost, especially on leveraged trades.

This guide shows you what swap fees are, when brokers apply them, and how they calculate them. You will learn why Wednesday swaps often post as triple, how long and short swaps differ, and how to estimate the fee before you open a trade. You will also learn simple ways to reduce swap drag and when swap can work in your favor.

If you need a quick refresher on position sizing and how costs scale, read lot size first.

Key Takeaways

Key Takeaways

- In het kort: Swap is the overnight financing cost or credit on leveraged forex positions.

- Brokers apply swap when you hold a trade past the daily rollover cutoff.

- Wednesday often posts as triple swap because it accounts for weekend settlement.

- Long and short swaps differ because each side implies a different funding leg.

- You can estimate swap before you trade by checking your platform’s swap rates and scaling by lot size and nights held.

- Swap can be a cost or a credit, but it can change without warning when rates or broker markups change.

- Swap drag compounds on longer holds, so it matters more for swing and position trades than for intraday trades.

- To reduce swap, shorten holding time, avoid holding over rollover, and choose pairs and directions with lower negative swap.

- Track swap separately from spread and slippage so you see your true carrying cost. Read What Is Slippage in Forex? Causes, Examples & How to Reduce It.

Swap fees in forex and rollover: the core concept

Plain-English definition and why brokers charge or pay it

A forex swap fee is an overnight financing adjustment on an open position.

Your broker applies it when you hold past the daily rollover cut-off.

If the swap is negative, you pay. If it is positive, you receive a credit.

Swap exists because spot FX has a settlement date. When you hold a position overnight, you effectively carry exposure to two interest rates. One for the base currency, one for the quote currency. The swap reflects that rate difference, plus the broker’s markup and any hedging costs.

You see the swap as “Swap Long” and “Swap Short” for each pair in your platform. Long means buy positions. Short means sell positions.

Swap vs spread vs commission vs financing: what’s different

- Spread, the bid-ask gap. You pay it when you enter and exit. It is an execution cost.

- Commission, a fixed fee per lot or per side on some accounts. You pay it on each trade.

- Swap, a daily holding cost or credit. You pay or receive it only if you hold past rollover.

- Financing, the broader label brokers use for the daily carry cost on leveraged products. In spot FX platforms, this usually shows as swap.

Keep them separate in your tracking. Spread and commission hit fast. Swap accumulates every night you stay open.

When rollover is triggered (daily cut-off, platform time zones, DST)

Rollover triggers at a broker-set daily cut-off. Most brokers use 5:00 pm New York time because it lines up with the industry day change for FX.

Your platform may display server time, not your local time. That changes the clock, not the economics.

Daylight saving time can shift what you see by one hour. New York time changes in March and November. Many broker servers adjust. Some do not. Check your broker’s contract specs and server clock.

If you open a trade minutes before cut-off and keep it open after, you can still get charged a full day of swap. If you close before cut-off, you avoid that day’s swap.

Spot FX settlement basics (T+2) and why it creates overnight financing

Spot FX typically settles on T+2. That means a trade done today settles two business days later.

When you hold a spot position overnight, your broker rolls the settlement forward by one day. It closes the old value date and opens a new one. That roll creates a financing adjustment. That adjustment is the swap.

Some pairs follow different settlement rules, such as USD/CAD often using T+1. Holidays in either currency can also shift settlement. That is why swap can change around holidays and month-end.

On the midweek rollover, brokers often apply a multi-day swap to account for weekend settlement. Most apply a triple swap on Wednesday. Some products use different schedules. Your broker’s specs control the exact day.

| Cost type | When it hits | What drives it | How you control it |

|---|---|---|---|

| Spread | Entry and exit | Liquidity, volatility, broker pricing | Trade liquid sessions, use limits, compare brokers |

| Commission | Entry and exit | Account plan | Pick pricing model that fits your lot size |

| Swap (rollover) | Daily at cut-off | Rate differential, broker markup, settlement calendar | Avoid holding over cut-off, choose direction and pair with lower negative swap |

Why swap can be positive or negative (the interest-rate differential)

Base vs quote currency interest, why long and short swaps differ

Every FX pair links two interest rates. The base currency comes first. The quote currency comes second.

If you go long, you hold the base currency and fund it with the quote currency. If you go short, you hold the quote currency and fund it with the base currency.

Your swap tracks that funding gap. Higher yield on what you hold can create a credit. Higher yield on what you fund can create a charge.

- Long EUR/USD, you are long EUR and short USD. Your swap tends to follow EUR rate minus USD rate, minus broker costs.

- Short EUR/USD, you are long USD and short EUR. Your swap tends to follow USD rate minus EUR rate, minus broker costs.

Central bank rates vs money-market rates, why the headline rate is not enough

Swap does not use the policy rate in a clean way. It tracks tradable funding rates used between banks and prime brokers.

Those rates move with, but do not equal, the central bank rate. They also include day-count rules, tenor conventions, and actual funding availability.

- Overnight and tom-next funding can price above or below the policy rate.

- Quarter-end and year-end funding often costs more. Swap can worsen around those dates.

- Collateral terms and credit charges can change the effective rate your broker can access.

Expectations and risk premiums, why swap can shift before rates change

Swap reflects what the market expects next, not just today. If traders price future hikes or cuts, forward points adjust. Swap follows.

Risk premiums also matter. If funding becomes scarce in one currency, lenders demand more. Swap turns more negative for positions funded in that currency.

- Higher expected future rates in the quote currency can raise the cost of being long the base currency.

- Stress periods can add a premium to safe-haven funding. Swap can move fast even if policy rates stay flat.

- Broker markup sits on top. Two brokers can show different swaps on the same pair.

Typical scenarios, high-yield vs low-yield pairs

Interest-rate gaps drive the sign. Broker pricing and market funding decide the final number you see.

| Pair setup | Common swap outcome | What to watch |

|---|---|---|

| High-yield base vs low-yield quote | Long can be less negative or positive, short usually negative | Broker markup can erase the credit |

| Low-yield base vs high-yield quote | Long usually negative, short can be less negative or positive | Funding spikes around roll dates |

| Two similar-rate majors | Small swaps, often negative both directions | Costs and calendar effects dominate |

| Exotic with wide rate gap | Large swings, credits can vanish fast | Liquidity and risk premium can overwhelm the rate gap |

If you trade minors and exotics, learn how pair selection affects swap. See major vs minor vs exotic currency pairs.

How rollover fees are calculated (the practical math)

Key inputs: notional size, swap points, pip value, and account currency conversion

Rollover uses your position size, the broker swap rate, and the value of a point in money terms.

- Notional size, your trade size in base currency. Example, 1.00 lot of EURUSD equals 100,000 EUR notional.

- Swap rate, what your broker charges or pays per day. Many brokers quote this as points or pips per 1 lot.

- Pip value, how much 1 pip is worth for your position size, in the quote currency for most USD pairs. Use a pip value tool if you do not want to do the manual math, see pip value calculator.

- Account currency conversion, if your account currency differs from the swap settlement currency, the platform converts it. The conversion rate changes your final debit or credit.

Swap quoted as points or annualized percent, how to read broker specs

Brokers usually show swap in one of two ways.

- Points or pips per day. Example, Swap Long = -6.2 points, Swap Short = +1.4 points. On many platforms, 10 points equals 1 pip. Check your symbol contract specs.

- Annualized percent. Example, -4.5% per year. The platform converts it to a daily amount using a day-count basis, often 360 or 365. Your broker sets the basis.

If your broker gives points, you can calculate cash swap with pip value. If your broker gives percent, you can calculate cash swap from notional and then convert to your account currency.

Worked example, swap in points for a long and a short (step by step)

Assume EURUSD, 1.00 lot, account currency USD. Contract size is 100,000 EUR. EURUSD price is 1.1000. Broker swap shows points per day.

| Item | Value |

|---|---|

| Position size | 1.00 lot |

| Swap Long | -6.2 points per day |

| Swap Short | +1.4 points per day |

| Point to pip | 10 points = 1 pip |

| Pip value (EURUSD, 1 lot) | about $10 per pip |

Step 1, convert points to pips.

- Long, -6.2 points = -0.62 pips

- Short, +1.4 points = +0.14 pips

Step 2, multiply by pip value.

- Long daily swap = -0.62 pips × $10 per pip = -$6.20

- Short daily swap = +0.14 pips × $10 per pip = +$1.40

Step 3, apply day multiplier when it applies.

- If your broker applies triple swap on the midweek rollover to account for weekend settlement, multiply the daily amount by 3 on that day.

- Long on triple day, about -$18.60. Short on triple day, about +$4.20.

Your platform posts the debit or credit around the broker rollover time. That time follows the broker’s server clock and liquidity session rules, so it can shift around holidays and daylight savings. Align holding periods with the right session, see forex market hours.

Cross-currency conversion and why your account currency matters

Swap often settles in the quote currency. If your account uses a different currency, you get a second conversion.

- If you trade EURJPY, swap accrues in JPY on many platforms. If your account is in USD, the platform converts JPY to USD at its conversion rate.

- Conversion uses a bid or ask spread. That spread adds cost. It also changes with volatility and market hours.

- With small swaps, the conversion spread can turn a small credit into near zero, or deepen a small debit.

Practical check. Look at the symbol contract specs for “swap currency” or “profit currency.” That tells you what you will convert from.

How leverage changes margin but not the underlying notional-based swap

Leverage changes how much margin you post. It does not change the notional size you control.

- Swap uses notional. If you buy 1 lot, you pay or earn swap on the full 100,000 base units.

- Higher leverage can make swap feel larger versus your cash balance, because your margin is smaller.

- Lower leverage does not reduce swap for the same lot size, it only changes your margin and free equity buffer.

If you want to cut rollover cost, reduce lots, shorten holding time across rollover, or pick a pair with a better swap for your direction. Changing leverage alone does not fix the fee.

Triple swap and other calendar effects you must plan for

Triple swap and why it exists

Spot FX uses delayed settlement. Most pairs settle on T+2.

When you hold past the broker’s daily cut-off, your broker rolls your position forward. That roll covers the funding difference between the two currencies.

Markets do not settle on Saturday and Sunday. So one rollover day has to cover multiple calendar days.

- Most FX pairs: triple swap hits on Wednesday at rollover, because Wednesday’s roll moves settlement across the weekend.

- Pairs with different settlement conventions: some instruments can differ. Your broker’s contract spec controls what you pay.

Plan for this. If you hold a high carry cost position, the triple swap day can be your biggest single-day drag.

Holidays and broken weeks

Public holidays change settlement calendars. When banks close, settlement shifts. Rollover can bundle extra days into one charge.

- A Monday holiday can push settlement out. Your rollover earlier in the week may include extra days.

- A holiday in one currency can still affect the pair, even if the other country is open.

- Expect changes around major bank holidays, especially in USD, EUR, GBP, JPY, CHF.

Check your broker’s holiday schedule and instrument notes. Do not assume Wednesday is always the only amplified day.

Year-end and quarter-end funding stress, abnormal spikes

Funding markets tighten around quarter-end and year-end. Banks manage balance sheets. Short-term funding rates can jump.

That pressure can feed into forward points and swap rates. Your rollover can spike for a few sessions, even if central bank rates did not move.

- Expect more noise in the last week of March, June, September, and December.

- Watch for reduced liquidity at the same time, since thin markets can widen pricing.

If your strategy holds positions for weeks, build a buffer for these periods. Do not run your free equity close to zero into calendar stress.

Daylight saving time shifts and cut-off confusion

Rollover posts at a fixed broker cut-off time. That time can shift by one hour when daylight saving time changes in the US or your broker’s server zone.

- Know your broker’s rollover timestamp in your local time.

- Do not open or adjust positions in the 30 to 60 minutes before cut-off if you want to avoid an extra day of swap.

- Track DST change weeks. The cut-off can move even when your local clock does not.

If you scalp near the end of the trading day, treat rollover like a hard deadline. One late fill can turn into a full swap charge.

Rate decisions can change your future rollover costs

Central bank decisions change expected funding. That change flows into forward pricing and then into swap rates.

- A surprise hike can increase the cost of being short the higher-yield currency and improve the swap for being long it.

- A surprise cut can flip the economics the other way.

- Market expectations matter. Swap can start moving before the decision as pricing adjusts.

Before you hold through major decisions, check current swap rates and your broker’s update cadence. You need to know how fast they reprice. If you want a quick primer on the mechanics behind pricing and execution, read how the forex market works.

| Calendar effect | What changes | What you do |

|---|---|---|

| Triple swap | One rollover charges multiple days | Reduce size or avoid holding over the triple day if swap is negative |

| Holidays | Extra days can bundle into one charge | Check holiday schedule, avoid assumptions about timing |

| Quarter-end, year-end | Funding stress can widen swap | Keep extra free equity buffer, expect temporary spikes |

| DST shifts | Cut-off time moves by one hour | Convert cut-off to your local time, avoid last-minute fills |

| Rate decisions | Future swap reprices fast | Recheck swap before and after the event, adjust hold plan |

Where to find swap rates and how to read them before trading

Where to find swap rates before you place a trade

You can only trust the swap shown by your broker for your account, your instrument, and your current trading conditions.

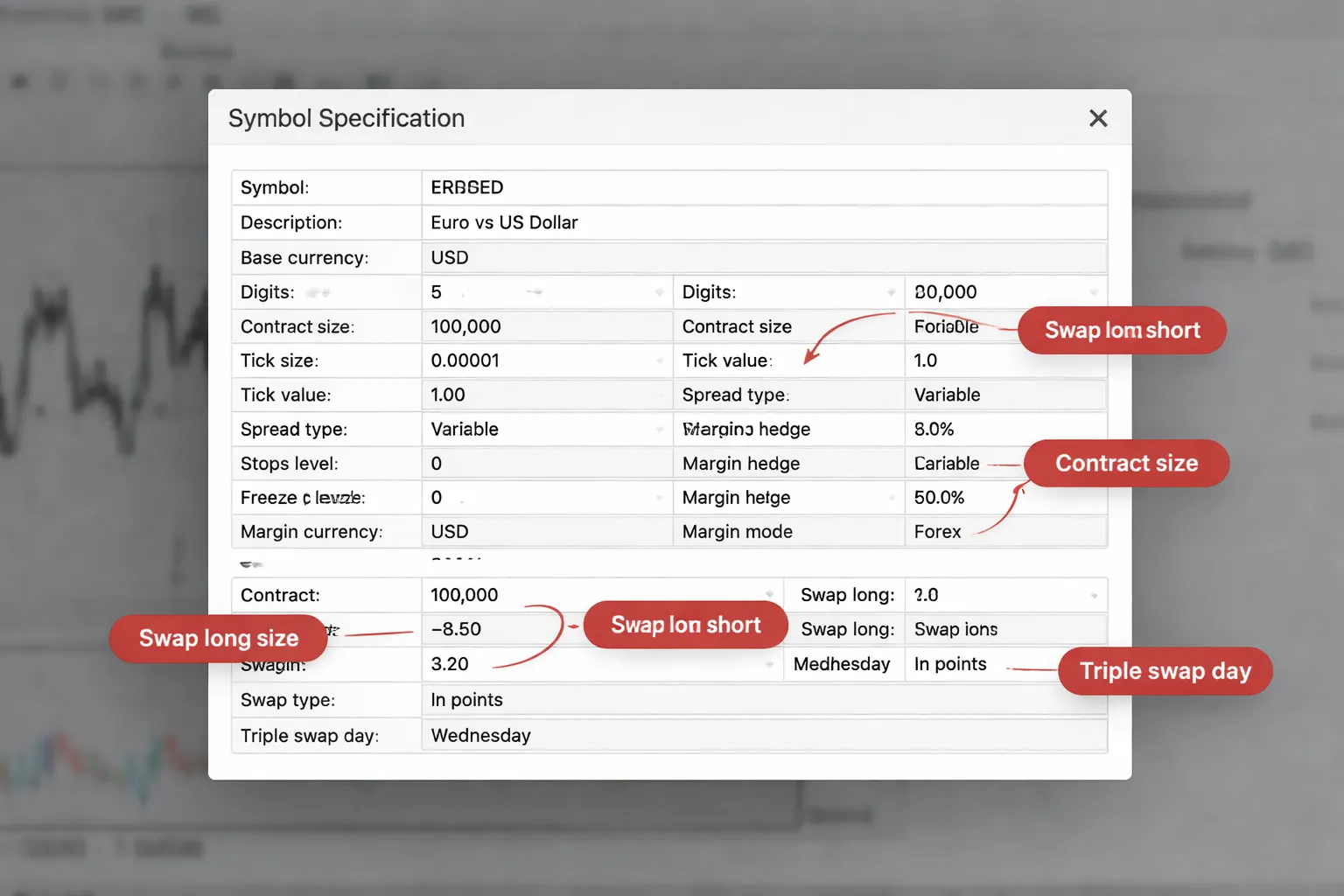

- MetaTrader 4 and 5, open Market Watch, right-click the symbol, select Specification. Look for Swap long, Swap short, and Swap type. Some brokers also show the triple swap day here.

- TradingView, the chart may show an estimated “swap” or “financing,” but it can differ from your broker’s CFD terms. Use it for context, then confirm in your broker platform or contract specs.

- Broker contract specifications, check the instrument page in your broker’s website or client portal. Look for the swap table, cut-off time, triple day, and whether the broker applies markup.

- Inside the order ticket, some platforms show the current swap or daily financing estimate before you click Buy or Sell. If your platform shows it, treat it as the most actionable number.

How to read “swap long” and “swap short”

Swap long applies when you hold a buy position past the rollover cut-off.

Swap short applies when you hold a sell position past the rollover cut-off.

- These values can be positive or negative. Positive means a credit, negative means a charge.

- Long and short swaps usually differ. Do not assume one is the mirror of the other.

- Swap can change daily. Recheck it before you open a position you plan to hold.

Symbol specifications that change what you actually pay

- Contract size (lot size). This sets your position’s notional value. Bigger contract size means bigger swap impact per lot.

- Tick size and tick value. These affect how P and L and fees translate into your account currency. They also help you sanity-check whether the swap shown “per lot” makes sense.

- Swap type. This tells you the unit of the swap number you see. Common types are:

- Points, swap gets converted into money using the symbol’s point value and your position size.

- Money, swap already shows a currency amount per lot per day, often in the quote currency or account currency, depending on the broker.

- Percent, swap charges a rate against notional value. Your cost moves with price and position size.

- Account currency conversion. If the swap is posted in a different currency than your account, your broker converts it. Your final charge can change with FX rates.

- Triple swap day. One day of the week carries three days of swap to cover weekend settlement. Your broker sets which day applies for each asset class.

Quick checklist to estimate multi-day swap cost

- Step 1. Confirm the symbol’s Swap long and Swap short in your platform specs.

- Step 2. Confirm the swap type so you know if the number is points, money, or percent.

- Step 3. Set your direction, buy uses swap long, sell uses swap short.

- Step 4. Convert to “per day” in your account currency if needed. If your platform already shows it in account currency, use that number.

- Step 5. Multiply by the number of nights you expect to hold.

- Step 6. Add one triple day if your holding period crosses it. Count it as two extra days of swap.

- Step 7. Add buffer for changes around events, then check your free margin so a larger-than-expected swap does not trigger a margin issue.

| What you need | Where to read it | What you do with it |

|---|---|---|

| Swap long, Swap short | MT4/MT5 Specification, broker contract specs | Pick the correct field for your direction |

| Swap type | Specification | Know if the number is points, money, or percent |

| Contract size | Specification | Scale swap to your lot size |

| Triple swap day | Contract specs | Apply three days of swap on that rollover |

| Cut-off time | Contract specs | Count nights correctly for your plan |

Broker differences that change rollover costs (and why competitors vary)

Liquidity provider pricing, internalization, and broker markups

Your broker does not invent swap rates from scratch. It builds them from funding costs and then adds its own pricing choices.

- Liquidity provider (LP) funding. Prime brokers and LPs quote tom next and forward points. These inputs shift with central bank rates, money market stress, and currency demand.

- Internalization vs pass-through. A broker can hedge your position externally, or match it internally against other client flow. Internal matching can change the broker’s net exposure, which changes its real funding need.

- Markup model. Many brokers add a spread to swap. Some add it only on one side. Some widen it on less traded pairs. The result is big differences on the same symbol across brokers.

- Risk controls. Brokers may adjust swap around weekends, holidays, or expected volatility. They do this to protect their book and their hedging costs.

- Pair liquidity. Majors usually show tighter swaps than minors and exotics because funding and hedging stay cheaper. This also ties to how pairs trade and settle across regions. See major vs minor vs exotic pairs.

Action step. Compare swap long and swap short for the same symbol and lot size across brokers, on the same day, at the same server time. If the gap stays wide, you are looking at broker pricing, not normal market noise.

Swap-free (Islamic) accounts: common alternative fees and eligibility rules

Swap-free rarely means free to hold trades. Many brokers replace swap with other charges.

- Fixed nightly fee. A set amount per lot per night, often different by symbol.

- Admin fee after grace period. Zero cost for a few days, then a daily fee starts.

- Wider spreads or higher commission. The cost moves from rollover into entry and exit pricing.

- Symbol restrictions. Brokers may allow swap-free on majors but block exotics, metals, or indices.

- Holding limits. Some brokers cap how long you can hold, or they review accounts that hold too long.

- Eligibility checks. Many require approval, documents, and a region-based or religion-based policy. Some allow it for all clients but enforce strict product limits.

Action step. Read the swap-free schedule line by line. Find the fee type, the grace period, the symbols covered, and the maximum holding rule. Treat it as a different pricing plan, not a free upgrade.

CFDs vs spot FX vs futures: how overnight financing differs by product

The product you trade sets the funding logic. Two charts can look identical, but the carry cost can differ.

- Spot FX on MT4 or MT5. You pay or receive swap based on the broker’s tom next and markup. Triple swap applies on the broker’s rollover day.

- FX CFDs. Many brokers still label it swap, but it acts like CFD financing. The broker can price it off an internal rate plus a spread, and it can vary more by broker policy.

- Index and commodity CFDs. Overnight cost often uses a benchmark rate plus broker markup, applied to notional value. Dividends on indices can also affect overnight adjustments.

- FX futures. Financing sits inside the futures price via the forward curve. You do not pay a daily swap line item. You still face roll cost when you move from one contract month to the next.

Action step. Do not compare swap across different products and assume it is the same fee. Compare like with like, same symbol, same product type, same contract size.

Negative swap on both sides: when it happens and what it signals

Sometimes you pay swap whether you buy or sell. That is real. It signals a cost stack that overwhelms any rate advantage.

- Large broker markup. The broker widens both long and short swap so both become negative.

- High hedging costs. On thin or risky pairs, the broker’s external funding cost can rise enough that neither side earns carry.

- Borrow constraints. If it is hard to borrow one currency, or demand to hold one side spikes, the implied funding can turn against both directions after fees.

- Protection against carry abuse. Some brokers price swaps to stop long-term carry strategies on their platform.

Action step. Treat negative swap on both sides as a warning for swing holds. If your plan needs multi-day positions, pick symbols and brokers where at least one side has fair carry, or keep holds shorter and plan exits before rollover.

Trading strategies and risk management around swap fees

Build swap into expectancy for swing and position trades

Your strategy has a holding-time distribution. Swap turns that time into a cost or a yield. Put it in your expectancy model.

- Track average hold time in nights, not in days. A trade closed before cutoff pays zero nights.

- Convert swap to pips so it matches your stop and target. Use: swap_per_night_in_account_currency ÷ pip_value = swap_pips_per_night.

- Adjust expectancy. Expected swap per trade = average_nights_held × expected_swap_per_night.

- Set minimum edge. If your average win is 25 pips and swap costs 0.7 pips per night for 5 nights, swap takes 3.5 pips. Your system must cover it.

If your broker quotes swap in cash, you need pip value to standardize it. Use a pip value calculator to avoid wrong sizing.

Time entries and exits around the rollover cut-off

One minute can decide if you pay an extra night. Treat the rollover time like a fee boundary.

- Know the server cutoff. Many brokers use 5 pm New York time, some use server midnight. Confirm it in the platform.

- Avoid accidental holds. If you plan a day trade, exit before cutoff. Do not let a small delay turn into a paid overnight.

- Plan for triple swap. One weekday often books three nights to cover weekend settlement. Do not hold through that cutoff unless you want that exposure.

- Watch widening costs near cutoff. Spreads can widen and liquidity can thin. A tight stop can trigger on noise.

Position sizing with holding time, make swap a planned expense

Swap scales with position size and nights held. Treat it like interest on leverage.

- Budget swap in currency. Max_swap_budget = account_balance × swap_budget_percent.

- Estimate worst case. Worst_swap = position_size × max_nights × worst_expected_swap_per_night.

- Size from the budget. If worst_swap exceeds the budget, cut size or reduce hold time.

- Link to stop risk. Keep swap small versus your planned loss. If swap can add 10 to 30 percent to a stopped-out loss, your size is too big for the holding period.

Carry trade basics, earning rollover vs drawdown and regime risk

Positive swap looks like income. Price moves can erase it fast.

- Separate two returns. Total return = price return + swap return.

- Stress test drawdown. A pair can move against you far more than daily swap can pay back. Model a shock move and check margin impact.

- Expect swap to change. Brokers update swap rates as funding conditions and policy rates change. Your edge can disappear.

- Watch risk-off regimes. In risk-off periods, high yield currencies can drop hard. Carry can lose in days what it earned in months.

Hedging and netting, when offsetting positions reduce swaps and when they do not

Many traders hedge to cut directional risk. It often does not cut swap.

- Netting accounts. If your platform nets positions, opposite trades reduce or close your net exposure. Swap usually applies to the net position only.

- Hedging accounts. If your platform holds both legs, many brokers charge swap on both positions. You can pay twice for a flat book.

- Partial offsets. If you hedge only part of the size, swap still applies to the remaining net exposure, and may still apply to each leg depending on broker rules.

- Before you hedge. Check the broker policy for “hedged margin” and “swap on hedged positions”. Test it on a demo with a small position across one rollover.

| Goal | Best approach | Swap risk to watch |

|---|---|---|

| Swing holds | Model swap in pips, size for nights | Triple swap and changing rates |

| Carry | Target positive swap with strict drawdown limits | Regime shifts and funding changes |

| Hedging | Use netting when possible, verify broker swap rules | Double swap on both legs |

Advantages and disadvantages of rollover (a balanced view)

Potential benefits

Rollover can work for you when swap is positive. You earn carry each night you hold. This can add up on long holds, especially on higher interest rate differentials and larger position sizes.

Positive carry can also align with macro trends. When rates diverge, the higher yielding currency can stay supported for months. You can then earn swap while you wait for the trend to play out. You still need a stop. Carry trades can unwind fast.

- Carry income: Positive swap can reduce your breakeven level on a multi-day hold.

- Patience reward: You can get paid to hold when the rate differential stays in your favor.

- Strategy fit: Swap matters most for swing and carry setups that hold through rollover often.

Key drawbacks

Negative swap compounds holding costs. Every rollover pushes your breakeven farther away. Many traders ignore this until the position turns into a long hold.

Swap rates can change without warning. Brokers update them as funding conditions change. A trade that paid swap last month can start charging swap next week.

Volatility shocks can erase months of carry. Central bank surprises, inflation prints, and risk-off events can move price far more than your daily swap. Triple swap can also hit harder than expected if you hold across it.

- Cost drift: Your net P and L bleeds each night on negative swap.

- Rate risk: Your expected swap can flip sign after a broker update.

- Gap risk: Large moves can dominate swap, even on “safe” carry pairs.

- Calendar risk: Triple swap days magnify both credits and charges.

Common misconceptions and what’s true

- “Swap is just broker profit.” Swap mainly reflects funding rates, the pair’s rate differential, and the broker’s markup. Your broker can add a spread. You should still treat it as a real cost or income line item.

- “If my swap is positive, the trade is safer.” Positive swap does not reduce price risk. A single trend reversal can outweigh many nights of carry.

- “Hedging cancels swap.” Two legs often mean two swaps. If both legs carry negative swap, you pay on both. Netting rules vary by broker and account type.

- “Swap is fixed.” It changes with funding markets, central bank guidance, and broker policy. Model it, then re-check it.

When swap matters most

Swap matters most when price moves little and you hold for many rollovers. In low-volatility ranges, swap can be a large part of your net result. It can turn a small winner into a loser, or the reverse.

In high-volatility periods, swap matters less than price movement. A large daily range, a gap, or a news-driven move will dominate your P and L. Still, triple swap can add a sudden jump in cost if you stay exposed.

| Market condition | Swap impact | What to do |

|---|---|---|

| Low volatility, range-bound | High. Swap can decide net outcome. | Include swap in your breakeven and time-in-trade plan. Size for nights held. Use a position sizing method that accounts for holding cost. |

| Trending with stable rate outlook | Medium to high. Positive carry can help. | Use swap as a tailwind, not a thesis. Re-check swap after rate announcements and broker updates. |

| High volatility, event risk | Low. Price dominates, but triple swap can sting. | Prioritize gap risk and liquidity. Avoid holding marginal setups through rollover if swap is negative. |

Troubleshooting: why your swap charge looks “wrong”

Time zone and server-time mismatches

Swap applies at your broker’s rollover time, based on server time. Your chart time and your local time can differ. This creates trades that “look” like they avoided rollover but still got charged.

- Rollover cut-off: Many brokers roll at 17:00 New York time, but they post it as a server-time timestamp.

- Daylight saving shifts: In March and November, New York and your broker server may shift on different dates. Your rollover hour can move by 1 hour for weeks.

- Open and close around cut-off: If you open at 16:59 NY and close at 17:01 NY, you can still book swap, depending on how the broker snapshots positions.

Lot size, symbol suffixes, and contract spec changes

Most “wrong swap” claims come from trading the wrong instrument, the wrong contract size, or holding through a spec update.

- Lot size mismatch: Swap scales with volume. 1.00 lot vs 0.10 lot changes swap by 10x. Verify your exact volume on the deal record.

- Symbol suffixes: EURUSD and EURUSD.m can use different liquidity, markups, and swap tables. You must check swap on the exact symbol you traded.

- Contract size differences: Some brokers use non-standard contract sizes on certain accounts. That changes pip value and swap in money terms.

- Spec changes after rollover: Brokers can update swap rates, margin, or trading conditions daily. Your position uses the rate in effect at the rollover timestamp, not the rate you see later.

If your exposure came from a larger position than you intended, fix your sizing process. Use this guide on position sizing to align lots with your risk.

Currency conversion and rounding in statements

Your platform often shows swap in points first, then converts it into your account currency. Small gaps appear from conversion and rounding.

- Account currency conversion: If your account runs in USD and you trade EURJPY, your swap may convert from JPY to USD using a broker rate at posting time.

- Different conversion price than your chart: Brokers can use bid, ask, or mid for conversion. They can also use an internal rate feed.

- Rounding: Platforms round swap in points, then again in money. Micro lots can show “odd” cents. High volumes can amplify tiny rounding rules.

Corporate actions and roll adjustments on CFDs

Some instruments post costs that look like swap but come from corporate actions or contract rolls.

- Index and stock CFDs: Dividends and financing adjustments can post as separate entries or net into overnight financing.

- Commodity and futures-style CFDs: When the underlying rolls from one futures month to the next, the broker can apply a roll adjustment. This can hit PnL even if price looks stable on your chart.

- Crypto CFDs: Funding or overnight fees can change fast and may apply every day, including weekends, depending on the broker model.

Check the instrument’s contract specs page. Look for “dividend adjustment,” “financing,” “rollover,” or “expiration and roll” notes.

How to audit a swap charge step by step

Do not rely on the terminal summary line. Audit from the deal level and match it to the broker’s published rates.

- 1) Export the trade record: Pull the account statement and include deal IDs, open time, close time, volume, symbol, and swap.

- 2) Confirm you held through rollover: Compare open and close timestamps to the broker’s rollover time in server time.

- 3) Check day count: Count how many rollovers you crossed. Add triple-swap day if your broker applies it and confirm which weekday it uses.

- 4) Pull the swap rate table: Use the broker’s “Swap long” and “Swap short” for that symbol and date. Do not use a generic pair page for a suffixed symbol.

- 5) Recreate the money value: Apply the broker method, points-per-lot or percent, then convert into your account currency using the broker’s conversion rate logic.

- 6) Match posting time: If the broker updated swaps at end of day, use the rate valid at the rollover timestamp, not the rate shown now.

- 7) Escalate with evidence: Send the deal ID, timestamps, symbol, volume, and your calculation. Ask for the exact swap rate and conversion price used.

If your numbers still do not reconcile, treat it as a broker-specific calculation rule. Get the written formula from support and store it. Use it for future holds.

Compliance, taxes, and record-keeping considerations

How swaps show up on your statements

Brokers label swaps in different ways. You need to map the labels to one cost bucket.

- Common names: Swap, Rollover, Financing, Overnight fee, Tom-next, Carry, Interest adjustment.

- Where you see them: Trade history, daily cash adjustments, account ledger, or a separate “financing” report.

- What to capture: Deal ID, symbol, direction, volume, open time, close time, rollover timestamps charged, swap per day, triple-swap day rule, and the conversion rate used.

- How it posts: As a credit or debit to balance, sometimes netted into P&L, sometimes shown as a separate cash entry.

- How to reconcile: Match each swap line to the position that stayed open through rollover. If your broker splits positions, you will see multiple swap lines for one idea.

Taxes and documentation for your accountant

Tax rules vary by country and product type. You cannot assume swaps count as “interest” everywhere. You can control your records.

- Export the raw data: Monthly statements, full account ledger, and trade-by-trade history in CSV. Keep the broker’s daily swap rate table if available.

- Store the key fields: Instrument, contract size, volume, timestamps, realized P&L, swap/financing amounts, commissions, spreads if reported, deposit and withdrawal history, and base currency conversions.

- Separate costs: Track swap/financing apart from commissions and spreads. Your accountant may need different categories.

- Track currency effects: Keep the broker’s conversion rate used on each swap posting. FX conversion can change the taxable number in your home currency.

- Document intent and system: Keep your method for calculating expected swap, plus the broker formula you received from support. This supports consistent treatment year to year.

You should treat your broker statement as the primary source, then use your own logs to validate and explain differences.

Why clear fee disclosure improves your strategy decisions

Swap is part of your expected return. If you ignore it, you misprice hold time.

- Compare brokers: Two identical spreads can produce different outcomes if financing differs.

- Evaluate holding periods: A strategy that looks profitable on intraday backtests can fail when you hold through multiple rollovers.

- Measure true risk: Financing can increase drawdown during slow moves, even when price stays near entry. This matters for margin and liquidation risk, see margin call vs stop out.

- Audit execution: Transparent swap posting lets you spot broker-specific rules, symbol-specific rates, and conversion spreads that change your net edge.

Risk note: swap rates change and are not guaranteed

Swap rates can change daily. Brokers can update them without prior notice. Central bank moves, liquidity conditions, and broker markups can all change your cost.

- Do not project last week’s swap into next month’s holds.

- Re-check the swap table before you enter a trade you plan to hold overnight.

- Expect different charges around weekends and holidays due to settlement conventions.

FAQ

What is a forex swap fee?

A swap fee is the interest adjustment you pay or receive when you hold a forex position past your broker’s rollover time. It reflects the rate difference between the two currencies, plus any broker markup. It posts to your account as a daily debit or credit.

When do swap fees apply?

Swap applies when your trade stays open at rollover, usually once per trading day. Close the position before rollover and you avoid that day’s swap. If you open after rollover, you start accruing swap on the next rollover.

Why do I sometimes get a swap credit?

You get a credit when the interest rate difference favors your position after the broker’s markup. It is more common when you buy the higher yielding currency against the lower yielding one. Credits can flip to charges when rates or markups change.

How do brokers calculate swap?

Brokers set a long swap and short swap for each symbol. They convert the result into your account currency and apply it to your position size. Many also include a spread or financing markup. Check the instrument specs and daily swap table inside your platform.

What is triple swap?

Triple swap applies one day per week to cover weekend settlement. Many brokers charge or credit three days at once on Wednesday, but the day can vary by broker and instrument. Holidays can add extra days. Confirm the schedule on your broker’s contract specs.

Do swap rates change?

Yes. Swap rates can change daily. Central bank decisions, money market funding costs, and liquidity shifts move the base rate. Your broker can also change markup. Re-check swap before you place a trade you plan to hold overnight.

Is swap the same as the spread or commission?

No. Spread and commission hit when you enter and exit. Swap hits only if you hold through rollover. You can have a low spread and still pay high swap on long holds. Track all three costs before you choose a strategy.

Where do I see the swap on my account?

You will see it in your trade history or account statement as “swap,” “rollover,” or “financing.” It posts at or shortly after rollover. If you hold multiple days, you will see multiple entries. Export statements to audit longer holding periods.

How can I reduce swap costs?

- Trade pairs with lower negative swap on your direction.

- Avoid holding through triple swap and holidays.

- Use smaller position sizes for longer holds.

- Re-check market session timing in forex market hours.

Do “swap-free” accounts remove all overnight costs?

Not always. Some brokers replace swap with an admin fee, wider spreads, or time limits. Terms can vary by symbol and holding duration. Read the fee schedule and test with a small position. Compare total costs, not the label.

Why is swap different across brokers?

Brokers source liquidity and hedging at different rates. They apply different markups and conversion methods. Some publish raw rates, others smooth them. Platform settings and account currency also change the final number. Compare swap tables for the exact symbol you trade.

Conclusion

Conclusion

Swap is the interest cost or credit for holding a leveraged FX position overnight. It can change your trade outcome if you hold for days or weeks.

Control it. Check the swap table for your exact symbol, direction, and account currency. Note the triple swap day. Convert the swap into your account currency and into pips so you can compare it to your spread and commission.

- Avoid surprises: Know your broker's rollover cutoff time and keep a calendar for holidays and triple swap.

- Plan holding time: If swap is negative, shorten holds or trade the direction with the smaller charge.

- Compare brokers: Test with a small position and record the real nightly debit or credit.

Final tip. Treat swap like any other risk variable. Build it into your position size and your expected return, then only hold trades overnight when the math still works. Use this position sizing guide to quantify the impact before you place the trade.

-

Forex Leverage Explained: How It Works, Pros, Cons & Examples

1 month ago -

Forex Market Hours & Trading Sessions Explained (Best Times to Trade)

1 month ago -

What Is a Lot Size in Forex? Lot Types + Quick Examples

1 month ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

1 month ago -

What Are Pips in Forex? Definition, Examples & Why They Matter

1 month ago

-

- Key inputs: notional size, swap points, pip value, and account currency conversion

- Swap quoted as points or annualized percent, how to read broker specs

- Worked example, swap in points for a long and a short (step by step)

- Cross-currency conversion and why your account currency matters

- How leverage changes margin but not the underlying notional-based swap

-

- Build swap into expectancy for swing and position trades

- Time entries and exits around the rollover cut-off

- Position sizing with holding time, make swap a planned expense

- Carry trade basics, earning rollover vs drawdown and regime risk

- Hedging and netting, when offsetting positions reduce swaps and when they do not

-

- What is a forex swap fee?

- When do swap fees apply?

- Why do I sometimes get a swap credit?

- How do brokers calculate swap?

- What is triple swap?

- Do swap rates change?

- Is swap the same as the spread or commission?

- Where do I see the swap on my account?

- How can I reduce swap costs?

- Do “swap-free” accounts remove all overnight costs?

- Why is swap different across brokers?

-

- Key inputs: notional size, swap points, pip value, and account currency conversion

- Swap quoted as points or annualized percent, how to read broker specs

- Worked example, swap in points for a long and a short (step by step)

- Cross-currency conversion and why your account currency matters

- How leverage changes margin but not the underlying notional-based swap

-

- Build swap into expectancy for swing and position trades

- Time entries and exits around the rollover cut-off

- Position sizing with holding time, make swap a planned expense

- Carry trade basics, earning rollover vs drawdown and regime risk

- Hedging and netting, when offsetting positions reduce swaps and when they do not

-

- What is a forex swap fee?

- When do swap fees apply?

- Why do I sometimes get a swap credit?

- How do brokers calculate swap?

- What is triple swap?

- Do swap rates change?

- Is swap the same as the spread or commission?

- Where do I see the swap on my account?

- How can I reduce swap costs?

- Do “swap-free” accounts remove all overnight costs?

- Why is swap different across brokers?

-

Forex Lot Size Calculator: How to Use It to Size Trades Correctly

1 month ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

1 month ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

1 month ago -

Margin vs Leverage in Forex: What’s the Difference?

1 month ago -

What Is Forex Trading? A Beginner’s Guide to How It Works

1 month ago

-

Forex Leverage Explained: How It Works, Pros, Cons & Examples

1 month ago -

Forex Market Hours & Trading Sessions Explained (Best Times to Trade)

1 month ago -

Is Forex Trading Legal in the United States? Rules, Regulators & What to Know

1 month ago -

What Is a Lot Size in Forex? Lot Types + Quick Examples

1 month ago -

Forex Trading Platforms Comparison: MetaTrader vs cTrader vs TradingView

1 month ago