Major vs Minor vs Exotic Currency Pairs: Differences + Examples

Every forex trade uses a currency pair. That pair falls into one of three buckets, major, minor, or exotic. The label affects your costs, your fills, and your risk.

In this guide, you will learn what defines each group, which currencies qualify, and how brokers and traders use these categories. You will also see clear examples of major pairs like EUR/USD, minor pairs like EUR/GBP, and exotic pairs like USD/TRY. We will break down the key differences that matter in practice, liquidity, typical spreads, volatility, and session behavior. You will leave with a simple way to pick pair types that match your strategy and account size, and avoid pairs that can break your risk plan.

If you want the core driver behind most of these differences, start with forex liquidity.

Key Takeaways

- Summary: Majors: Highest liquidity. Typically the lowest spreads. Best choice for tight stops, higher frequency trading, and accounts where costs matter most.

- Minors: No USD leg, examples include EUR/GBP and AUD/NZD. Liquidity is lower than majors. Spreads are often wider. Moves can be sharp during local data releases.

- Exotics: One major currency plus an emerging market currency, examples include USD/TRY and USD/ZAR. Expect wider spreads, more slippage, and larger gap risk, especially around news and off hours.

- Liquidity drives everything: lower liquidity increases spread, increases slippage, and weakens stop execution. This is the main reason majors behave “cleaner” than exotics.

- Match pair type to strategy: scalping and short term systems fit majors. Swing trading can work on minors if you plan for wider spreads. Treat exotics as specialist instruments and reduce size.

- Respect leverage and margin: volatile pairs plus leverage can trigger fast drawdowns and forced liquidations. Use conservative position sizing and understand your margin limits. Read Margin Call vs Stop Out.

| Pair type | Typical liquidity | Typical spread | Volatility and gaps | Best use |

|---|---|---|---|---|

| Major | High | Low | Lower gap risk | Cost sensitive trading, tighter stops |

| Minor | Medium | Medium | Can spike on regional news | Directional trades, diversification from USD |

| Exotic | Low | High | Higher gap and slippage risk | Advanced setups, smaller size, wider stops |

Currency pairs 101: base/quote, pips, and what a price means

How to read a forex quote, base and quote currency

A currency pair quote has two parts.

- Base currency, the first code. This is what you buy or sell.

- Quote currency, the second code. This is what you pay or receive.

Example: EUR/USD = 1.0850.

- 1 euro costs 1.0850 US dollars.

- If EUR/USD rises, the euro strengthens vs the dollar.

- If EUR/USD falls, the euro weakens vs the dollar.

Most pairs quote to 4 decimals. JPY pairs usually quote to 2 decimals.

Pips, pipettes, and spreads, the real cost

A pip is the standard price step.

- Most pairs, 1 pip = 0.0001.

- JPY pairs, 1 pip = 0.01.

A pipette is one tenth of a pip.

- Most pairs quote 5 decimals. The last digit is a pipette.

- JPY pairs often quote 3 decimals. The last digit is a pipette.

The spread is the gap between bid and ask. It is your transaction cost in pips.

Cost formula in your account currency depends on position size and the pair. For USD-quoted majors, you can treat it as simple math.

- Example, EUR/USD spread = 1.2 pips.

- Standard lot is 100,000 EUR, pip value is about $10 per pip.

- Entry cost is about 1.2 x $10 = $12.

Bid and ask pricing, why you pay the spread

You always see two prices.

- Bid, the price you can sell at.

- Ask, the price you can buy at.

If you buy, you enter at the ask. If you sell, you enter at the bid. Right after entry, your position shows a loss close to the spread. Price must move in your favor by at least the spread to reach break even.

Wider spreads hit harder on low liquidity pairs. That is one reason exotics demand smaller size and wider stops.

Lot sizes and notional exposure

Lots set your trade size. They drive pip value, risk, and margin use.

- Micro lot, 0.01 = 1,000 units of the base currency.

- Mini lot, 0.10 = 10,000 units of the base currency.

- Standard lot, 1.00 = 100,000 units of the base currency.

Example: you buy 0.10 lots of EUR/USD. Your notional is 10,000 EUR. Your pip value is about $1 per pip.

How profit and loss is calculated across quote conventions

P and L starts with pip value. Pip value changes based on where USD sits in the pair.

| Pair type | Example | Pip value rule (1 standard lot) | Quick number |

|---|---|---|---|

| USD is the quote | EUR/USD | About $10 per pip | 1 pip on 100,000 EUR is $10 |

| USD is the base | USD/JPY | Pip value in USD changes with price | At 150.00, 1 pip is about $6.67 |

| Cross pair | EUR/GBP | Pip value is in GBP, then convert to your account currency | If account is USD, you also need GBP/USD |

Simple P and L method:

- Find the move in pips.

- Multiply by pip value for your lot size.

- Subtract spread and any other costs.

If you want a deeper read on why costs change with liquidity and execution, see forex liquidity explained.

What defines major vs minor vs exotic currency pairs (the practical classification)

Liquidity is the core differentiator: depth, order flow, and slippage

In practice, brokers label pairs by how easy they are to trade at size without moving price.

- Major pairs sit on the deepest liquidity. You get tighter pricing, faster fills, and less slippage in normal conditions.

- Minor pairs have solid liquidity, but less depth than majors. Slippage shows up sooner when you trade larger size or during news.

- Exotic pairs have thin liquidity. You see wider pricing, partial fills, and bigger slippage, especially outside local market hours.

Liquidity is not a label, it is order flow. More active buyers and sellers at each price level means your trades hit less friction.

Transaction costs: typical spread ranges and commissions by pair type

Your main day-to-day cost is spread. On some accounts you also pay commission, but the pattern stays the same, majors cost less to trade than exotics.

| Pair type | Common examples | Typical spread range (normal market) | What to expect on costs |

|---|---|---|---|

| Major | EUR/USD, USD/JPY, GBP/USD, AUD/USD, USD/CAD, USD/CHF, NZD/USD | ~0.1 to 1.5 pips | Lowest spreads. Best execution quality. Commission accounts often shine here. |

| Minor | EUR/GBP, EUR/JPY, GBP/JPY, AUD/JPY, EUR/AUD | ~0.8 to 4 pips | Higher spread than majors. Costs jump during sessions with low overlap. |

| Exotic | USD/TRY, USD/ZAR, USD/MXN, EUR/TRY, USD/THB | ~10 to 100+ pips | Spread can dominate your P and L. Many brokers add extra markups and wider minimum spreads. |

Spreads expand around news, rollovers, and thin hours. Exotics can stay wide even when nothing happens.

Volatility and gap risk: when price jumps matter more than spreads

For majors, the spread is often the main cost. For exotics, the price jump is often the main risk.

- Majors move a lot during high-impact data, but deep liquidity often limits gaps in normal trading hours.

- Minors can spike harder than majors because fewer orders sit in the book, especially on crosses tied to risk sentiment.

- Exotics can gap on policy headlines, capital controls, and local market shocks. Stops can fill far from your price.

When volatility rises, execution quality matters more than the quoted spread.

Market accessibility: trading hours, broker availability, and liquidity providers

Access depends on who makes prices and when they want to hold risk.

- Majors trade well across all major sessions. Most brokers offer multiple liquidity providers and stable pricing.

- Minors trade best when at least one of the currencies is in its active session. Outside that window, spreads widen and slippage increases.

- Exotics often rely on fewer liquidity providers. Some brokers restrict leverage, widen spreads sharply, or disable trading during local events.

If your broker runs a smaller liquidity pool, a pair can behave like a lower tier even if it looks popular on a chart.

Why classifications can differ slightly across brokers and data providers

There is no single global rulebook. Labels change because the data behind them changes.

- Volume source differs. One provider uses interbank data, another uses retail flow, another uses futures proxies.

- Broker liquidity differs. A broker with strong LP coverage can treat some minors like majors on pricing.

- Local demand matters. A pair can be “minor” globally but liquid on a regional broker.

- Time of day matters. A pair can trade like a major during session overlap, then trade like a minor in dead hours.

Use the label as a shortcut, then verify with live spread, typical slippage, and fill quality. For a practical shortlist, see best forex pairs for beginners.

Major currency pairs: definition, list, and real-world examples

What makes a pair a “major”

A major currency pair includes the US dollar, USD. It also draws constant global demand from banks, funds, corporates, and hedgers.

You can treat a pair as a major when you see three things on your platform, tight spreads, deep liquidity, and consistent fills across most sessions. You still verify live conditions. Your broker and time of day can change the real cost.

If you want the mechanics behind pricing and liquidity, see how the forex market works.

Common list of major currency pairs

- EUR/USD, euro vs US dollar

- GBP/USD, British pound vs US dollar

- USD/JPY, US dollar vs Japanese yen

- USD/CHF, US dollar vs Swiss franc

- AUD/USD, Australian dollar vs US dollar

- USD/CAD, US dollar vs Canadian dollar

- NZD/USD, New Zealand dollar vs US dollar

Real-world quote examples, how to read them

A quote tells you how much the quote currency costs for 1 unit of the base currency.

| Pair | Example quote | Meaning | If the price rises |

|---|---|---|---|

| EUR/USD | 1.0850 | 1 euro costs 1.0850 US dollars | EUR strengthens vs USD |

| USD/JPY | 148.20 | 1 US dollar costs 148.20 Japanese yen | USD strengthens vs JPY |

Keep your direction clear. If you buy EUR/USD, you go long EUR and short USD. If you buy USD/JPY, you go long USD and short JPY. The base currency drives your P and L direction.

Typical use cases for majors

- News trading, majors often absorb large flows better. You usually get tighter spreads before the release, then wider spreads and faster price moves at the print.

- Intraday strategies, majors suit short holding times because transaction costs tend to stay lower. You can scale in and out with less slippage in liquid hours.

- Hedging global exposure, USD sits in many cash flows. Traders and businesses use majors to hedge dollar revenue, costs, or portfolio risk, such as USD/JPY for Japan exposure or USD/CAD for Canada exposure.

Pros and cons of major pairs

- Pro, lower trading costs, majors usually show the tightest spreads and best fill quality.

- Pro, high liquidity, you can place larger orders with less price impact, especially during London and New York hours.

- Con, crowded trades, the same technical levels and headlines attract many traders. Stops can cluster.

- Con, correlation spikes, in risk-on or risk-off moves, majors can start moving together. Your “diversified” basket can behave like one trade.

- Con, event risk still hits, spreads can jump around central bank decisions and major data releases. Your execution can degrade even on EUR/USD.

Minor currency pairs (crosses): definition, categories, and examples

Minor currency pairs, what “cross” means

A minor pair is a currency pair that does not include USD. Traders also call it a cross, or cross pair.

Crosses exist because the market can quote and trade EUR/JPY or GBP/CHF directly, without routing every trade through USD.

In practice, you still see USD influence in the background. Many crosses track what each leg does versus USD, plus their own local flows.

High-liquidity crosses you will see most

These minors trade heavily and often show tighter spreads than other crosses.

- EUR/GBP, driven by euro zone and UK rate expectations, plus UK and EU data surprises.

- EUR/JPY, sensitive to risk sentiment and Japan yield moves, plus ECB policy shifts.

- GBP/JPY, a high-volatility cross, reacts hard to rate differentials and risk swings.

- AUD/JPY, often used as a risk barometer, links to commodities and Japan rates.

- EUR/CHF, influenced by Swiss National Bank policy and safe-haven demand.

Group minors by theme

Grouping crosses helps you map which drivers matter most, and when liquidity tends to peak.

- Euro crosses, EUR/GBP, EUR/JPY, EUR/CHF, EUR/AUD, EUR/CAD.

- Yen crosses, EUR/JPY, GBP/JPY, AUD/JPY, CAD/JPY, NZD/JPY.

- Pound crosses, EUR/GBP, GBP/JPY, GBP/CHF, GBP/AUD, GBP/CAD.

- Commodity crosses, AUD/NZD, AUD/CAD, CAD/JPY, NZD/JPY.

Example walkthrough, EUR/GBP vs EUR/USD

EUR/USD prices the euro against the dollar. It reacts to ECB versus Fed expectations, and US data can move it fast.

EUR/GBP prices the euro against the pound. It reacts to ECB versus Bank of England expectations, and UK specific news can dominate.

That changes your trade logic.

- Cleaner relative-value bet, EUR/GBP isolates Europe versus UK. You can express “ECB more hawkish than BoE” without taking direct USD exposure.

- Different volatility profile, EUR/GBP often trends in tighter ranges than EUR/USD, but it can gap on UK political headlines or surprise inflation prints.

- Different best hours, EUR/GBP tends to trade best during the London session. EUR/USD stays liquid through London and New York.

- Different technical behavior, EUR/USD often respects levels watched by the widest crowd. EUR/GBP can respect different zones because the participant mix differs.

Pros and cons of trading minors

- Pro, diversification, you can spread exposure across different central banks and economies instead of loading everything into USD pairs.

- Pro, targeted bets, crosses let you trade one macro story more directly, like BoE versus ECB or risk sentiment via AUD/JPY.

- Con, variable spreads, many crosses quote wider than majors, especially outside their home sessions or during news.

- Con, session-dependent liquidity, liquidity can drop hard in off-hours. Slippage risk rises, and stops can fill worse.

- Con, indirect USD link, even without USD in the quote, broad USD moves can still ripple through both legs.

If you want the mechanics behind pricing, spreads, and execution quality, read our guide on how the forex market works.

Exotic currency pairs: definition, examples, and when they make sense

Exotic currency pairs: what they are

An exotic currency pair links one major currency to one emerging or frontier market currency. Most exotics use USD, EUR, or JPY on one side. The other side often has lower trading volume and fewer market makers.

You trade exotics when you need exposure to a specific country risk. That can mean inflation, commodity dependence, politics, or central bank policy that does not track G10 cycles.

Common exotic pairs and what drives them

| Pair | Type | Typical drivers |

|---|---|---|

| USD/TRY | Major vs EM | Inflation, central bank credibility, reserves, capital flow pressure |

| EUR/TRY | Major vs EM | Turkey risk plus EU trade exposure and EUR funding conditions |

| USD/MXN | Major vs EM | Rate differentials, US growth, oil, risk sentiment |

| USD/ZAR | Major vs EM | Risk-on or risk-off flows, commodities, local power and fiscal risk |

| USD/BRL | Major vs EM | Rates, fiscal policy, commodities, election risk |

| USD/THB | Major vs EM | Tourism, trade balance, local policy, regional risk |

| USD/SGD | Major vs advanced Asia | MAS policy band, regional growth, USD cycles |

Why exotic spreads run wider

- Lower liquidity. Fewer buyers and sellers at each price level. Spreads widen fast when volume drops.

- Higher hedging costs. Dealers often hedge with NDFs, swaps, or proxies. Those markets can be expensive, especially around events.

- Market structure limits. Capital rules, local trading hours, onshore versus offshore pricing, and less competition between market makers all push spreads up.

These costs show up as wider quoted spreads, larger slippage, and less reliable fills. If you want the mechanics, read how the forex market works.

Key risks you must price in

- Gaps. Thin books can jump through your stop level. You get filled worse than planned.

- Weekend risk. Policy headlines can hit when markets close. Monday opens can gap hard.

- Capital controls. Authorities can restrict FX access, change settlement rules, or split onshore and offshore pricing.

- Sudden policy moves. Surprise rate changes, interventions, or rule changes can reprice the pair in minutes.

When exotics make sense

- You trade a clear macro theme. Inflation shocks, fiscal stress, or a strong rate cycle that can last weeks or months.

- You use carry with strict risk limits. Some exotics offer high yields, but funding stress can erase months of carry in a day.

- You can trade in the right hours. You need liquid overlap, reliable pricing, and a plan for event risk.

Pros and cons

- Pro, strong trends. Exotics can trend for long stretches when policy and capital flows align.

- Pro, carry potential. Higher local rates can pay, if volatility stays contained.

- Con, higher costs. Wider spreads and financing can turn small edges negative.

- Con, execution uncertainty. Slippage, partial fills, and gaps matter more than your entry signal.

Major, minor, and exotic pairs compared (quick decision framework)

Major, minor, and exotic pairs compared (liquidity, spread, volatility, holding time)

| Factor | Majors (EUR/USD, USD/JPY, GBP/USD) | Minors (EUR/GBP, AUD/JPY, GBP/JPY) | Exotics (USD/MXN, USD/ZAR, EUR/TRY) |

|---|---|---|---|

| Liquidity | Deep. Many participants. Reliable fills. | Medium. Good most hours, thinner outside core sessions. | Thin to uneven. Liquidity can vanish around local news. |

| Typical spread and total cost | Tight. Lowest spread and slippage in normal conditions. | Wider than majors. Costs jump when one leg is illiquid. | Wide. Financing can dominate your edge, especially on longer holds. |

| Volatility | Steady. Spikes around US and Europe data. | Variable. Can move fast when only one region trades. | High. Gaps and air pockets show up more often. |

| Typical holding period | Scalp to position trade. Most flexible. | Day to swing. Works best when you trade the active session. | Swing to position, if you can absorb drawdowns and financing. |

Majors fit systems that need precision. Minors reward session focus. Exotics punish weak execution and weak risk limits.

Which pair type fits your style (scalp, day, swing, position)

- Scalping, trade majors. You need tight spreads, fast fills, and low slippage. Avoid exotics.

- Day trading, majors first, then liquid minors during their active overlap. Keep trade duration aligned with the session that drives the pair.

- Swing trading, majors and minors both work. Use exotics only if your strategy accepts gaps and you size small enough to survive them.

- Position trading, majors for macro themes with lower friction. Exotics can work for carry or policy divergence, but your financing, drawdown limits, and event plan must come first.

Session timing changes the best pair to trade

- Asian session, AUD/JPY and USD/JPY often move cleaner than EUR/USD. Many Europe-focused pairs chop.

- London session, EUR/USD and GBP/USD usually offer the best combination of volume and range. Many minors linked to EUR and GBP come alive.

- New York session, USD pairs react to US data and rates. EUR/USD can trend on data, then mean revert after the first impulse.

- Overlap hours, expect the best liquidity and the tightest spreads in majors. You also get the highest news density, so tighten rules on entries and stops.

- Local exotic hours, liquidity improves, but event risk rises. A single headline can override technical levels.

If you ignore session timing, you will misread volatility. Your stops will look too tight, or your targets will look too small.

A quick decision framework (choose your pair in 60 seconds)

- Step 1, define your holding time. Minutes, hours, days, or weeks. Longer holds increase exposure to gaps and financing.

- Step 2, set a max all-in cost. Spread plus average slippage plus expected financing. If cost exceeds your average win, drop the pair.

- Step 3, check liquidity at your trading hours. Trade the pair when its main regions trade. If you cannot, stick to majors.

- Step 4, confirm your stop distance fits normal noise. If you need a 10 pip stop in a pair that regularly swings 30 pips in a minute, you picked the wrong market.

- Step 5, map event risk. Rate decisions, CPI, jobs data, and political headlines. If you cannot hold through it, plan to be flat.

- Step 6, size for the worst candle. Base risk on adverse move and gap risk, not on your ideal entry. Use a position sizing rule you can repeat.

Liquidity drives execution quality. If you want a deeper explanation, read forex liquidity first.

Common beginner mistakes when moving from majors to exotics

- Using major-style stops. Exotics need wider stops or smaller size, often both.

- Ignoring financing. Positive carry can flip negative after spreads and roll costs. Calculate it before you hold.

- Trading exotics like news scalps. Spreads widen, liquidity disappears, and slippage breaks your backtest.

- Overleveraging because the pip value looks small. Your real risk is the gap, not the pip.

- Assuming technical levels will hold. In thin markets, price can cut through levels without tradeable pullbacks.

- Holding through local political risk without a plan. You need predefined exits and a max loss rule for headline gaps.

What moves exchange rates for each pair type

Macro drivers, what matters most by pair type

All FX prices react to the same core forces. Rates, inflation, growth, and what the central bank signals next.

- Majors. Policy expectations drive most moves. When the market reprices the next 3 to 6 months of rate cuts or hikes, majors trend fast. Deep liquidity keeps spreads tight, but volatility spikes at data releases.

- Minors. You trade two developed economies at once, so relative expectations matter more. If one central bank turns hawkish while the other turns dovish, the cross can trend even when USD pairs chop.

- Exotics. Local rates matter, but credibility matters more. If the market doubts the central bank, the currency can fall even with high yields. Capital controls and intervention risk can override your macro view.

Risk sentiment and safe havens, why JPY and CHF differ

Risk sentiment shifts FX flows. You see it first in funding currencies and high beta currencies.

- JPY. Moves with global yields and carry trades. When yields drop and risk comes off, leveraged carry positions unwind, JPY strengthens. When yields rise and risk stays on, JPY often weakens.

- CHF. Trades more like a balance sheet haven. It can strengthen in stress even if yields do not collapse. The SNB can lean against CHF strength, so intervention risk sits in the background.

- Pair impact. In majors like USDJPY and EURCHF, risk shocks can dominate for hours or days. In minors like GBPJPY, the move can be sharper because both legs can swing at once.

Commodities and terms of trade, AUD, CAD, NZD linkages

Commodity exporters price their currencies off export income and global demand.

- AUD. Sensitive to China growth news, metals, and broad risk. AUDUSD can move with iron ore signals and Asian session headlines.

- CAD. Tracks oil more than people admit, especially when oil drives Canada’s trade balance. USDCAD can gap on crude shocks and OPEC headlines.

- NZD. Reacts to dairy, domestic growth, and risk tone. NZD pairs can feel thin outside Wellington and London overlap.

- How it changes by type. Commodity currencies as majors or minors still trade clean in liquid hours. When you see them in exotic combinations, spreads can widen and the commodity signal gets drowned out by local risk.

Emerging market specifics, politics, debt, reserves, and flows

Exotics move on constraints. External funding, reserves, and politics set the boundary conditions.

- Politics and policy. Elections, cabinet changes, and sudden fiscal plans can reprice an exotic in minutes. Headlines can beat charts.

- External debt. Large USD debt creates reflex moves. A stronger USD tightens funding, the local currency sells off, and hedging demand accelerates the drop.

- Reserves and intervention. Low reserves raise devaluation risk. Heavy intervention can pin price for weeks, then fail in a single session.

- Capital flows. EM FX depends on foreigners buying local bonds and equities. If global funds de risk, you get one way markets and gappy opens.

Event calendar essentials, what you must track

Majors react to scheduled data. Exotics react to schedules and surprises. You need both on your radar.

- CPI and inflation prints. Reprice rate paths fast. Biggest impact on majors like EURUSD, GBPUSD, USDJPY, and on inflation sensitive exotics when credibility sits on the line.

- Jobs data. US NFP and wage growth move USD pairs hard. Local employment matters most when it changes the next central bank step.

- Rate decisions and guidance. The statement and press conference move price more than the hike itself. Watch vote splits, dot plots, and forward guidance shifts.

- Unexpected headlines. Geopolitics, sanctions, capital controls, resignations, emergency meetings. Exotics can gap through stops. Trade smaller and predefine exits, then apply strict position sizing so one headline does not wipe your month.

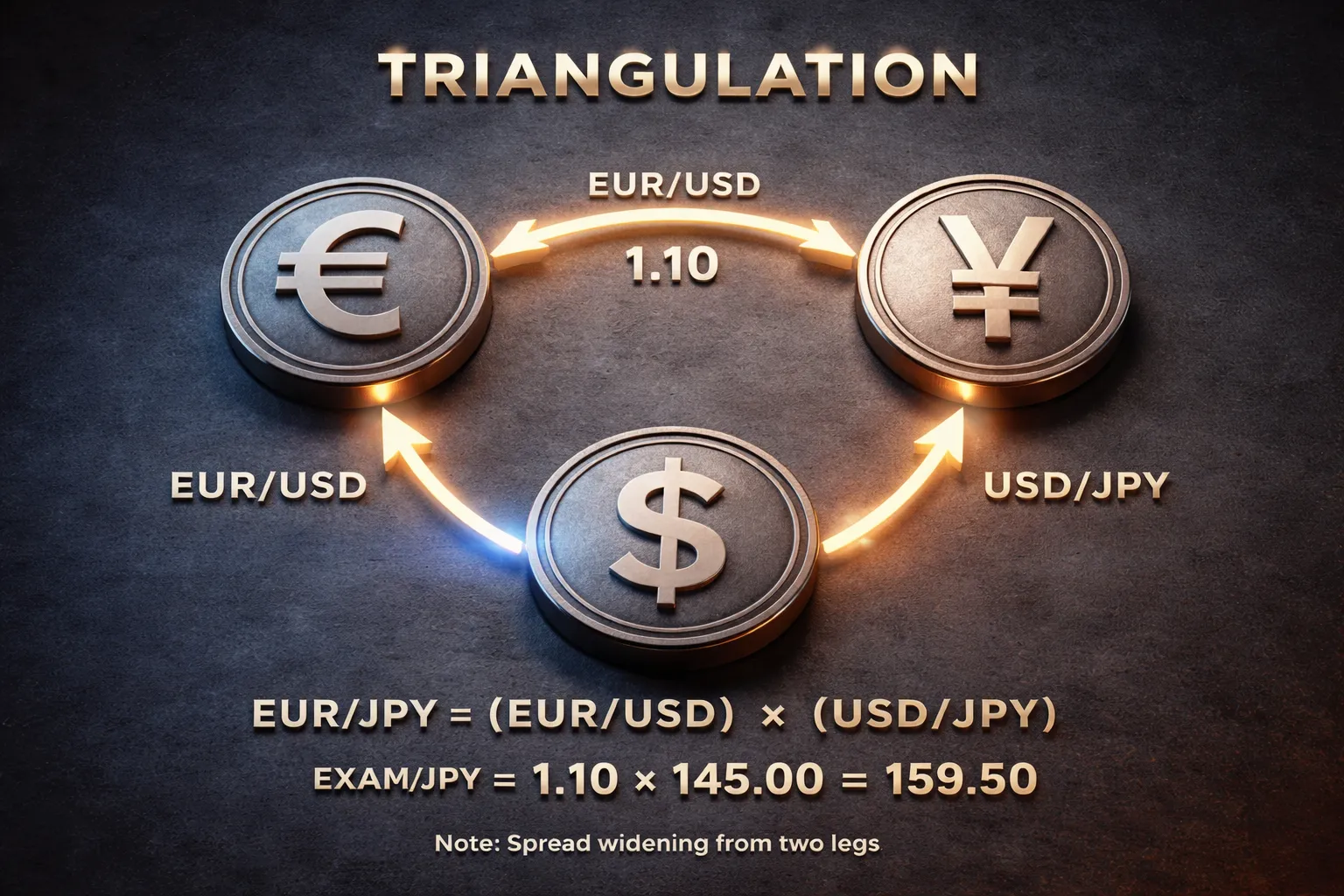

Cross rates and triangulation (how minors are derived)

Cross rates and triangulation, how minors are derived

Most minor pairs are cross rates. Dealers derive them from two majors that share a common currency, usually USD.

Example. You want a EUR/JPY quote. The market can imply it from EUR/USD and USD/JPY.

- Formula: EUR/JPY = (EUR/USD) x (USD/JPY).

- If EUR/USD = 1.0800 and USD/JPY = 150.00, then EUR/JPY = 162.00.

This is triangulation. You combine two liquid legs to get the cross.

Why cross-rate pricing can widen spreads in thin liquidity

A cross has two sources of spread, one from each leg. When liquidity thins, both legs widen. The cross widens more.

- Cross spread adds up: the implied cross must cover the cost and risk of quoting EUR/USD and USD/JPY.

- Legs can desync: one leg updates faster than the other during fast markets. The cross quote turns stale, then re-quotes wider.

- Less direct flow: some crosses have less natural two-way interest than majors. Dealers hedge through USD, so they price defensively.

Thin liquidity shows up around rollovers, holidays, session gaps, and surprise headlines. It also shows up when a central bank headline hits one leg first.

Practical execution impact, partial fills and slippage

Cross execution often routes through legs. Your broker may fill you on available liquidity, then hedge the other side. You see it as slippage, re-quotes, or partial fills.

- Partial fills: you get part of your size at the shown price, the rest at worse prices or not at all.

- Slippage: one leg moves while the other lags, the implied cross jumps, your fill price worsens.

- Stops can slip: in a fast cross, the executable price can gap past your stop level.

If you care about fill quality, trade smaller size, avoid thin windows, and use limit orders when you can. Liquidity drives this behavior, not your chart. Read forex liquidity basics if you want to map when this risk rises.

When triangulation arbitrage matters, and when it does not

Triangular arbitrage happens when the implied cross and the direct cross differ enough to cover costs.

- It matters for: banks, HFT firms, and liquidity providers that can trade all legs fast, with low fees, and with credit lines.

- It rarely matters for you: spreads, commission, latency, and execution rules usually erase the edge before you can capture it.

- It can still affect you: when the market snaps back into alignment, the cross can move fast with no clean technical trigger.

Use cross-rate logic to sanity-check quotes

You can use triangulation to spot bad pricing, platform glitches, and risky conditions.

- Step 1: pull mid prices for EUR/USD and USD/JPY.

- Step 2: multiply them to get the implied EUR/JPY mid.

- Step 3: compare with the shown EUR/JPY mid.

- Step 4: check spreads. If the cross spread looks extreme versus the legs, treat it as a liquidity warning.

If the cross deviates by more than you expect, assume execution risk. Reduce size, widen limits, or step aside until quotes normalize.

Risk management considerations by pair type

Position sizing by pip value and volatility

Size your position from risk first, not from habit. Majors usually give you tighter spreads and steadier fills. Minors move more per session and quote wider. Exotics can jump, gap, and reprice.

Start with your max loss per trade in account currency. Convert it into a stop distance in pips, then into a position size using the pair’s pip value. Do not assume pip value stays constant. If USD is not the quote currency, pip value changes as price changes.

- Majors: You can often run smaller stops for the same noise level, but do not over-leverage just because spreads look cheap.

- Minors: Use smaller size than majors for the same stop in pips. Daily range often runs larger and spreads can widen around sessions.

- Exotics: Use the smallest size. Treat the quoted spread as a cost and a warning. Your real cost can be higher during fast markets.

| Pair type | Typical spread and liquidity | Volatility profile | Practical sizing rule |

|---|---|---|---|

| Major | Tight, deep | Moderate | Baseline risk unit |

| Minor | Wider, thinner | Higher spikes | Cut size versus majors |

| Exotic | Wide, patchy | Jump risk | Smallest size, accept missed trades |

Use ATR and volatility stops, not fixed pips

Fixed-pip stops break across pair types. A 20 pip stop can be wide on EUR/USD and tight on GBP/JPY. Build stops from recent volatility instead.

- Use ATR from your trading timeframe. Many traders anchor to 14 periods.

- Set stop distance as a multiple of ATR, then size down so your cash risk stays constant.

- Recheck ATR after big news and after session changes. Volatility regimes shift fast in minors and exotics.

Keep the logic consistent. Volatility decides stop distance. Your risk limit decides size.

Gap risk, order choice, and weekend exposure

Gap risk rises as liquidity falls. Exotics carry the most gap risk. Some minors gap hard around local news. Majors still gap on major macro shocks.

- Stop orders: You get out, but you may get filled far from your stop in fast markets. Plan for slippage, especially on exotics.

- Limit orders: You control price, but you may not get filled. Use limits when you must cap entry cost, or when spreads jump.

- Weekend holds: Reduce or hedge before the close if the pair has a history of weekend gaps. Exotics often reprice on Monday open.

If spreads widen and quotes look unstable, treat stops as worst-case tools, not precise exits. The execution layer matters. Review how your broker routes orders and fills during spikes. See how the forex market works.

Correlation risk when you stack similar exposure

You can take five trades and still place one bet. Correlation turns separate pairs into the same exposure.

- Long EUR/USD and long GBP/USD both load you long USD weakness.

- Long AUD/USD and long NZD/USD stack similar risk, especially during risk-on and risk-off moves.

- Short USD/JPY and short USD/CHF can crowd into the same USD leg and the same flight-to-safety flows.

Track exposures by currency, not by pair count. Cap total risk per currency. If you add a second trade that shares the same driver, cut size on both.

Leverage and margin, why exotics draw down faster

Exotics punish leverage. They trade wider, move in jumps, and require more margin on many brokers. That combination accelerates drawdowns.

- Wide spreads hit your P and L at entry and exit. You start behind.

- Slippage rises during news and thin hours. Stops can fill worse than planned.

- Margin can change without warning. Some brokers raise margin on exotics around events.

- Funding and swap costs can run high. Carry can erase small edges.

Use lower leverage on minors. Use the lowest leverage on exotics. Keep more free margin than you think you need. A single gap should not trigger a margin call.

Costs beyond spreads: swaps, rollover, and funding effects

What swap and rollover are, and why they differ by pair

Swap is the overnight interest adjustment on your open spot FX trade. Brokers apply it at rollover, often at 5pm New York. Most brokers charge or pay swap every night. Many apply a triple swap on one weekday to cover the weekend.

Swap varies by pair because each currency has its own short term interest rate. It also varies because your broker sets its own swap schedule and adds a markup. Exotics often show bigger swap numbers because local rates sit far from G10 rates, and because brokers add wider buffers for risk and funding.

Carry trade basics: positive vs negative swap and rate differentials

Carry is the interest rate differential you hold when you stay long one currency and short the other. If you buy the higher yielding currency and sell the lower yielding one, you can receive positive swap. If you do the reverse, you usually pay swap.

- Positive swap adds to P and L each rollover, but it can flip if rates change or if the broker changes its schedule.

- Negative swap acts like a daily holding fee. It can turn a small winning trade into a loser if you hold too long.

- Direction matters. Long and short swaps differ. Do not assume they are symmetric.

Swap also interacts with trade size. You pay it per lot, not per pip. Tight spreads will not save you if your holding cost is large.

Why exotic carry looks good, and why it can hurt you

Exotics can offer high nominal yields. That makes positive swap look attractive. The risk comes from gaps, re pricing, and sudden volatility. A few bad days can erase months of carry.

- Higher jump risk. Political headlines, central bank actions, and capital controls hit exotics harder.

- Wider trading friction. Spreads, slippage, and swap all tend to rise in stress.

- Funding can vanish. Brokers can raise margin, cut leverage, or change swap rates quickly.

- One way markets. When risk turns, liquidity thins. Stops slip. You exit worse than planned.

Do not treat carry as free income. Price risk dominates. Carry works only if your downside stays contained.

Broker specific fees: commissions, markups, and overnight rate schedules

Your total cost depends on account type and broker policy. Two brokers can quote the same spread and still produce different net results.

- Commission. ECN style accounts add a per lot fee. Include it in your break even.

- Spread markup. Some brokers widen spreads instead of charging commission.

- Swap markup. Brokers often pay you less on positive swap and charge you more on negative swap.

- Rollover rules. Cutoff time, triple swap day, and holiday treatment differ.

- Base currency effects. If your account currency differs, conversion can add cost.

Read the broker swap table for each symbol you trade. Check both long and short values. Verify whether the broker lists swap in points, pips, or account currency.

How to estimate total trading cost before you enter

Estimate costs in money terms, not just pips. Use this checklist.

- Step 1. Record the average spread for your trading hours, not the minimum spread.

- Step 2. Add round turn commission, if any.

- Step 3. Estimate slippage for your order type and session, then add it as extra pips.

- Step 4. Multiply total pips by your pip value for the planned position size. Use a pip value calculator if you do not calculate it by hand.

- Step 5. Add expected swap for your holding period. Use the broker swap table and include the triple swap day.

- Step 6. Compare expected cost to your average target and stop size. If costs eat a large share of your expected move, skip the trade or reduce holds.

| Cost type | When you pay it | Why it matters more on minors and exotics |

|---|---|---|

| Spread | On entry and exit | Wider and less stable, especially outside local hours |

| Commission | On entry and exit | Adds fixed friction per lot, hurts small targets |

| Slippage | During execution | Liquidity gaps, worse fills, larger stop losses in practice |

| Swap and rollover | Each rollover | Bigger rate differentials, bigger broker buffers, higher surprise risk |

| Funding and margin changes | Any time | Leverage cuts and higher margin hit exotics first |

Pair selection examples for different trader goals

Low-cost learning path, start with one or two majors

Start where execution stays clean. Pick one or two majors. Track them daily for 30 to 60 sessions.

- EUR/USD, tight spreads, deep liquidity, steady news flow.

- USD/JPY, high liquidity, strong rate sensitivity, clear session behavior.

Keep your variables low. One setup. One timeframe. One risk rule. You learn faster when spreads and slippage do not dominate your results.

Diversification path, add one minor cross to cut USD concentration

After you can execute on a major, add one minor cross. You reduce USD exposure and you learn how crosses move without the dollar as the quote anchor.

- EUR/GBP, reacts to relative growth and central bank divergence, often range driven.

- EUR/JPY, mixes euro drivers with risk sentiment, can trend hard in macro cycles.

- GBP/JPY, higher daily range than many majors, demands wider stops and smaller size.

Do not add three at once. Add one cross, then compare your execution cost and stop distance to your major. If cost rises faster than your edge, drop it.

Opportunity path, criteria before you trade an exotic

Trade exotics only when the conditions justify the extra friction. Use objective gates.

- Spread to target, your average spread should stay a small fraction of your planned take profit. If the spread eats the trade, pass.

- Liquidity windows, trade during the pair’s active local session. Avoid dead hours.

- News and policy risk, check central bank decisions, inflation prints, and capital controls risk.

- Swap and funding, confirm rollover costs and whether your broker widens buffers on exotics.

- Margin stability, assume leverage cuts hit exotics first. Size for higher margin.

- Execution quality, expect worse fills. Read our guide on what is slippage in forex if you have not measured it.

Common exotics include USD/TRY, USD/ZAR, USD/MXN, EUR/TRY. Treat each as its own market. Do not assume it behaves like a major with a wider spread.

Example portfolios by trader profile

| Profile | Pairs | Why it fits | Main risk |

|---|---|---|---|

| Conservative | EUR/USD, USD/JPY | Lowest typical spreads, best fills, simpler monitoring | USD concentration, fewer distinct themes |

| Balanced | EUR/USD, USD/JPY, EUR/GBP | Adds a cross, reduces USD dependence, still liquid | Cross can chop, needs tighter rules for range regimes |

| Advanced | EUR/USD, USD/JPY, EUR/GBP, USD/MXN | Adds carry and local macro opportunity when conditions align | Spread, slippage, rollover shocks, margin changes |

Keep the list short. More pairs increase errors, not edge. Add a new pair only after you can show stable execution metrics on your current set.

A practical pre-trade checklist

- Liquidity, trade in the pair’s active session, avoid thin hours and holidays.

- Calendar, check central bank events and top tier data for both currencies. If risk sits inside your trade window, reduce size or skip.

- Spread, record the live spread at entry time. Compare it to your stop and target. If it is too large, pass.

- Volatility, size your stop to current range. If the pair demands a wide stop, cut position size.

- Risk limit, set a hard per-trade loss cap and a daily max loss. Stop after you hit it.

Run this checklist every time. It keeps your costs and tail risks visible, which matters most when you move beyond majors.

FAQ

What is a major currency pair?

A major pair includes the US dollar and a top liquidity currency. Examples: EUR/USD, USD/JPY, GBP/USD, USD/CHF. Majors usually show the tightest spreads and deepest liquidity, so your trade costs tend to stay lower than in minors or exotics.

What is a minor currency pair?

A minor pair does not include the US dollar. It still uses major currencies. Examples: EUR/GBP, EUR/JPY, GBP/JPY, AUD/NZD. Minors often have wider spreads than majors and can move fast during local data releases.

What is an exotic currency pair?

An exotic pair combines a major currency with an emerging market currency. Examples: USD/TRY, USD/ZAR, EUR/PLN, USD/MXN. Exotics usually have wider spreads, higher swap costs, and sharper gaps, so your risk control matters more.

Which has the lowest spreads, majors, minors, or exotics?

Majors usually have the lowest spreads. Minors often cost more. Exotics cost the most. Your actual spread depends on broker, session, and volatility. Always check the live spread before entry and compare it to your stop size.

Which pairs are best for beginners?

Start with majors. You get better liquidity and cleaner pricing. Keep your list small and learn one or two pairs first. If you trade minors or exotics, reduce position size and widen your safety margin for spread and slippage.

Do exotics always have higher volatility?

No. Exotics can show calm periods, then gap hard on news or liquidity drops. The bigger issue is tail risk, slippage, and sudden repricing. Use smaller size, avoid holding through key local events, and respect daily loss limits.

How many currency pairs should you trade?

Fewer. Track 2 to 6 pairs. You will learn their spread behavior, range, and news drivers faster. More pairs add monitoring load and increase the chance you trade a bad spread or a thin session.

What time of day is best for tight spreads?

Spreads often tighten during liquid overlaps, especially London and New York. They often widen during rollovers, holidays, and around major news. Check your platform’s spread at the exact time you plan to execute.

How do I size trades differently on majors vs exotics?

Base size on your stop distance and your cash risk cap, not on lot count. Exotics often need wider stops and still face slippage. If the required stop is large, cut size. Review margin vs leverage before scaling.

Are minors less liquid than majors?

Yes, in most cases. Some minors like EUR/JPY can stay fairly liquid, but still trail majors. Lower liquidity can mean wider spreads, more slippage, and less stable fills, especially outside active regional sessions.

Can I hold exotic pairs overnight?

You can, but expect higher carry costs and bigger gap risk. Check swap rates before you hold. Avoid holding through major central bank decisions and political events. Keep a hard per-trade loss limit and a daily max loss.

What is a “cross pair”?

A cross is any pair that does not include USD. Most crosses are minors, like EUR/GBP or GBP/JPY. Some crosses can be exotic, like EUR/TRY. Costs and volatility depend on the two currencies and the trading session.

What is the quickest way to compare majors, minors, and exotics?

| Type | Includes USD | Typical cost | Examples |

|---|---|---|---|

| Major | Yes | Lowest spreads | EUR/USD, USD/JPY |

| Minor | No | Medium spreads | EUR/GBP, EUR/JPY |

| Exotic | Often yes | Highest spreads | USD/TRY, USD/ZAR |

Conclusion

Major pairs trade tighter. You usually get the lowest spreads and the most liquidity.

Minor pairs add cost. You pay wider spreads and you often see sharper moves around European and UK hours.

Exotic pairs raise the stakes. Spreads can jump, swaps can bite, and price can gap during local news or thin sessions.

Your final step stays the same. Match the pair type to your risk and keep your position size small enough to survive a spread spike. Use a pip value calculator before you place the trade.

- If you want lower costs, start with majors.

- If you want specific regional exposure, use minors and accept higher spreads.

- If you trade exotics, plan for wide spreads, slippage, and higher margin needs.

-

Forex Leverage Explained: How It Works, Pros, Cons & Examples

1 month ago -

Forex Market Hours & Trading Sessions Explained (Best Times to Trade)

1 month ago -

What Is a Lot Size in Forex? Lot Types + Quick Examples

1 month ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

1 month ago -

What Are Pips in Forex? Definition, Examples & Why They Matter

1 month ago

-

-

- Liquidity is the core differentiator: depth, order flow, and slippage

- Transaction costs: typical spread ranges and commissions by pair type

- Volatility and gap risk: when price jumps matter more than spreads

- Market accessibility: trading hours, broker availability, and liquidity providers

- Why classifications can differ slightly across brokers and data providers

-

- Major, minor, and exotic pairs compared (liquidity, spread, volatility, holding time)

- Which pair type fits your style (scalp, day, swing, position)

- Session timing changes the best pair to trade

- A quick decision framework (choose your pair in 60 seconds)

- Common beginner mistakes when moving from majors to exotics

-

- What is a major currency pair?

- What is a minor currency pair?

- What is an exotic currency pair?

- Which has the lowest spreads, majors, minors, or exotics?

- Which pairs are best for beginners?

- Do exotics always have higher volatility?

- How many currency pairs should you trade?

- What time of day is best for tight spreads?

- How do I size trades differently on majors vs exotics?

- Are minors less liquid than majors?

- Can I hold exotic pairs overnight?

- What is a “cross pair”?

- What is the quickest way to compare majors, minors, and exotics?

-

-

-

- Liquidity is the core differentiator: depth, order flow, and slippage

- Transaction costs: typical spread ranges and commissions by pair type

- Volatility and gap risk: when price jumps matter more than spreads

- Market accessibility: trading hours, broker availability, and liquidity providers

- Why classifications can differ slightly across brokers and data providers

-

- Major, minor, and exotic pairs compared (liquidity, spread, volatility, holding time)

- Which pair type fits your style (scalp, day, swing, position)

- Session timing changes the best pair to trade

- A quick decision framework (choose your pair in 60 seconds)

- Common beginner mistakes when moving from majors to exotics

-

- What is a major currency pair?

- What is a minor currency pair?

- What is an exotic currency pair?

- Which has the lowest spreads, majors, minors, or exotics?

- Which pairs are best for beginners?

- Do exotics always have higher volatility?

- How many currency pairs should you trade?

- What time of day is best for tight spreads?

- How do I size trades differently on majors vs exotics?

- Are minors less liquid than majors?

- Can I hold exotic pairs overnight?

- What is a “cross pair”?

- What is the quickest way to compare majors, minors, and exotics?

-

-

Forex Lot Size Calculator: How to Use It to Size Trades Correctly

1 month ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

1 month ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

1 month ago -

Margin vs Leverage in Forex: What’s the Difference?

1 month ago -

What Is Forex Trading? A Beginner’s Guide to How It Works

1 month ago

-

Forex Leverage Explained: How It Works, Pros, Cons & Examples

1 month ago -

Forex Market Hours & Trading Sessions Explained (Best Times to Trade)

1 month ago -

Is Forex Trading Legal in the United States? Rules, Regulators & What to Know

1 month ago -

What Is a Lot Size in Forex? Lot Types + Quick Examples

1 month ago -

Forex Trading Platforms Comparison: MetaTrader vs cTrader vs TradingView

1 month ago