Regulated Forex Brokers Explained: Licenses, Safety & Red Flags

You send your money and trades through your broker. If the broker fails, your account can freeze. If the broker lies, you can lose funds and have no recourse.

A regulated forex broker holds a license from a financial authority and must follow rules on client money, reporting, and conduct. Regulation does not remove trading risk. It reduces counterparty risk.

This guide shows you how broker licenses work, which regulators set the strictest standards, and how to verify a license in minutes. You will also learn the safety checks that matter, like segregated accounts, compensation schemes, and negative balance protection. You will get clear red flags that signal offshore shells, fake authorizations, and weak oversight.

If you also want a curated shortlist after you learn the basics, see our best forex brokers for beginners guide.

Key Takeaways

- In het kort: A “regulated” broker has an active license from a real regulator, not a logo on a website.

- Start with the license number, then confirm it on the regulator’s register. Match the legal entity name and domain.

- Prioritize top tier oversight. FCA, ASIC, CFTC, NFA, MAS, IIROC, BaFin, and similar bodies enforce stricter rules.

- Check client money protection. Look for segregated accounts, a clear custody setup, and clean withdrawal terms.

- Know your backstops. Compensation schemes and negative balance protection reduce damage when things go wrong.

- Ignore “registered” language. Registration, incorporation, or a business number does not equal authorization to deal in FX.

- Watch for offshore red flags. Vague addresses, cloned firms, mismatched domains, and pressure to deposit fast.

- Don’t stop at regulation. Compare costs and execution, see our guide to forex broker fees.

Regulated forex brokers explained: what regulation really means

How broker oversight works

Regulation means a government agency, or a delegated authority, supervises your broker. The broker must meet rules to offer forex or CFDs to the public. The regulator can audit, fine, restrict, or shut the broker down.

- Licensing. The broker applies for permission to operate. The regulator checks owners, managers, systems, and funding.

- Ongoing rules. The broker must keep minimum capital, file reports, and separate client money from company money where required.

- Conduct standards. The broker must treat clients fairly, disclose risks, and follow marketing rules. Some regulators cap leverage and require negative balance protection.

- Monitoring. Regulators review filings, investigate complaints, and run inspections. They also share data with other agencies.

- Enforcement. Penalties can include fines, compensation orders, license limits, public warnings, and license removal.

Regulation reduces risk. It does not remove it. You can still lose money through trading losses, slippage, gaps, or poor execution. You can also face delays during disputes. Your job is to confirm the license, then judge the broker on costs, execution, and cash handling.

Broker vs platform vs liquidity provider: who is responsible for what

Many traders blame the platform for broker problems. Keep the roles clear.

- Broker. Holds your account, accepts your deposits, sets margin rules, runs order routing, and issues statements. The broker bears the legal duty to follow its regulator’s rules. Your complaint usually starts and ends with the broker.

- Trading platform. Software you use to place orders and view prices. A platform vendor may not hold client funds and may not be your counterparty. A platform issue can still hurt your trading, but it is not the same as broker oversight.

- Liquidity provider. Bank or market maker that provides pricing and fills. You usually have no direct contract with the liquidity provider. The broker chooses them, monitors them, and stays responsible for best execution under most rulebooks.

- Payment processor. Moves money. It does not replace broker regulation. High-risk processors and crypto-only funding often show up with weak brokers.

When something goes wrong, ask who controlled the decision. Pricing and fills, the broker. Platform stability, the broker and vendor. Withdrawals, the broker and its banking setup.

Key terms beginners confuse

| Term | What it usually means | What you should do |

|---|---|---|

| Licensed | A regulator granted permission to provide specific services. | Match the license number, legal entity name, and approved activities on the regulator register. |

| Authorized | Similar to licensed. The firm can legally offer regulated products in that jurisdiction. | Confirm the exact entity you sign with is the authorized one, not a related company. |

| Registered | Often means the company exists as a business. It may have no permission to offer forex. | Treat this as marketing until you see regulator authorization. |

| Passported | A firm can serve clients across a region under home regulation, based on local rules. | Check the host register entry and the services covered. Some passport rights have changed in recent years. |

| Member firm | Member of an exchange, association, or dispute scheme. Membership is not always regulation. | Confirm the member body’s power. Look for regulator supervision and enforcement history. |

After you confirm regulation, compare the total trading cost. Spreads can look cheap while commissions and swaps raise your bill. Use our guide on spread vs commission to judge account types.

Why trading with a regulated broker can be safer (and what it doesn’t guarantee)

Investor protections that may apply

Regulation does not make trading safe. It can make your broker safer to deal with. It sets rules the broker must follow. It gives you a regulator to complain to. It also raises the odds that the broker stays solvent and pays you on time.

- Segregated client funds. Many regulators require the broker to keep your money in separate accounts from its own operating cash. This can reduce misuse risk. It does not always protect you if the broker fails and the segregation was weak or breached.

- Capital and liquidity requirements. Regulators often set minimum net capital. This can improve the broker’s ability to handle client withdrawals and market stress.

- Best execution and fair dealing. Some regimes require policies for order handling, slippage, and conflicts of interest. You still need to watch fills, requotes, and stop execution quality.

- Leverage limits and margin rules. Many regulators cap leverage for retail clients and require margin closeout rules. This can reduce blow ups from small moves. It also limits your position size.

- Risk disclosures and product rules. You may get standardized risk warnings, negative balance protection in some regions, and tighter rules on bonuses and promotions.

- Dispute resolution and complaints process. Regulated brokers usually must follow a formal complaint path. Some jurisdictions add an external ombudsman or compensation scheme.

What regulation cannot prevent

Regulation targets broker conduct. It cannot fix trading risk. You can still lose money fast.

- Market losses. If price moves against your position, you take the loss. No license changes that.

- Gaps and extreme volatility. News events can gap price past stops. Slippage can be large. Some instruments can move when liquidity disappears.

- Strategy failure. Poor risk management, over leverage, and weak entry logic will still damage your account.

- Platform outages and execution limits. Regulation may require controls and reporting, but it cannot guarantee uptime or perfect fills during stress.

- Jurisdiction limits. If you open an account under an offshore entity, you may lose access to stronger rules, ombuds services, or compensation coverage.

Where protections differ for retail vs professional clients

Rules often protect retail clients more. If you opt into professional status, you can lose key safeguards.

- Leverage. Retail clients often face caps. Professional clients may get higher leverage and higher risk.

- Negative balance protection. Retail clients may get it in some jurisdictions. Professional clients often do not.

- Risk warnings and appropriateness tests. Retail onboarding may include stronger disclosures and suitability checks. Professional onboarding may rely more on your experience claims.

- Compensation schemes. Some investor compensation rules apply only to retail clients, or they cap coverage by client type and product.

- Complaint handling. Retail clients may access an ombudsman or dispute scheme. Professional clients may have fewer paths and stricter timelines.

If you want a step by step framework for checks beyond regulation, use our practical broker selection checklist.

Major regulator tiers and what they typically require

Common characteristics of strict jurisdictions

Top tier regulators focus on three things. Broker solvency, fair dealing, and clean supervision.

- Capital adequacy. You usually see higher minimum capital, plus ongoing capital ratios. The broker must hold enough liquid funds to survive losses and client withdrawals.

- Client money segregation. The broker must keep your funds in separate accounts at approved banks. You get clearer rules on how, where, and when the broker can move that money.

- Leverage and product controls. Many strict regimes cap leverage for retail clients and restrict incentives like bonuses. Some also require margin close-out rules and negative balance protection.

- Best execution and conflict rules. The broker must show how it routes orders and manages conflicts. You get disclosure on execution quality and dealing practices.

- Audits and reporting. Expect annual audited financial statements, frequent regulatory reporting, and event reporting when something breaks.

- Governance and fit and proper tests. Directors and key staff face vetting. Regulators expect risk controls, compliance staffing, and written policies.

- Marketing and disclosure rules. Regulators police risk warnings, performance claims, and how brokers describe spreads, commissions, and rollover costs. If you compare pricing models, see our guide on spread vs commission.

Mid-tier frameworks, solid oversight but narrower protections

Mid tier regulators can run serious supervision. You still need to check the fine print.

- Lower capital and simpler reporting. Requirements often exist, but the buffers can be thinner and reporting less frequent.

- Segregation rules with more exceptions. Client money rules may allow wider use of approved counterparties, or looser controls on reconciliations.

- Retail protections vary. Leverage caps, negative balance protection, and bonus bans may not apply, or may apply only to local residents.

- Enforcement can be uneven. The rules may look strong on paper, but fines, license removals, and public warnings may happen less often.

- Cross-border limits. A license may cover only a domestic market. If the broker solicits you from abroad, you may sit outside the regulator’s priority.

Offshore regulators, why they exist and what to watch for

Offshore licenses exist because brokers want lower costs, simpler onboarding, and fewer product limits. Some operate cleanly. Many use the location to reduce accountability.

- Light capital rules. Minimum capital can be low. A broker can scale fast without building real buffers.

- Weak client money standards. Segregation may be optional, or poorly supervised. You may not get clear custody and reconciliation rules.

- Limited audits and disclosure. Some regimes accept basic filings with minimal public transparency.

- Few conduct controls. High leverage, aggressive bonuses, and loose marketing claims show up more often.

- Harder dispute resolution. You may not have an ombudsman, a local court path, or practical enforcement if the broker refuses to pay.

- Red flag pattern. A broker promotes “regulated” but hides the entity name, license number, and legal address, or pushes you to sign with an offshore subsidiary even when it advertises a stronger license.

Examples of well-known regulators by region (for context, not an endorsement)

| Region | Common examples | How brokers often use them |

|---|---|---|

| UK | FCA | Often used for strict retail rules and clear supervision. |

| EU | CySEC, BaFin, AMF, CONSOB | Rules align under MiFID, but enforcement intensity can differ by country. |

| US | CFTC, NFA | High barriers to entry, strict reporting, tight product limits. |

| Canada | IIROC, provincial regulators | Strong oversight, tighter leverage, fewer brokers accepted. |

| Australia | ASIC | Well-known licensing, retail leverage limits, active supervision. |

| Singapore | MAS | Bank-grade expectations, strict licensing and conduct standards. |

| Japan | JFSA | Strict leverage caps and detailed oversight. |

| Dubai | DFSA | Often viewed as mid to upper tier, check which DIFC entity you contract with. |

| South Africa | FSCA | Common for regional access, protections can differ by product and entity. |

| Offshore centers | SCB, FSC Mauritius, FSA Seychelles, IFSC Belize, Vanuatu VFSC | Often used for higher leverage and broader client intake, you must verify the exact entity and protections. |

Broker licenses and legal entities: reading the fine print

How multi-entity broker groups operate

Many brokers run a group structure. One brand. Several legal entities. Each entity sits under a different regulator and rulebook.

Your protections depend on the exact entity on your account agreement. Not the logo on the website.

- Same platform, different rules. The broker can offer the same MT4 or MT5 setup, but change leverage limits, margin close-out rules, and negative balance protection by entity.

- Different product sets. One entity may offer CFDs, another may restrict certain instruments or offer different crypto access.

- Different money handling. Client money segregation rules, eligible banks, and reconciliation standards vary by regulator.

- Different dispute routes. Complaint handling, ombuds coverage, and court jurisdiction depend on the contracted entity.

Why the trading name can differ from the regulated company name

Websites and ads push a trading name. Regulators license a legal company. These often differ.

You must match the licensed company name and license number to what you sign. You usually find this in the footer, legal documents, and the account opening PDFs.

- Trading name: the brand you see on the site and app.

- Licensed entity: the company listed on the regulator register.

- Contracting party: the entity named in your client agreement, terms, and risk disclosure.

- Payment receiver: the company name on card charges and bank wires, it should align with the contracting party or a clearly disclosed group payments entity.

Red flag. The broker highlights a top-tier regulator on the homepage, but your agreement points to a different offshore entity.

Cross-border onboarding and which laws apply to your account

When you sign up from one country, you can still get onboarded to an entity in another country. The broker does this to manage leverage, marketing permissions, product scope, and client acceptance rules.

For you, one question matters. Which entity holds your account.

- Look for the “you are contracting with” line. It sits in the application flow, client agreement, or terms.

- Check the jurisdiction clause. It states the governing law and the courts or arbitration venue.

- Confirm the regulator in writing. Your portal usually lists the regulated entity, address, and license number.

- Do not assume local protections. Your passport and residence do not automatically grant you local investor compensation or ombuds access.

- Track entity switches. Brokers can ask you to migrate accounts. Read what changes, leverage, protections, and complaint process.

| What to verify | Where to find it | Why it matters |

|---|---|---|

| Legal entity name | Client agreement, terms, footer | Defines who owes you duties and holds your funds |

| License number | Regulator register, broker legal page | Lets you confirm authorization and permissions |

| Country of regulation | Disclosure documents | Sets leverage rules, conduct rules, and enforcement strength |

| Governing law and venue | Terms, dispute resolution section | Controls how you can file and where you must file |

| Client money rules | Client money policy | Affects segregation, handling, and insolvency outcomes |

If you want to compare account types across entities, start with fees. Use this guide on spread vs commission pricing.

How to verify a broker’s regulatory status step-by-step

1) Find the exact legal entity and license number on the broker’s site

Start on the broker’s website, not on ads, review sites, or social profiles.

- Open the Legal, About, or Regulation page.

- Find the company legal name. You need the entity name, not the brand name.

- Find the license number and the regulator name.

- Find the registered address and country.

- Check the client contracting entity in the Terms. This is the entity you will actually trade with.

- Check the domain listed in the footer and legal pages. Write it down.

If the broker shows multiple entities, match each entity to the account type and region it serves. Brokers often route retail clients to an offshore entity.

2) Check the regulator’s official register and match every field

Use the regulator’s website register. Do not trust screenshots or PDF “certificates” on the broker’s site.

- Search by license number first. If search fails, search by legal name.

- Confirm status. Look for “Authorised”, “Licensed”, or the regulator’s active equivalent. Avoid “Revoked”, “Suspended”, “Expired”, or “Unlicensed”.

- Match the legal name letter for letter. Small differences can mean a different company.

- Match the registered address. One city mismatch can signal a clone.

- Match the website domain shown on the register to the domain you will use to sign up and log in.

- Check trading names if the register lists them. Your broker brand should appear there.

- Open any public notes on the register entry, warnings, restrictions, or disciplinary actions.

If the register does not list a domain, treat the broker’s domain claim as unverified and tighten checks on name, address, and permissions.

3) Spot license clones and impersonators fast

Clones copy real license details from a legitimate firm, then use them to sell you an account.

- Domain mismatch. The register shows one domain, the broker asks you to sign up on another.

- Lookalike brands. Small spelling changes, extra words, or different punctuation.

- Altered license numbers. Extra digits, missing digits, or a number that belongs to a different firm.

- Wrong address. The site shows a different suite, street, or city than the register.

- Different contact details. Email and phone do not match the regulator listing.

- Pressure to deposit. The salesperson rushes funding before you can verify.

If you see any mismatch, stop. Do not deposit. Use the regulator’s site contact details to confirm the firm’s real domain.

4) Confirm the permissions cover forex, CFDs, and your client type

A valid license does not always cover the product you trade or the protections you expect.

- Check the register for permissions or authorised activities.

- Confirm it allows FX and, if relevant, CFDs or derivatives.

- Confirm it allows service to retail clients, not only professional or eligible counterparties.

- Check for restrictions, product bans, or limits on leverage and marketing.

- Confirm the licensed entity is the one named in your client agreement and account application.

If you want a broader due diligence flow, use our practical broker checklist.

Core safety features to assess beyond the license

Client fund segregation

Segregation means your broker must hold client money in separate accounts from its own operating funds. The goal is simple, reduce the risk that your deposit gets used to pay the broker’s bills.

Segregation does not guarantee you get your money back if the broker fails. It does not remove market risk. It does not stop losses from trading. It also does not protect you from fraud if the broker lies about where it holds funds.

How to confirm it.

- Read the broker’s client money policy. Look for clear wording such as “client funds are held in segregated accounts” and the regulator rule reference.

- Check the legal entity named in your account agreement. Confirm the policy applies to that exact entity.

- Ask support which bank holds client funds and in which country. A serious broker answers. A weak broker dodges.

- Check whether the broker can use client money for hedging, margin, or credit under its terms. Some regimes allow limited “title transfer” or collateral use for certain products. Avoid unclear language.

Negative balance protection and margin close-out rules

Negative balance protection means you cannot lose more than you deposit in your trading account. Without it, a fast gap can put your account below zero and you can owe the broker money.

Margin close-out rules define when the broker must reduce or close positions as your margin level falls. Strong rules force earlier action and reduce the chance of a negative balance during sharp moves.

- Find the negative balance section in the terms. Look for plain wording that losses cap at your account equity, and that the broker will reset a negative balance.

- Check whether protection applies to all clients or only retail. Many regulators require it for retail accounts, not for professional status.

- Check the margin close-out level in the product disclosure. Common setups trigger close-out when margin level hits a fixed percentage. Lower thresholds usually mean higher risk of falling negative in a gap.

- Check how the broker handles weekend gaps and extreme volatility. Your terms should state the broker’s rights and your liability.

Compensation schemes and insolvency protections

Some regulators back an investor compensation scheme. It can pay eligible clients if a regulated firm fails and cannot return client assets. It does not cover trading losses.

Coverage depends on the regulator, the product, and the legal entity that holds your account. It often applies only to retail clients and only after insolvency.

| Protection type | When it helps | Typical limits |

|---|---|---|

| Investor compensation scheme | Broker becomes insolvent and client assets cannot be returned | Commonly capped per client, amount varies by country |

| Segregated client funds | Limits commingling with broker money, supports asset return process | No fixed payout limit, recovery can still be partial and slow |

| Professional indemnity insurance | May cover specific claims such as negligence, if policy applies | Policy limits and exclusions apply, not a client guarantee |

- Confirm the exact scheme name tied to the broker’s regulator and entity. Do not rely on marketing pages.

- Read eligibility rules. Check whether CFDs and leveraged FX qualify in that jurisdiction.

- Check the compensation cap and claim process on the scheme’s official site, not the broker’s summary.

Dispute resolution

A solid broker gives you a clear complaint path and access to an independent dispute body when you cannot resolve an issue directly.

- Find the broker’s complaints policy. It should list contact details, required information, and steps.

- Check timelines. A serious policy states when you should receive an acknowledgment and when you should receive a final response.

- Confirm independent escalation. Look for ombudsman or external dispute resolution access for your jurisdiction and entity.

- Keep records. Save chats, emails, trade IDs, platform logs, and account statements. You need these for any formal complaint.

Operational security basics

Licensing does not secure your login. You still need basic controls that stop account takeovers and reduce withdrawal fraud.

- 2FA. Use app based authentication if the broker supports it. Avoid SMS only when you can.

- Withdrawal controls. Check for name matching, withdrawal whitelists, and cooling off periods for new bank details.

- Access controls. Look for device management, session timeouts, and login alerts.

- Data protection. Check where the broker stores data and which standard it claims to follow. Look for clear privacy notices and breach reporting commitments.

- Support security. Test support. Ask how they verify identity before changing email, phone, or bank details.

If you want a full workflow, use our practical broker checklist.

Costs, execution, and conflicts of interest (often overlooked in safety checks)

Spread, commission, swaps. Where the real costs hide.

Regulation does not cap your trading costs. You need to map every fee to your strategy.

- Spread. You pay it on entry and exit. Check the typical spread, not the minimum. Compare normal hours and news hours.

- Commission. Often charged per side, per lot. Convert it to pips so you can compare brokers. Total cost equals spread plus round-trip commission.

- Swaps and financing. You pay or earn it when you hold overnight. It can dwarf spread on long holds, high leverage, or wide rate differentials. Check long and short swap rates on your main pairs. Check triple swap day.

- Markups. Some brokers add a markup to swaps or spreads on specific account types. Look for language like “from” or “variable” with no typical value.

- Non-trading fees. Withdrawal fees, inactivity fees, conversion fees, and payment processor charges. These hit small accounts hard.

If the broker avoids publishing typical spreads, commission per lot, and swap tables, treat that as a risk signal. Use a practical broker checklist to capture the numbers before you deposit.

Slippage, requotes, and execution quality. What to measure.

Execution is part of safety. Poor fills can drain an account even when pricing looks fine.

- Slippage. The gap between requested and filled price. You want data on both positive and negative slippage. If the broker reports only one side, assume the other side hurts you.

- Requotes. A broker rejects your price and offers a new one. Frequent requotes often appear during fast markets. That can block stops and entries when it matters.

- Fill rate. How often orders fill at the first price without rejection.

- Execution speed. Look for median and 95th percentile, not a single best-case number.

- Order types under stress. Test market orders, stops, and stop limits during liquid and volatile sessions. Track your own slippage and rejection logs.

- Stop handling. Read the order execution policy. Check how they define “market conditions,” “off quotes,” and “best execution.” Those clauses decide disputes.

| Metric | What you want to see | Red flag |

|---|---|---|

| Typical spread | Published per instrument, with time window | Only “from 0.0” marketing |

| Slippage stats | Positive and negative distribution | One-sided reporting |

| Requote rate | Low, disclosed, explained | No data, vague excuses |

| Execution speed | Median and tail latency | Single best-case number |

| Trade dispute process | Clear steps, timestamps, audit trail | “Sole discretion” language |

Dealing desk vs agency, STP, ECN. What it implies for conflicts.

Execution model changes who wins when you lose.

- Dealing desk, market maker. The broker may take the other side of your trade. That can create a direct conflict. It does not mean automatic fraud, but it raises the need for strict controls, clear pricing rules, and strong oversight.

- Agency, STP, ECN. The broker routes orders to external liquidity and earns from spread markups, commissions, or both. Conflicts can still exist through last-look practices, internalization, or selective routing. You still need execution data.

- Hybrid models. Many brokers switch routing based on size, volatility, or client profile. You need clarity on when they internalize flow.

- Look for disclosures. Search the legal docs for “principal,” “agent,” “matched principal,” “internalization,” “last look,” and “liquidity provider.” These terms explain incentives.

Bonuses, “risk-free” trades, and rebates. How incentives can harm you.

Promotions often target behavior that increases broker revenue. They can also block your withdrawals.

- Deposit bonuses. They usually require high volume targets before you can withdraw. That pushes overtrading and higher leverage.

- “Risk-free” trades. The refund often comes as credit, not cash. It can expire. It can lock you into more trading.

- Rebates and IB programs. They reward high turnover. If an educator or signal seller gets paid per lot, your best interest comes second.

- Terms that trap funds. Watch for clauses that let the broker cancel profits, reverse trades, or delay withdrawals for “bonus abuse.”

- Regulatory mismatch. Many top-tier regulators restrict or ban retail bonuses. Heavy bonus marketing can signal a weaker jurisdiction or an offshore entity.

When a broker pushes incentives over transparent costs and execution stats, treat it as a safety issue, not just a marketing choice.

Red flags and scam patterns regulators frequently warn about

Unrealistic promises regulators flag

- Guaranteed returns. Any promise of fixed profit, daily yield, or “risk-free” forex breaks basic market reality and often breaches marketing rules.

- “No-loss” systems. Claims like loss insurance, protected trades, or a magic algorithm usually hide limits, exclusions, or a bonus trap.

- Account managers pushing deposits. Pressure to “top up now,” match a deposit, or upgrade tiers signals a sales room, not a broker. Treat urgency as a control tactic.

- Performance screenshots and leaderboards. Many scams use cherry-picked results, demo statements, or edited MT4 reports. Ask for audited, regulator-grade disclosures. They rarely exist.

Withdrawal friction tactics

- Endless verification loops. The broker keeps asking for new documents, repeats checks, or demands notarized papers after you request a withdrawal.

- Surprise fees. Extra “processing,” “compliance,” “tax,” or “wallet unlock” fees appear only when you withdraw. Regulated firms disclose withdrawal fees upfront.

- Minimum volume conditions. The broker blocks withdrawals until you hit trading volume targets, often tied to bonuses or “account status.”

- Partial payments and delays. Small withdrawals go through, larger ones stall. The goal is to keep you depositing while they control your cash flow.

Entity bait-and-switch

- Top-tier badge, offshore onboarding. The website highlights a strong license, but your account contract sits under a different company in a weak jurisdiction.

- Different domain, different entity. You sign up on one site, then get redirected to a “global” or “international” site with separate terms.

- License details that do not match. The legal name, license number, address, or website listed on the regulator register does not match the broker page you use.

- Wrong regulator scope. The firm holds a license for another activity or another country, then markets services outside its permissions.

Opaque terms and missing disclosures

- No clear risk documents. You cannot find basic risk disclosures, product documents, or clear warnings about leverage and losses.

- Vague execution policy. The broker does not explain how it routes orders, handles slippage, rejects orders, or manages conflicts.

- Missing legal pack. No client agreement, no complaints process, no company details, no margin call and stop-out rules.

- One-sided clauses. Terms let the broker change pricing, widen spreads, cancel trades, or void profits with broad wording.

- Cost fog. Spreads, commissions, swaps, and inactivity fees stay unclear or change without clear notice. Use a simple cost check before you fund. See spread vs commission.

Aggressive marketing channels tied to scams

- Unsolicited calls and DMs. Cold calls, Telegram pitches, and WhatsApp outreach often sit at the center of boiler-room sales.

- WhatsApp signal groups. You get “trade alerts” and pressure to deposit more to “follow the next move.” Losses get blamed on you, then they sell a higher tier.

- Fake reviews and cloned sites. Many scams buy reviews, copy regulated brands, and use near-identical domains. Verify the exact URL on the regulator register.

- Recovery scams. After you lose money, a new “firm” contacts you and claims it can recover funds for a fee. Regulators warn this pattern often targets victims twice.

| Warning sign | What it often means | What you do |

|---|---|---|

| Guaranteed profits, no-loss claims | Illegal marketing or fraud model | Stop, do not deposit, verify the entity on the regulator register |

| Withdrawal delays, new fees at withdrawal | Cash flow control, exit block | Request written fee policy, document all chats, escalate fast |

| License badge but different contracting company | Offshore onboarding | Check the legal entity on your account agreement and the regulator register |

| No execution policy, missing legal docs | No accountability | Do not trade until you can read and download the full legal pack |

| Cold calls, WhatsApp pressure, “recovery” offers | Boiler-room tactics | Block contact, report to the regulator, never pay recovery fees |

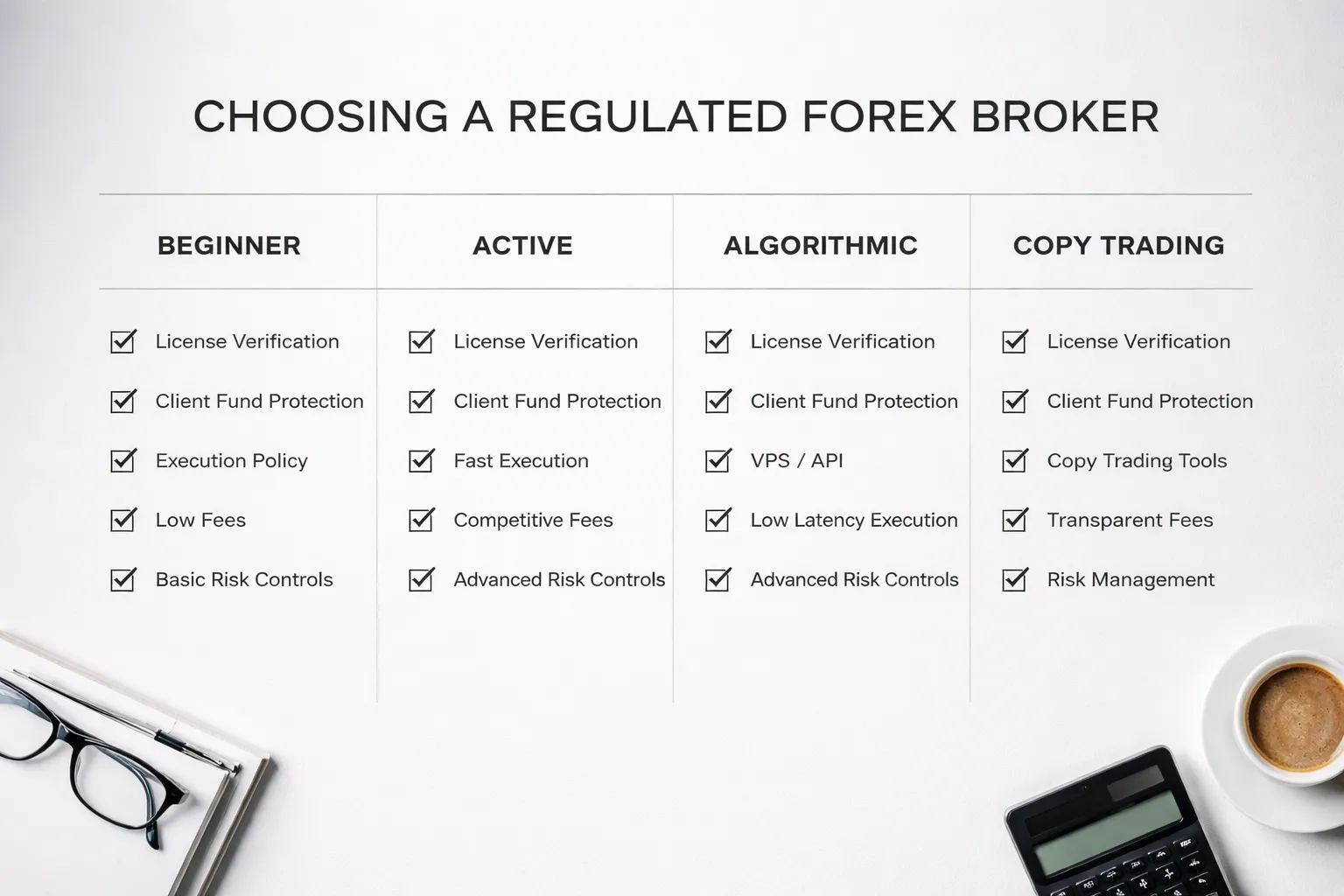

Choosing a regulated broker: a practical checklist for different trader types

Beginner checklist: simplicity, protections, education, and conservative leverage

- Confirm the regulator and entity. Match the broker name, license number, and legal entity on your account agreement to the regulator register.

- Choose a top-tier jurisdiction when possible. Prefer FCA, ASIC, IIROC, MAS, or a strong EU regulator under ESMA rules. Treat offshore add-ons as higher risk.

- Check client money rules. Look for segregation of client funds, where money is held, and whether the broker can use client funds for hedging or operating costs.

- Know your protections. Confirm negative balance protection, complaint process, and whether any investor compensation scheme applies to your entity.

- Use conservative leverage. If you can select leverage, start low. Avoid accounts that push high leverage by default.

- Start with simple pricing. Pick one clear account type. Avoid complex tiers, rebates, or VIP programs.

- Demand a clean fee table. Spreads, commissions, swaps, deposit fees, withdrawal fees, and inactivity fees must sit in the legal docs, not only in marketing pages.

- Use a demo first. Test order placement, spreads during news, slippage, and platform stability before you fund the account.

- Check withdrawals early. Make a small deposit, then a small withdrawal. Track time to process and any surprise charges.

- Prefer strong education and risk tools. Look for clear margin info, position sizing calculators, and guaranteed access to statements and trade history.

Active trader checklist: execution, fees, order types, and platform stability

- Verify the execution model. The broker must state market maker, STP, or ECN in its execution policy. Learn the differences in ECN vs STP vs Market Maker.

- Read the execution policy. You want clear rules on slippage, requotes, order rejection, and how the broker handles fast markets.

- Measure real trading costs. Compare average spreads, commissions per lot, and swap rates. Judge costs on your pairs and your trading hours, not on advertised minimums.

- Check order types. Confirm stop, limit, stop-limit if needed, partial close, OCO where available, and whether stops can trigger during gaps.

- Check instrument specs. Contract size, minimum lot, minimum stop distance, margin rates, and trading hours must be published and consistent in-platform.

- Stress-test platform uptime. Track disconnects, freezes during sessions, and stability during major data releases.

- Test fills in live conditions. Place small trades across sessions. Record slippage and fill speed on market orders and stop orders.

- Check margin call rules. Confirm margin call level, stop-out level, and whether the broker can change requirements before news or weekends.

- Review deposit and withdrawal rails. Prefer established banking and card channels. Be careful with brokers that push crypto rails as default.

Algorithmic trader checklist: VPS, APIs, latency, and historical quality of fills

- Confirm platform support. Check the exact version and bridge setup for MT4, MT5, cTrader, or a proprietary platform. Ask how updates affect EAs and scripts.

- Get API details in writing. If the broker offers FIX or other APIs, confirm access requirements, costs, throttling limits, and supported order types.

- Plan for VPS. Check whether the broker offers a VPS, where it sits, uptime targets, and what happens during maintenance windows.

- Check server location. Ask for trading server location and data center. Place your VPS near it to reduce latency.

- Audit execution logs. You need millisecond timestamps, order IDs, and full deal history export. Avoid platforms that hide execution metadata.

- Test for execution drift. Compare expected vs actual entry price on market orders and stop orders over a sample size, not a handful of trades.

- Check for plugin risk signs. Look for vague language on “price improvements” with no data, frequent off-quotes, or systematic negative slippage without symmetric positive slippage.

- Validate backtest data inputs. Confirm historical data source, timezone, rollover policy, and whether the platform uses last look or aggregated pricing.

- Confirm hedging rules. Some entities restrict hedging or FIFO. Match the rule set to your strategy before you fund.

Copy/social trading checklist: signal transparency, risk controls, and fee clarity

- Verify who runs the signal. You need a real identity or a regulated firm profile. Avoid anonymous providers with no track record outside the platform.

- Demand full performance disclosure. Look for max drawdown, time in market, leverage used, average holding time, and trade frequency. Ignore screenshots.

- Check live account proof. Confirm the signal trades on a real account with verifiable history, not only a demo or “model portfolio.”

- Inspect risk settings. You need equity stop, max allocation, max leverage cap, and the ability to pause copying instantly.

- Review trade copying mechanics. Confirm how the platform handles slippage, partial fills, minimum lot sizes, and whether it copies by lot, equity percent, or risk percent.

- Map all fees. Check spread markups, performance fees, management fees, subscription fees, and withdrawal fees. You must know who gets paid and when.

- Check conflicts of interest. Watch for providers who earn more when you trade more, or platforms that promote high turnover strategies.

- Control concentration. Avoid copying one strategy with most of your account. Split risk across uncorrelated approaches if you copy at all.

- Plan an exit. Confirm you can stop copying, close positions, and withdraw without lockups or penalties.

| Trader type | Non-negotiables | Fast red flags |

|---|---|---|

| Beginner | Top-tier license, segregated funds, clear fees, low leverage option, easy withdrawals | High leverage push, unclear legal entity, vague fee page, blocked withdrawals |

| Active trader | Execution policy, stable platform, predictable costs, proper order types, published margin rules | Requotes, frequent “off quotes,” hidden stop distances, surprise margin changes |

| Algorithmic | VPS plan, API clarity, execution timestamps, consistent fills, server location transparency | Missing logs, unstable connections, one-sided slippage, unclear bridge setup |

| Copy/social | Verified history, drawdown disclosure, risk caps, fee transparency, instant stop control | Anonymous providers, marketing-only stats, hidden fees, lockups, pressure to “top up” |

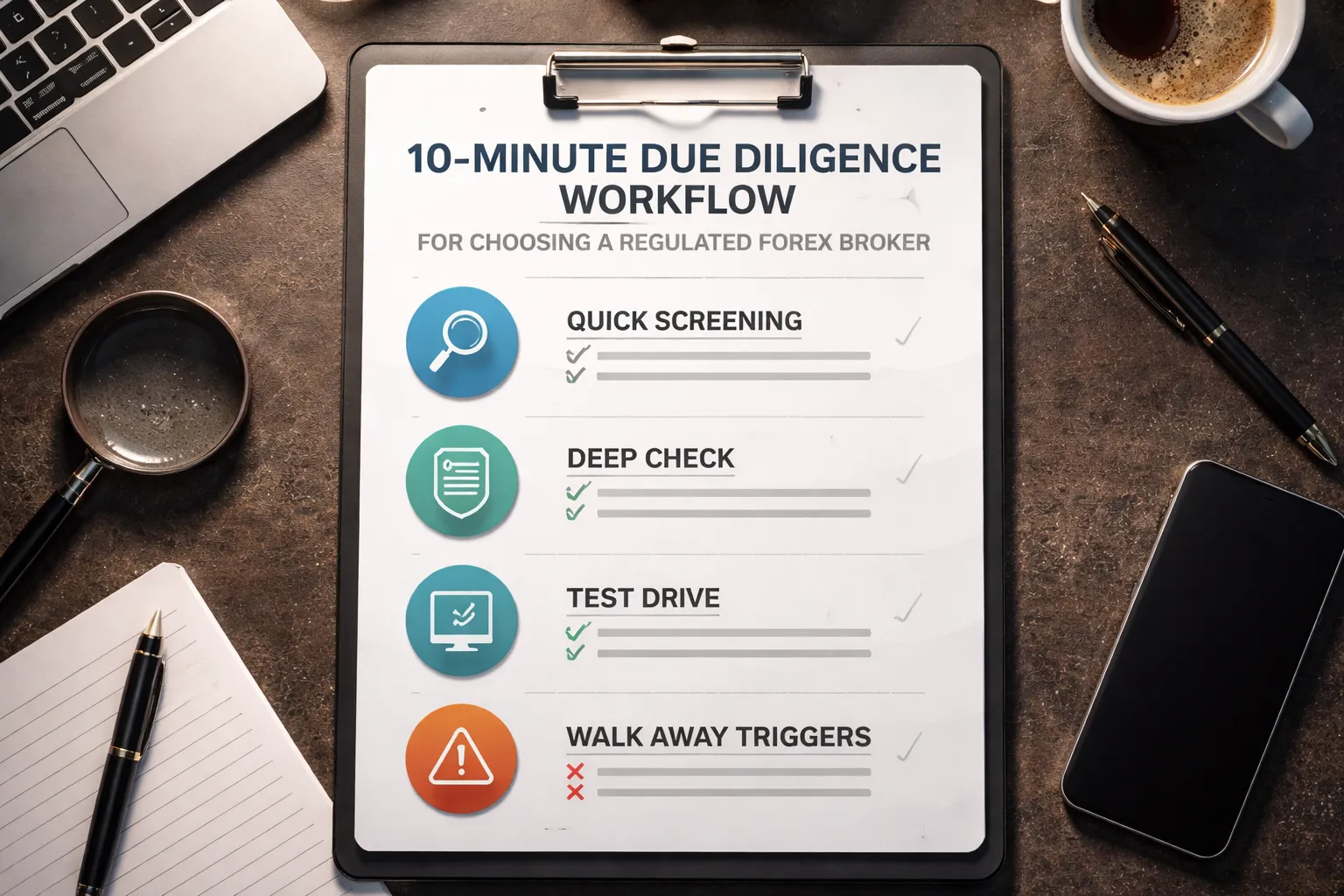

Putting it all together: a 10-minute due diligence workflow

Quick screening, license, permissions, entity match

- Step 1, copy the legal entity name. Take it from the broker footer, Client Agreement, and product disclosure. You need the exact company name, not the brand.

- Step 2, find the license in the regulator register. Use the regulator site, not a screenshot on the broker site. Match the license number, company name, and address.

- Step 3, confirm the permissions. Check what the license allows. Look for dealing in derivatives, CFDs, and FX, plus the right to hold client money if the broker holds funds.

- Step 4, map your account to the right entity. Check the entity on your onboarding screens, your account application, and your terms. If you get routed to an offshore subsidiary, treat that as your real counterparty.

- Step 5, scan the regulator record for issues. Look for restrictions, past enforcement, name changes, and warnings about clone firms.

Deep check, policies, conflicts, disclosures, financials

- Execution and slippage policy. Read the execution policy. Check how they handle re-quotes, partial fills, price improvement, and negative slippage. Look for clear timestamps and venue logic.

- Conflicts of interest. Find out if they act as principal, run a dealing desk, internalize flow, or hedge. You want plain language on who takes the other side and when.

- Client money and custody. Confirm segregation, eligible banks, and what happens if the broker fails. Check if they use omnibus accounts and if they can rehypothecate.

- Costs and charges. Pull the full fee schedule. Include spreads, commissions, swaps, inactivity fees, deposit and withdrawal fees, and conversion markups. Use this when you compare account pricing, see spread vs commission.

- Margin and liquidation. Check margin call levels, stop-out rules, and forced closeout order. Look for rules that let them change margin without notice during volatility.

- Complaints and dispute path. Confirm the process, timelines, and the external ombudsman or arbitration scheme, if any.

- Financial statements, if available. For listed firms, read annual reports. For some regulators, search for capital adequacy and audited accounts. You want solvency, clean audit opinions, and stable cash flow.

Test drive, demo, small deposit, full withdrawal

- Demo test, 15 minutes. Check platform stability, order types, stop and limit behavior, and the history log. Export reports if the platform allows it.

- Small live deposit. Use the smallest amount that still lets you trade normally. Avoid bonuses and “special programs” tied to volume or lockups.

- Execution test. Place a set of small market and limit orders in normal and news-adjacent conditions. Record fill time, slippage, and any rejections.

- Support test. Ask two direct questions, one about execution and one about fees. Judge speed, clarity, and whether they answer with policy language.

- Full withdrawal test. Withdraw 100 percent of the remaining balance. Track how long it takes, what documents they request, and whether they add fees you did not see upfront.

Decision framework, when to walk away even if the broker is regulated

- Entity mismatch. The brand advertises a strong license, but your account sits under a weaker entity.

- Permission mismatch. The firm holds a license, but it does not clearly cover leveraged FX or CFDs for your jurisdiction.

- Policy fog. Execution rules, slippage handling, and conflict disclosures stay vague or change across documents.

- Withdrawal friction. Delays, new document demands, “compliance” holds with no timeline, or pressure to cancel withdrawals.

- Cost surprises. Fees appear at withdrawal, conversion, or swap, and the broker cannot point you to a clear fee page.

- Sales pressure. Calls push leverage, upsells, or “recovery” after losses. Legit brokers do not need pressure tactics.

- Platform and logs fail. Missing trade history, inconsistent timestamps, frequent disconnects, or unexplained price spikes.

- Regulator signals trouble. Restrictions, warnings, frequent name changes, or related entities with enforcement actions.

FAQ

What makes a forex broker “regulated”?

A regulator issues a license to a legal entity. The broker must follow rules on client money, reporting, conduct, and capital. You should confirm the exact entity name and license number in the regulator register, then check the permissions match the services you use.

Does regulation guarantee your money is safe?

No. Regulation lowers risk, it does not remove it. Your safety depends on client money segregation, leverage limits, complaint handling, and enforcement strength. You still need to test deposits and withdrawals, review fees, and avoid brokers with repeated sanctions.

How do you verify a broker’s license fast?

Find the legal entity name in the footer or terms. Search the regulator register. Match the name, license number, website domain, and address. Check permissions and restrictions. If the broker cannot show the licensed entity clearly, do not fund the account.

What is a “clone” broker scam?

Scammers copy a real firm’s license details, then use a different domain, email, or phone number. You avoid this by matching the broker’s domain and contact details to the regulator entry and the licensed firm’s official site. If details differ, walk away.

What licenses matter most for retail forex?

Licenses from strict regulators usually give stronger oversight and clearer client money rules. Focus on your account’s legal entity and your country coverage. A group can hold multiple licenses, but your protections come from the entity that holds your account.

What are the biggest red flags in regulation claims?

Missing license number. “Regulated” with no regulator named. License belongs to a different entity. Offshore entity listed for your account. Domain mismatch in the register. Warnings on regulator sites. Aggressive bonus offers tied to withdrawal blocks.

What is client money segregation?

The broker keeps your funds in separate accounts from its operating money. It reduces misuse risk, but it does not prevent losses if the bank fails or if fraud occurs. Read the broker’s client money policy and confirm the regulator requires segregation.

Do you get investor compensation if the broker fails?

Sometimes. It depends on the regulator, your entity, and eligibility rules. Compensation often covers insolvency, not trading losses. Check the scheme name, maximum payout, and exclusions in your entity’s jurisdiction. Do not assume coverage applies to you.

How can you reduce risk before you deposit big?

Start with a demo, then a small live deposit. Place market and limit orders. Test a full withdrawal to your bank or wallet. Keep records. Scale only after clean withdrawals and stable execution. For step-by-step screening, use a practical checklist for choosing a forex broker.

Can a regulated broker still manipulate prices?

Yes. Some brokers internalize trades and set their own pricing model. Regulation limits abuse but does not remove conflicts. Read the execution policy, check how the broker handles slippage, and compare live spreads to benchmarks during news and active sessions.

What is the difference between regulation and registration?

Regulation usually means a license to offer forex to retail clients under ongoing supervision. Registration can mean a basic listing with fewer permissions. Always check the regulator entry for “authorized” status and the permitted activities, not marketing claims.

Conclusion

Regulation does not remove trading risk. It reduces broker risk. You still need to verify the license, match it to the legal entity you will fund, and confirm the broker can legally serve clients in your country.

- Start with the regulator. Find the firm in the official register. Check the status, license number, and permitted activities.

- Match the entity. Align the register entry with the broker’s legal name, address, domain, and client agreement. Do not fund a different subsidiary.

- Confirm protections. Check segregation rules, negative balance protection, and any investor compensation scheme limits.

- Test execution. Use a small deposit. Track slippage, requotes, and withdrawal times. Compare spreads in calm and fast markets.

- Watch the red flags. Pressure sales, “guaranteed” returns, bonus lockups, unclear fees, and missing legal documents.

Final tip, build a one page broker checklist and keep it updated. If the broker fails one hard check, license mismatch, unauthorized status, blocked withdrawals, walk away. Then compare pricing across account types so you understand the real cost of trading, see spread vs commission.

-

Spread vs Commission: Which Forex Account Type Is Cheaper?

5 months ago -

Forex Demo Account Guide: What It Is, How It Works & How to Use It

5 months ago -

Forex Broker Fees Explained: Spreads, Commissions, Swaps & More

5 months ago -

How to Open a Forex Trading Account (Step-by-Step for Beginners)

5 months ago -

Best Forex Brokers for Beginners (Top Picks + What to Look For)

5 months ago

-

-

- Beginner checklist: simplicity, protections, education, and conservative leverage

- Active trader checklist: execution, fees, order types, and platform stability

- Algorithmic trader checklist: VPS, APIs, latency, and historical quality of fills

- Copy/social trading checklist: signal transparency, risk controls, and fee clarity

-

- What makes a forex broker “regulated”?

- Does regulation guarantee your money is safe?

- How do you verify a broker’s license fast?

- What is a “clone” broker scam?

- What licenses matter most for retail forex?

- What are the biggest red flags in regulation claims?

- What is client money segregation?

- Do you get investor compensation if the broker fails?

- How can you reduce risk before you deposit big?

- Can a regulated broker still manipulate prices?

- What is the difference between regulation and registration?

-

-

-

- Beginner checklist: simplicity, protections, education, and conservative leverage

- Active trader checklist: execution, fees, order types, and platform stability

- Algorithmic trader checklist: VPS, APIs, latency, and historical quality of fills

- Copy/social trading checklist: signal transparency, risk controls, and fee clarity

-

- What makes a forex broker “regulated”?

- Does regulation guarantee your money is safe?

- How do you verify a broker’s license fast?

- What is a “clone” broker scam?

- What licenses matter most for retail forex?

- What are the biggest red flags in regulation claims?

- What is client money segregation?

- Do you get investor compensation if the broker fails?

- How can you reduce risk before you deposit big?

- Can a regulated broker still manipulate prices?

- What is the difference between regulation and registration?

-

-

How to Place a Forex Trade Step by Step (Your First Trade Explained)

3 months ago -

Forex Trading vs Crypto Trading: Which Market Is Better for Beginners?

3 months ago -

Forex Lot Size Calculator: How to Use It to Size Trades Correctly

5 months ago -

How to Calculate Position Size in Forex (Position Sizing Formula + Examples)

5 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

5 months ago

-

Forex Trading Platforms Comparison: MetaTrader vs cTrader vs TradingView

5 months ago -

Is Forex Trading Legal in the United States? Rules, Regulators & What to Know

5 months ago -

Stop Loss vs Take Profit: Differences, Examples & Best Practices

5 months ago -

Forex Market Hours & Trading Sessions Explained (Best Times to Trade)

5 months ago -

Forex Leverage Explained: How It Works, Pros, Cons & Examples

5 months ago